All time highs doesn’t mean bubble

October 14, 2024 Leave a comment

The Nasdaq 100 is stretched but not bubbly

October 14, 2024

Trying to hear what's not being said

October 14, 2024 Leave a comment

The Nasdaq 100 is stretched but not bubbly

October 14, 2024

October 13, 2024 Leave a comment

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

* denotes multiple week inclusion

Extremes above the Mean (at least 2.5 standard deviations)

Brazilian and Turkish 10 year government bond yield

U.S. 5 year bond yield minus the U.S. inflation rate (YoY) spread

U.S. 10 year bond yield minus the U.S. inflation rate (YoY) spread

Shanghai Composite *

CSI 300 *

HSCEI *

Hang Seng *

Nasdaq Transports

And Australia’s ASX Small Caps *

Overbought (RSI > 70)

Middle East Urea *

Gold as priced in AUD, CAD, CHF, EUR, GBP & USD *

Dow Jones Industrials

And Toronto’s TSX *

The Overbought Quinella (Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Pakistan’s KSE *

Extremes below the Mean (at least 2.5 standard deviations)

None

Oversold (RSI < 30)

U.S. 3 month government bill yield *

Australian Coking Coal

U.S. Midwest Hot Rolled Coil Steel *

North European Hot Rolled Coil Steel *

Lithium Carbonate *

Lithium Hydroxide *

The Oversold Quinella (Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

None

Notes & Ideas:

Broadly, it was a week to ‘leave the bat on the shoulder’ and there was nothing to do.

Global government bond yields mildly rise, adding to last week’s move.

Yields across the UK and U.S. curve are in a 4 week rising streak.

The US minus German 10 year spread has also risen for 4 consecutive weeks.

While the US 5 year breakeven inflation rate and and the US 5 year yield minus US 3 month bill spread have both risen for 5 weeks.

U.S. 2’s are their highest weekly close in 2 months.

Equities were mixed.

Understandably, Chinese and Hong Kong indices gave up some of the previous weeks gains.

Last week, I wrote that around July 2020 – February 2021 was the last time we saw Chinese A50, CSI 300 and Shanghai Composite register an overbought quinella.

This week, they only appear in the overbought category because they traded up to their 2.5 standard deviation mark early in the week.

In addition, the China A50, HSCEI, Hang Seng and Egyptian indices had bearish outside reversal weeks.

DJ Industrials notable entrant in overbought this week.

The Nasdaq Composite has put together a 5 week winning streak as have the S&P MidCap 400, Nasdaq 100, S&P 500 and the TSX.

The Philippines PSE winning run ended at 5 weeks.

And Thailand’s SET is closing in on a overbought quinella reading.

Commodities were the busiest of the 4 assets classes featured in Macro Extremes.

The bia was slightly tilted to weakness.

Gold across various currencies remains overbought.

Silver and Sugar aren’t overbought this week.

Coking Coal joins Steel prices in oversold territory.

The Baltic Dry Index has fallen 15% over the past fortnight.

Lean Hogs are in a 5 week winning streak.

Sugar, Tin, Nickel and CRB Index all broke their 4 week winning streaks.

U.S.Midwest Hot Rolled Coil Steel has spent 20 weeks being oversold.

And Lithium Hydroxide has now spent 65 consecutive weeks in weekly oversold territory.

Currencies action was dominated by U.S. strength, again.

The DXY Index is at its highest close in 2 months.

All currency pairs which are appeared in last week’s edition no longer appear.

The Aussie fell while the Swiss rose.

The Yen also rose, albeit slightly.

CHF/AUD broke its 4 week losing streak and AUD/EUR broke its 4 week rising run.

And the British Pound was flat to slightly lower.

