A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

* denotes multiple week inclusion

Extremes above the Mean (at least 2.5 standard deviations)

Belgian, Danish and Finnish 10 year government bond yields *

IEF & IEF *

SHY & TLT *

U.S. 10 year minus U.S. 2 year government bond yield spread *

U.S. 10 year minus U.S. 5 year government bond yield spread *

U.S. 30 year minus U.S. 10 year government bond yield spread *

Gold Volatility Index

Dutch TTF Gas

Gold in AUD

CHF/AUD *

CHF/USD *

CNH/USD *

EUR/AUD

EUR/USD

THB/USD *

USD/CAD *

USD/DKK

USD/INR

USD/MXN

Overbought (RSI > 70)

None

The Overbought Quinella (Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

MYR/USD *

Extremes below the Mean (at least 2.5 standard deviations)

German 2, 5 and 10 year bond yields

Australian 2, 3, 5 & 10 year bond yields

British 2, 3, 5 & 10 year bond yields

5 year Japanese bond yields

10 year Austrian, Swiss, Czech, Spanish, South Korean, Dutch, Norwegian, New Zealand, Polish, Portuguese and Swedish government bond yields.

U.S. 2, 5, 7, 10, 20 and 30 year government bond yields

TBT & TBX *

U.S. 5 year bond yield minus the 5 year break-even inflation rate *

U.S. 5 year bond yield minus the 3 month break-even inflation rate *

U.S. 5 year bond yield minus the U.S. inflation rate *

U.S. 10 year bond yield minus the 10 year break-even inflation rate *

U.S. 10 year bond yield minus the U.S. inflation rate *

Bloomberg Commodity Index

S&P GSCI Index

Brent Crude Oil

AUD/INR

AUD/JPY

AUD/SGD

AUD/THB *

CAD/EUR *

EUR/JPY

GBP/JPY

USD/CHF

DXY (USD) Index

Chile’s IPSA Index

Tel Aviv 35

Poland’s WIG

ASX Materials

AEX

Austria’s ATX

CAC

DAX

MIB *

IBEX

KOSPI

S&P MidCap 400

Copenhagen

Helsinki

Stockholm

Russell 2000 Index

Oversold (RSI < 30)

