Biden will save the day

February 21, 2022 Leave a comment

Russia says they will not invade Ukraine and are open to using diplomacy while America says they will invade and are poised to do so very soon.

I believe Russia will not initiate an invasion.

Firstly, Putin doesn’t have the money nor the troops.

Also, you don’t invade in the mud. You wait until the ground has dried.

However, Russia will retaliate and blame NATO if they throw the first stone.

Russia may already have a claim if they cite the threats of sanctions.

For the U.S. has already sanctioined companies involved in the NordStream 2 pipeline. Germany isn’t happy.

An outlier call is that Russia walks across the border and Ukraine accepts their terms of a ‘merger’.

My belief is that Biden is ‘creating a war’ for various reasons. He needs to improve his fall in the polls and he’ll do that by being tough on Russia (and China) while also increasing government spending.

Remember than Obama was softer and friendlier to Russia, which included assisting Russia joining the WTO in 2012.

Obama was also continuing the austerity measures adopted at the end of the Global Financial Crisis.

The Democrats lost heavily in the 2014 midterm elections and Biden has not forgotten Obama’s soft and friendly stance.

With Biden’s infrastructure spending bill not being passed, another way he can spend money is to increase military expenditures, especially as the Iraq and Afghanistan campaigns have ended.

The charts below show the ebbs of current U.S. military spending in the form of 1) as a percentage of GDP and 2) as a percentage of general government expenditure.

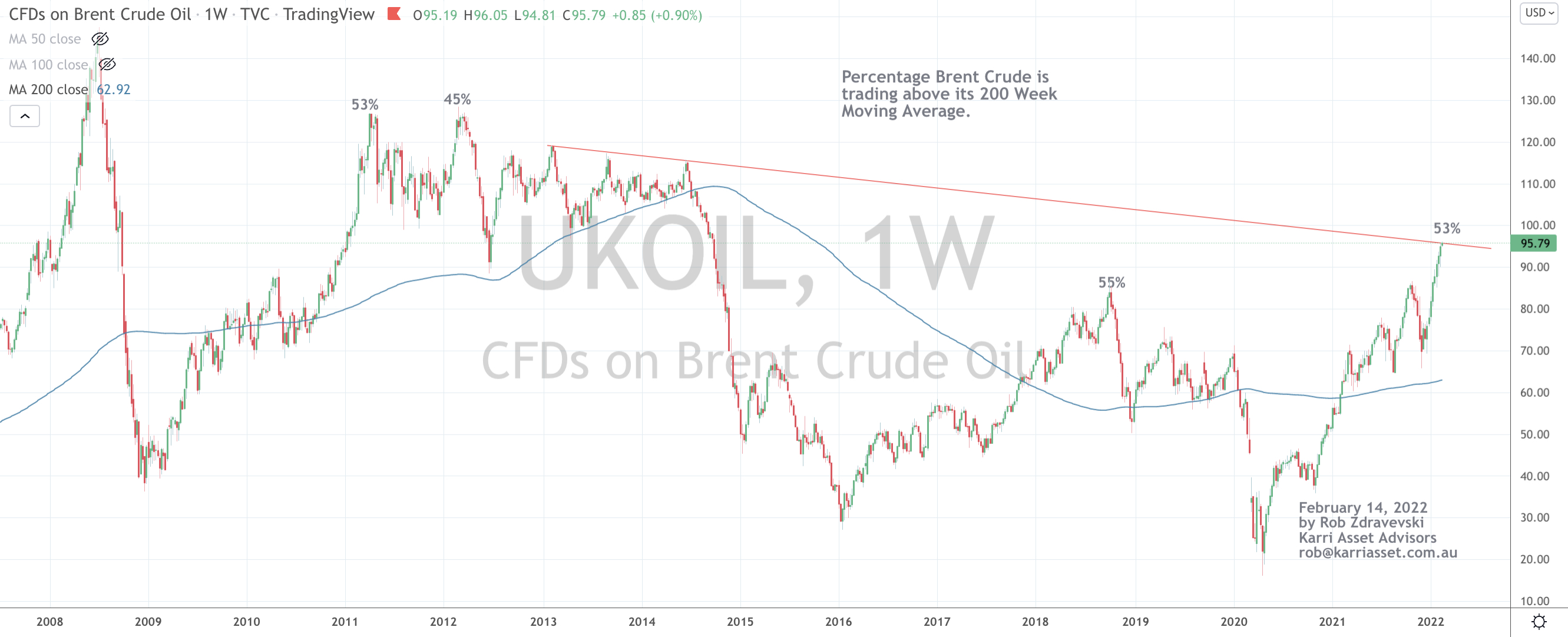

Beyond flooding his mates in Ukraine with more American weapons and ammunition, other incentives for Biden to cite that a war is imminent is that he’ll be able to blame Russia’s aggression for the higher oil and gasoline prices his citizens are experiencing.

(It’s also plausible Ukraine has some ‘dirt’ on the Biden’s too)

In turn, higher energy prices creep into corporate operating costs which may lead into a lower GDP figure in the coming quarters.

Then corporations can also be blamed for passing on higher costs.

The main point is that Biden isn’t blamed for rising costs and inflation because he really needs to wins these mid-term elections in December.

Also, have you noticed France’s involvement in trying to broker talks.

In 2019, Macron declared NATO brain-dead.

Today, Macron has ‘arranged’ for a summit between Putin and Biden.

In the interim, I am surprised by Blinken’s rhetoric recently changing from pacifist to belligerent, to side more with Biden’s stance.

This is contrary to the paper Blinken wrote in 1987, titled Ally vs Ally.

Should Biden ‘negotiate a retreat’, he will certainly take credit for his toughness hoping this elevates his standing in the polls.

Although, if a war does eventuate, it’ll be brought to you by CBS News, CNN and the lobbyists for various U.S. military manufacturers and suppliers.

February 21, 2022

by Rob Zdravevski

rob@karriasset.com.au