The larger advancers over the past week comprised of;

Cocoa 9.5%, WTI Crude Oil 1.6%, Heating Oil 1.4%, Lithium Hydroxide 1.7%, Orange Juice 2.3%, Palladium 7.1%, Gasoline 2.7%, Rubber 1.6%, Gold in CAD 1.5%, Wheat 1.6%, KBW Bank Index 4%, Dow Jones Transports 2.7%, MIB 2.1%, TAIEX 2.7%, KRE Regional Banks 3.9%, KSE 2.3%, S&P Midcap 400 1.2%, Nikkei 225 2.5%, Copenhagen 1.4%, SET 1.8%, SOX 2.5%, Nasdaq Transports 2.7%, WIG 1.8%, ASX Financials 2.4% and the ASX Small Caps rose 2.5%.

The group of largest decliners from the week included;

Australian Coking Coal (4.5%), Rotterdam Coal (2.1%), Bloomberg Commodity Index (1.3%), Baltic Dry Index (6.2%), China Coking Coal (4.3%), North European Hot Rolled Coiled Steel (1.8%), Copper (1.8%), US Midwest Hot Rolled Coiled Steel (2.6%), Arabica Coffee (2.1%), Tin (4.1%), Natural Gas (7.8%), Nickel (2.9%), Shanghai Rebar (1.9%), Robusta Coffee (4.7%), Sugar (3.4%), Dutch TTF Gas (2.7%), Middle East Urea (2%), Silver in AUD (1.4%), Silver in USD (2.1%), Corn (2.1%), Oats (2.2%), Soybeans (3.1%), Shanghai Composite (3.6%), CSI 300 (3.3%), China A50 (10.6%), Egypt (3%), HSCEI (6.6%), Hang Seng (6.5%), MOEX (1.8%), PSE (2.1%), BIST (2.6%) and the ASX Materials Index fell 1.4%.

October 13, 2024

by Rob Zdravevski

October 9, 2024 Leave a comment

My latest newsletter discusses how a stretched, full valued equities market can still ‘rip’ higher.

“shenanigans in the late hours of this current party (cycle) is when things become dangerous.

It’s also often when the most fun is had.”

The link to read and subscribe is below.

October 6, 2024 Leave a comment

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

* denotes multiple week inclusion

Extremes above the Mean (at least 2.5 standard deviations)

Turkish 10 year government bond yield

U.S. 10 year bond yield minus the U.S. inflation rate (YoY) spread

Silver in AUD & USD *

AUD/CAD *

AUD/INR *

AUD/USD *

BIST

And Australia’s ASX Small Caps *

Overbought (RSI > 70)

Sugar *

Urea (Middle East and U.S. Gulf)

Gold as priced in AUD, CAD & USD *

MYR/USD *

Egypt

Karachi *

Philippines PSE *

And Toronto’s TSX

The Overbought Quinella (Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Gold in CHF, EUR & GBP

Shanghai Composite

CSI 300

HSCEI *

Hang Seng *

Extremes below the Mean (at least 2.5 standard deviations)

CAD/AUD *

EUR/GBP *

Oversold (RSI < 30)

U.S. 3 month government bill yield *

U.S. Midwest Hot Rolled Coil Steel *

North European Hot Rolled Coil Steel *

Lithium Carbonate *

Lithium Hydroxide *

The Oversold Quinella (Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

None

Notes & Ideas:

Broadly, many things that were trading at ‘extremes’ last week, are no longer so, this week.

Global government bond yields rose.

Yields across the UK curve are in a 3 week rising streak.

Japanese yields rose strongly, recovering last weeks decline.

Commensurate to bond yields being oversold recently, inversely, this publication listed iShares 1-3 year Bond ETF (SHY) being overbought. It was implying to consider the antithesis of being long bonds. This past week, SHY fell 1%. This gave up 33% of the capital gain seen over the past 6 months.

U.S. 2’s are their highest weekly close in 2 months.

The U.S. 5 year yield minus the 3 month bill spread has climbed for 4 straight weeks.

And various U.S. yield spreads listed last week have broken their 6 week rising streak.

Equities were mainly lower, contrary to any bullish feelings being felt.

The pocket of strength was contained to Chinese and Hong Kong indices.

In fact, the Chinese market was only open on Monday.

