Macro Extremes (week ending June 7, 2024)

June 9, 2024 Leave a comment

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

* denotes multiple week inclusion

Extremes above the Mean (at least 2.5 standard deviations)

AUD/ZAR

Dutch TTF Gas *

Overbought (RSI > 70)

Brazilian 10 year government bond yield

Biodiesel *

Rubber *

AEX

KLSE

and Taiwan’s TAEIX

The Overbought Quinella (Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Robusta Coffee *

USD/MXN

Extremes below the Mean (at least 2.5 standard deviations)

Australian 10 year minus Australian 2 year government bond yield spread *

Australian 10 year minus Australian 5 year government bond yield spread

Heating Oil

Iron Ore CFR China

CAD/EUR

CAD/GBP

BOVESPA

Mexico

MOEX

And Thailand’s SET equity index

Oversold (RSI < 30)

Chilean 2 year government bond yield *

North European Hot Rolled Coil Steel *

U.S. Midwest Hot Rolled Coil Steel *

Lumber *

Lithium Hydroxide *

PHP/USD *

The Oversold Quinella (Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

BRL/USD

MXN/USD

Notes & Ideas:

Government bond yields were mostly lower.

As a result, last week’s oversold entries are no longer.

The exception is the Brazilian 10’s are back being overbought.

Chilean 2 year yields have fallen for 7 consecutive weeks. Their oversold reading may lead the world in a trough in yields.

We saw a large decline in Japanese yields across the curve.

U.S. 10 year yield minus German 10 year yield spread is in a 8 week declining streak.

And the Copper/Gold ratio has fallen for the past 3 weeks.

Equities were mixed.

While may indices spent the week between +/- 0.5% – 0.8% from last weeks close.

Budapest and Amsterdam are at all-time highs.

Several more indices dropped out of overbought territory, while a few traded to some overbought extremes.

S&P SmallCap 600, the Russell 2000, Tel Aviv 25 and Oslo performed a bearish outside reversal week.

And Switzerland’s SMI is nearing a overbought quinella.

Commodities were mostly weaker, again.

Cocoa & Coffee all saw strength again.

Robusta Coffee and Cocoa have risen 23% and 31%, respectively over the past 3 weeks.

Coal, Aluminium, Steel, Nickel and Copper were amongst the weakest performers for the week.

Copper has fallen 12% in the past 3 weeks.

Gasoline has fallen 5 of the past 6 weeks, as has Brent Crude Oil.