Cotton *

North European Hot Rolled Coil Steel *

U.S. Midwest Hot Rolled Coil Steel *

Shanghai Rebar *

Lithium Hydroxide *

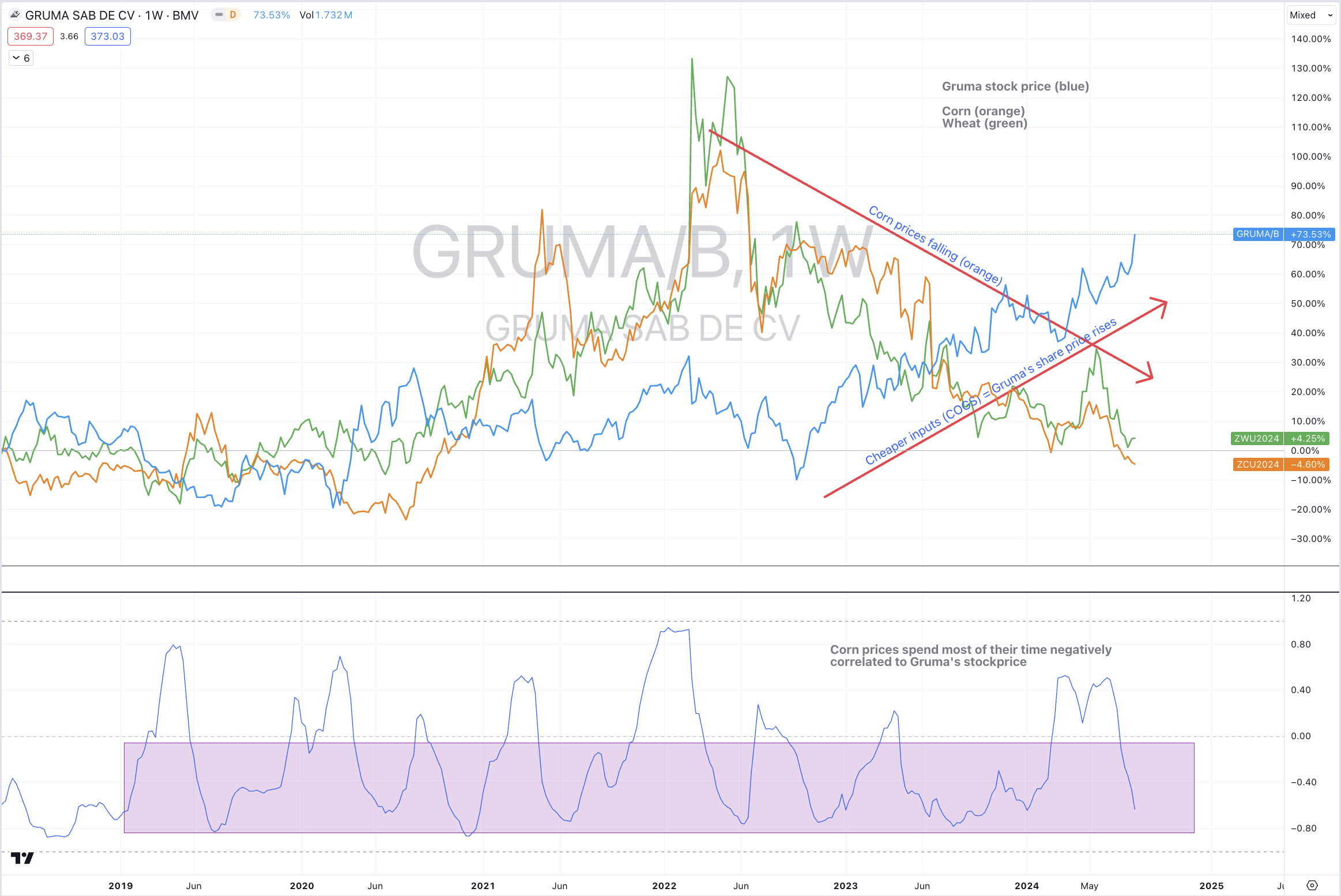

Corn *

Soybeans *

BRL/USD *

The Oversold Quinella (Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

Australian Coking Coal

China Coking Coal

Notes & Ideas:

Government bond yields rose, which broke many declining streaks.

The exception were Finnish, Japanese, Chilean and Brazilian yields.

The misnomer in this weeks edition is that intra-week yields did trade to oversold extremes before reversing higher and many closing above last weeks close.

U.S. inflation breakeven inflation rates also rose.

The Copper/Gold ratio is in a 5 week losing streak.

And we are seeing divergence in Chilean yields. The 2 year yield has risen for 8 straight weeks while the 10 year yield has fallen for 6 consecutive weeks.

Amazingly, most equity indices closed either flat or rose for the week.

There are no equity indices in overbought territory this week, however of the many appearing in the oversold category, did so due to their intra-week swoons.

The major Indian indices are no longer overbought.

Australian indices were amongst the rare losers for the week as were selected Asian markets.

The Nasdaq 100 rose 0.4% for the week which was enough to break its 4 week long streak.

The KOSPI is in a 5 week losing streaks.

And the Nikkei 225 has declined 17% over the past 4 weeks, keeping it in a 4 week losing streak.

Commodities were mixed, although generally posting gains which is change of a few weeks of broader weakness.

Oil, Cocoa, Lumber Thermal (again) Tin, Gasoline and Gases had a good week.

All things steel related are in a trough.

Coking Coal prices are unloved.

Silver, Grains, Copper, Platinum and Lean Hogs were weaker.

I’m very happy to see cheaper bacon prices.

Sugar broke its 5 week losing streak.

Copper and Iron Ore prices have fallen for 5 and 6 straight weeks, respectively.

Copper has declined 15% over the past 6 weeks.

While Crude Oil and Palladium broke their 4 week losing streaks.

Worthy of note, is the forward contract month for Henry Hub Natural Gas bounced out of oversold territory.

And Lithium Hydroxide has now spent 56 consecutive weeks in weekly oversold territory.

Currencies continue to provide action, again and again.

The Aussie was mostly higher thus breaking its losing streak against most currencies.

The anomaly is its 4 week losing streak versus the Loonie.

The ‘mid-week’ Aussie strength was commensurate with the rising fortunes for equities and an analogy for ‘risk-on’.

In the meantime, the AUD mean reverted against the Yen.

The Loonie saw strength and as a result it broke its 6 week losing streak agains the Euro.

In fact, many streaks were broken this week.

The British Pound fell and extended its losing streak against the USD to 4 weeks.

Brazil’s Real bounced out its stay in oversold land

The GBP/JPY have fallen for 5 straight weeks.

And as pre-empted in last weeks edition, the DXY Index did trade to 2.5 standard deviations below its 20 week average.

The larger advancers over the past week comprised of;

Cocoa 24.2%, WTI Crude Oil 4.5%, Coffee 2.5%, Lumber 4.2%, JKM LNG 3.2%, Tin 2.5%, Newcastle Coal 3.3%, Natural Gas 9%, Palladium 1.6%, Gasoline 3.1%, Robusta Coffee 2.3%, Sugar 2.1%, LME Tin 3.9%, S&P GSCI 1.7%, CRB 2.2%, Dutch TTF Gas 10.2%, Brent Crude 3%, BOVESPA 3.8%, Mexico 1.6% and Philadelphia’s SOX Index rose 2.2%.

The group of largest decliners from the week included;

Australian Coking Coal (5.5%), China Coking Coal (5.4%), Lean Hogs (2.6%), Copper (2.7%), Lithium (2%), Platinum (3.9%), Silver in AUD (4.8%), Silver in USD (3.9%), Corn (2.5%), Oats (2%), Soybeans (2.4%), Egypt (2.1%), KRE Regional Bank Index (1.9%), KOSPI (3.3%), Nikkei 225 (2.5%), Russell 2000 (1.4%), SENSEX (1.6%), Strait Times (3.5%), WIG (2.5%), ASX Financials (2.6%), ASX 200 (2.1%), ASX Materials (2.5%), ASX Small Caps (3.5%) and Turkiye’s BIST fell 5.4%.

August 11, 2024

by Rob Zdravevski

rob@karriasset.com.au