The July 2020 – February 2021 period was the last time we saw Chinese A50, CSI 300 and Shanghai Composite register an overbought quinella.

The Nasdaq Composite has put together a 4 week winning streak.

The Philippines PSE is in a 5 week winning run.

The ASX Financials Index has fallen 6.5% in the past fortnight after being overbought in the week prior.

And Toronto’s TSX makes a return to overbought territory.

Commodities were mixed, although the indices strength due to their weighting to energy contracts.

The Bloomberg Commodity Index has risen 8.6% over the past 4 weeks.

Gold across various currencies remains overbought as does Silver.

Urea is a new overbought entrant.

Coffee isn’t overbought anymore.

Cocoa and Shipping Rates took a shellacking.

While Coking Coal prices bounced out from oversold territory.

Sugar, Tin, Nickel and CRB Index are in 4 week winning streaks, while Natural Gas its.

Shanghai Rebar prices have soared 15% over the past 2 weeks.

Soybeans broke its 6 consecutive weeks of positive closes.

U.S.Midwest Hot Rolled Coil Steel has spent 19 weeks being oversold.

And Lithium Hydroxide has now spent 64 consecutive weeks in weekly oversold territory.

Currencies action was dominated by U.S. strength.

The DXY Index broke its 4 week losing streak and rose 2%.

Hence I had a confusing read of currencies during the week.

Risk-off was seen in equities but the AUD and CAD rose.

And the Yen fell.

CHF/AUD has fallen for 4 consecutive weeks.

The AUD has risen for 4 weeks against the Euro.

The GBP was generally weaker.

And the THB/USD is no longer overbought as the Thai Baht broke its 4 weeks rising trend, falling 3% against the USD.

The larger advancers over the past week comprised of;

Australian Coking Coal 19.7%, Rotterdam Coal 3.2%, Bloomberg Commodity Index 1.8%, WTI Crude Oil 9.1%, DXY Index 2.1%, Lean Hogs 2.4%, Heating Oil 7.5%, Tin 4.1%, Newcastle Coal 2.3%, Nickel 5.7%, Gasoline 8.8%, Shanghai Rebar 12.1%, S&P GSCI 4.6%, CRB Index 2%, Dutch TTF Gas 6.2%, Urea U.S. Gulf 3.9%, Brent Crude Oil 8.5%, Gasoil 8.4%, Urea Middle East 5.3%, Silver in AUD 3.4%, Silver in USD 1.8%, Gold in CHF 1.9%, Gold in GBP 1.7%, Gold in ZAR 2%, Corn 1.6%, Wheat 1.7%, Shanghai Composite 8.1%, CSI 300 8.5%, China A50 16.3%, HSCEI 11.7%, Hang Seng 10.7%, KSE 2.8% and Oslo rose 3%.

The group of largest decliners from the week included;

Baltic Dry Index (8.6%), Cocoa (14.6%), Arabica Coffee (4.4%), Lumber (1.9%), Lithium Carbonate (5.6%), Lithium Hydroxide (5.1%), Natural Gas (1.7%), Palladium (2.4%), Platinum (2%), Robusta Coffee (7.6%), Rubber (1.6%), Soybeans (2.6%), All World Developed ex USA (3.5%), Budapest (1.5%), CAC (3.2%), DAX (1.8%), DJ Transports (2.3%), MIB (3.3%), IBEX (2.6%), IDX (2.8%), MOEX (1.9%), TAEIX (2.3%), KLSE (1.8%), KOSPI (3%), FTSE 250 (1.6%), Nikkei 225 (3%), NIFTY (4.5%), Copenhagen (2.3%), SENSEX (4.5%), SMI (1.9%), Vietnam (1.6%), BIST (6.8%) and the ASX Financials fell 2%.

October 6, 2024

by Rob Zdravevski

October 5, 2024 Leave a comment

I have now exited all (except for one) Chinese related equities.

Years ago, when equity markets were in the doldrums, I would hear people tell me how they would gladly accept a 7% return in a given year.