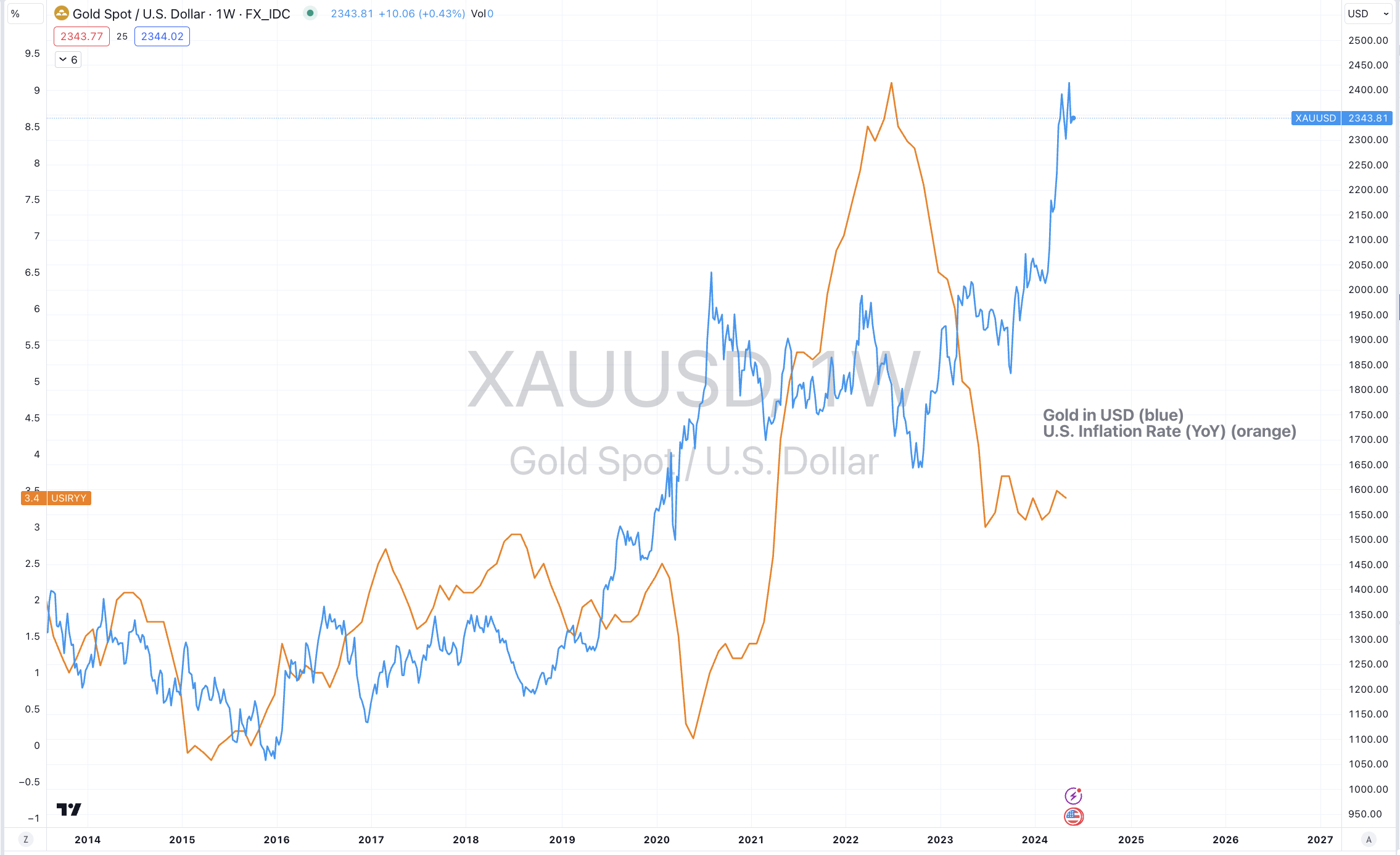

And Gold as priced in Swiss Francs has fallen 6% over the past 3 weeks.

Grains were weaker too.

Rubber & Biodiesel broke their 5 week winning streaks.

U.S. Midwest Hot Rolled Coil Steel fell, following last week’s outside bearish week.

Orange Juice has fallen 11%, nearly halving the 27% advance seen in the prior 5 weeks.

And Lithium Hydroxide has now spent 47 consecutive weeks in weekly oversold territory.

Currencies continue to provide action.

The Aussie was weaker and didn’t make a new high against the Yen.

AUD/INR, AUD/THB and the AUD/USD had outside bearish reversal weeks.

In keeping with general weakness amongst commodities, the Loonie was also weaker.

The GBP/AUD had a bullish outside reversal week.

The Yen rose and as a result the GBP/JPY broke its 4 week winning streak.

The USD was stronger.

PHP/USD is in a 5 week losing streak.

And the Mexican Peso fell 8% (against the USD) following its election result.

The larger advancers over the past week comprised of;

Cocoa 6.5%, Natural Gas 12.8%, Robusta Coffee 3.8%, Sugar 3.8%, Urea U.S. Gulf 2.6%, Urea Middle East 5.1%, Rice 2.8%, AEX 2.2%, Budapest 2.9%, HSCEI 1.8%, Hang Seng 1.6%, IDX 2%, Nasdaq 100 2.4%, KOSPI 3.3%, Nasdaq Biotech 2.3%, Nasdaq 100 2.5%, NIFTY 3.4%, Copenhagen 1.7%, SENSEX 3.7%, SMI 2.1%, SOX 3.2%, S&P 500 1.3%, TAEIX 3.2%, Vietnam 2.1%, ASX 200 2.1% and the ASX Industrials rose 1.9%.

The group of largest decliners from the week included;

Aluminium (3.2%), Rotterdam Coal (8.8%), WTI Crude Oil (1.9%), Cotton (3%), Lean Hogs (1.9%), Copper (2.6%), HRC (4.3%), LNG in Yen (5.5%), Lithium (3.3%), Tin (3.1%), Newcastle Coal (7.6%), Nickel (8.8%), Orange Juice (3.1%), Platinum (6.8%), SPGSCI (1.6%), Iron Ore CFR China (8.5%), Dutch TTF Gas (3.3%), Brent Crude Oil (2.2%), Uranium (2.7%), Silver in AUD (3%), Silver USD (4%), Gold in CHF (2.1%), Oats (10.2%), Soybean (2.1%), Wheat (7.5%), KBW Banking Index (1.9%), Egypt (1.8%), S&P SmallCap 600 (2.5%), Russell 2000 (2.2%), KRE Regional Banks (3.4%), KSE (2.8%), S&P MidCap 400 (2.1%), Mexico (4%), BIST (2.5%) and Tel Aviv 25 fell 1.7%.

June 9, 2024

by Rob Zdravevski

rob@karriasset.com.au