Over the past 3 weeks, some Chinese/HK stocks and indices have risen 30%.

I bet if many or any caught one-third of that gain, they wouldn’t pack up for the next 12 months and stay away from the markets…….

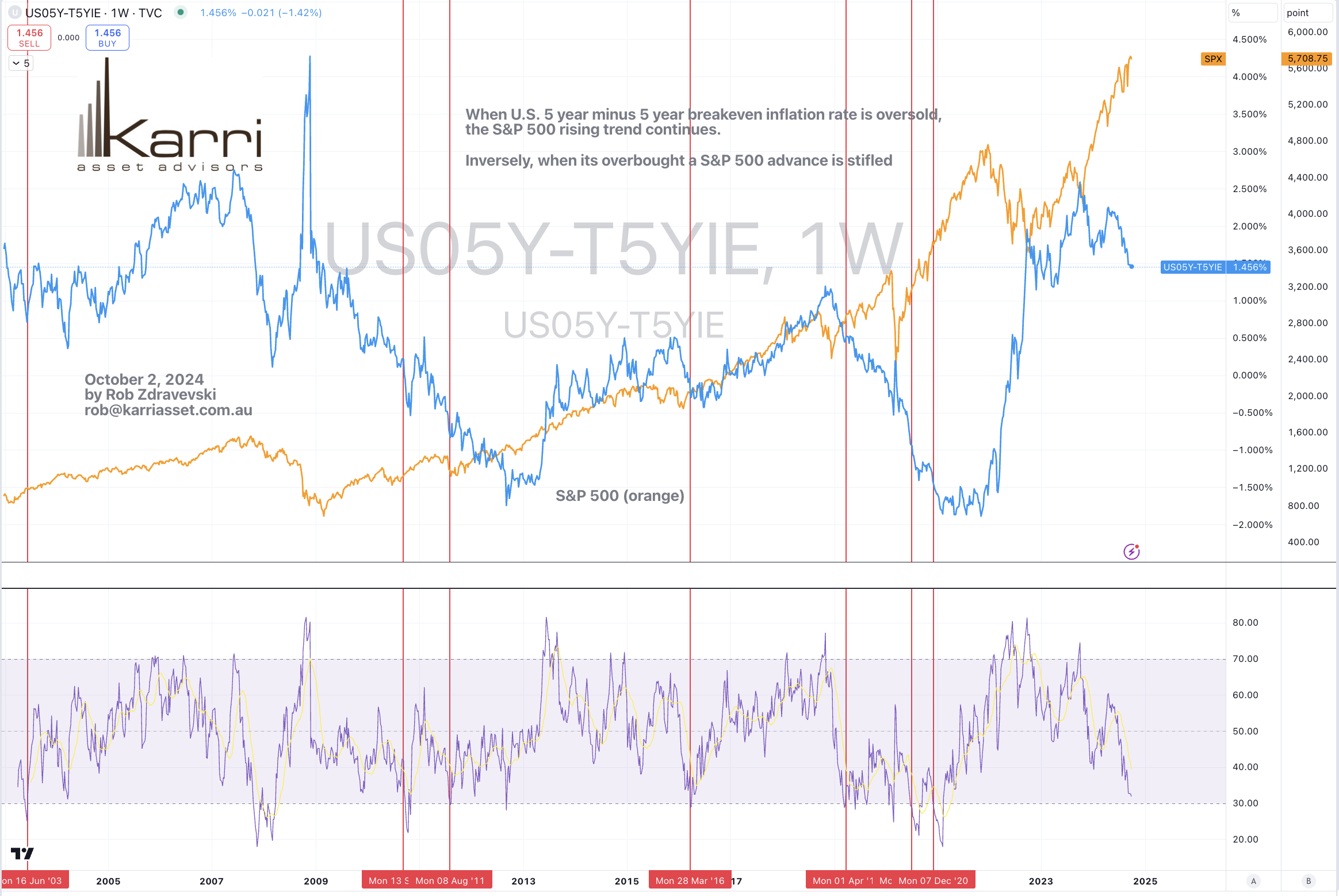

October 2, 2024 Leave a comment

Watching when the spread in the study below trades at extremes can assist validating the continuation or waning of a trend in the S&P 500.

That spread is nearing oversold territory.

October 2, 2024

October 2, 2024 Leave a comment

On the topic that new technologies (or AI, perhaps) will take away jobs….

Approximately 85% of employment growth in the last 80 years can be attributed to new technologies.

Today, nearly 60% of workers are engaged in jobs that did not exist in 194

source: The Labor Market Impacts of Technological Change: From Unbridled Enthusiasm to Qualified Optimism to Vast Uncertainty (David Autor, 2022).

October 1, 2024 Leave a comment

Broadly, interest rates (2 year government bond yields) are now between 20% and 25% below their peaks and are trading at levels last seen 18-24 months ago.

I think it’s near time for many to re-finance their debt.

From here on in, those companies still carrying much debt, better be seen to pay lower interest expenses over the coming years.

September 30, 2024 Leave a comment

This study shows the 6 times (over the past 30 years) that the U.S. inflation rate (blue line) has been oversold. It’s nearing a 7th occurrence.

It dances with the S&P 500 (orange) and the U.S. 2 year bond (green) yield.

As inflation rises, bond yields rise because bonds are being sold. This can be paraphased as an increase in #liquidity.

When bonds are sold, money tends to finds it way into equities.

In this week’s edition of Macro Extremes, the U.S. 2’s appear in the oversold category.

September 30, 2024

by Rob Zdravevski

rob@karriasset.com.au

September 29, 2024 Leave a comment

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

* denotes multiple week inclusion

Extremes above the Mean (at least 2.5 standard deviations)

Australian 10 year bond yield minus the 2 year bond yield

Australian 10 year bond yield minus the 5 year bond yield

Brazilian 10 year government bond yield

Sugar *

Silver in USD

Gold in CHF

AUD/CAD *

ZAR/USD *

AUD/INR

AUD/USD

CAD/USD

All World Developed Equities Index (ex USA)

China A50

DAX

IBEX *

South Africa 40 Index

Nasdaq Transportation Index *

And Australia’s ASX Small Caps

Overbought (RSI > 70)

SHY

U.S. 10 year minus U.S. 2 year government yield *

U.S. 10 year minus U.S. 5 year government yield *

Robusta Coffee *

Gold as priced in AUD, CAD & GBP *

MYR/USD *

THB/AUD

Budapest

Karachi

NIFTY *

SENSEX *

The Overbought Quinella (Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Arabica Coffee

Gold in EUR & USD

CNH/USD

HSCEI

Hang Seng

And the Philippines PSE Index

Extremes below the Mean (at least 2.5 standard deviations)

CAD/AUD

EUR/GBP

USD/ZAR

Oversold (RSI < 30)

U.S. and German 2 year government bond yield *

Australian Coking Coal *

U.S. Midwest Hot Rolled Coil Steel *

North European Hot Rolled Coil Steel *

Lithium Carbonate *

Lithium Hydroxide *

USD/IDR *

USD/SGD *

The Oversold Quinella (Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

U.S. 3 month bill yield

USD/CNH

Notes & Ideas:

Global government bond yields fell.

Shorter dated American and German (Euro) yields are oversold.

Japanese yields slumped more than others.

Those who bucked the declines were Chinese 10’s and Gilts across the curve.

U.S. bond yields squeezed out a small rise.

Following its central bank policy to hike rates, Brazilian 10’s ventured into overbought territory.

It’s worthy to note that the Copper/Gold ratio rallied.

The U.S. 5 year minus 5 year breakeven inflation rate is nearing an oversold extreme.

And various Australian and U.S. bond yield spreads are in this weeks list.

Equities rose again, again.

Many indices have put together a 3 week rising streak.

And we are seeing more indices entering overbought territory.

The FTSE All World Index (Developed ex USA) makes a return to the list.

Chinese and Hong Kong indices soared during the week sending them into overbought extremes.

Bangkok, Copenhagen and the ASX Financials took a break from being overbought. The latter fell 4.4% for the week.

Spain’s IBEX and Germany’s DAX are mathematically stretched.

The former has risen 7 of its past 8 weeks, amounting to an advance of 16%.

The PSE has also climbed 16% over the past 14 weeks.

Australia’s Materials Index has soared 15% over the past 3 weeks.

Singapore’s Strait Times breaks its 6 week winning streak.

And Toronto’s TSX is nearing an overbought quinella.

Commodities mostly rose.

The Bloomberg Commodity Index has risen 6.8% over the past 3 weeks.

Palladium isn’t overbought this week while Gold across various currencies remains so.

Aluminium, Iron Ore, Copper, Coffee, Dutch TTF Gas and grains had a terrific week.

Only a few commodity contracts saw declines being Crude Oil, Palladium, Rice and OJ.

Most commodities are trading at their ‘mid-points’.

Soybeans have risen for 6 consecutive weeks.

U.S. Henry Hub Natural Gas has risen 44% in its current 4 week winning streak.

U.S.Midwest Hot Rolled Coil Steel has spent 18 weeks being oversold.

And Lithium Hydroxide has now spent 63 consecutive weeks in weekly oversold territory.

Currencies once again saw most action and they feature prominently in this week’s list.

The Aussie rose again, stringing together a 3 week streak.

The Canadian Loonie was generally weaker, again. Confusing perhaps, as the decline in the CAD juxtaposed the risk-on feeling for the week.

The Euro was weaker while the Yen saw strength.

The Swiss has fallen 3 consecutive weeks agains the AUD, confirming the ‘risk-on’ mood.

The DXY is in a 4 week losing streak which helps explain USD appearing as oversold in this weeks edition.

Furthermore, the USD/SGD has fallen for 9 of the past 10 weeks.

And the British Pound registered an overbought reading against the USD.

The larger advancers over the past week comprised of;

Australian Coking Coal 1.7%, Aluminium 7.1%, Rotterdam Coal 2%, Bloomberg Commodity Index 2.1%, Baltic Dry Index 6.7%, Cocoa 8.1%, Iron Ore 11.4%, Copper 5.9%, JKM LNG 1.8%, Arabica Coffee 7.3%, Lumber 4.6%, Tin 2.1%, Newcastle Coal 4.7%, Natural Gas 11%, Nickel 2.8%, Platinum 3.1%, Shanghai Rebar 3.3%, Robusta Coffee 8.4%, Dutch TTF 9.6%, Uranium 3.2%, Corn 4%, Oats 4.8%, Soybeans 5.3%, Wheat 2%, Shanghai Composite 12.8%, CSI 300 15.7%, All World Index ex-USA 3.4%, AEX 2.2%, Budapest 1.9%, CAC 3.9%, China A50 18.9%, DAX 4%, DJ Transports 2.7%, MIB 2.9%, HSCEI 14.4%, Hang Seng 13%, IBEX 1.8%, MOEX 2.7%, TAIEX 3%, KOSPI 2.2%, FTSE 250 2%, Nikkei 225 5.6%, Helsinki 4.2%, Stockholm 2.3%, PSE 2.8%, South Africa 4.9%, SMI 2.5%, SOX 4.3%, Chile 3%, Tel Aviv 4.9%, WIG 3.9%, ASX Materials 9.4% and the ASX Small Caps rose 2.8%.

The group of largest decliners from the week included;

WTI Crude Oil (4%), Orange Juice (4.2%), Palladium (5.1%), Gasoline (4%), Brent Crude Oil (3.7%), Rice (3.1%), KRE Regional Banks Index (3.1%), Nasdaq Biotechs (2.7%), Copenhagen (1.3%), Strait Times (1.4%) and the ASX Financials slumped 4.4%.

September 29, 2024

by Rob Zdravevski