A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

- denotes multiple week inclusion

Extremes “above” the Mean (at least 2.5 standard deviations)

Australian 2, 3, 5 & 10 year government bond yields *

Japanese 2 year government bond yield

South Korean 10 year government bond yield *

Copper/Gold Ratio

U.S. 5 year government bond yield minus U.S. 5 year inflation breakeven rate *

Newcastle Coal

Oats

AUD/IDR *

AUD/THB *

Hang Seng China Enterprises Index (HSCEI) *

Hang Seng Index *

J’burg 40

Singapore Straits Times Index *

Overbought (RSI > 70)

Russian 10 year government bond yield

AEX

Budapest

Malaysia’s KLSE *

Pakistan’s KSE Index *

FTSE 250

and Turkiye’s BIST 100 *

The Overbought Quinella (Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

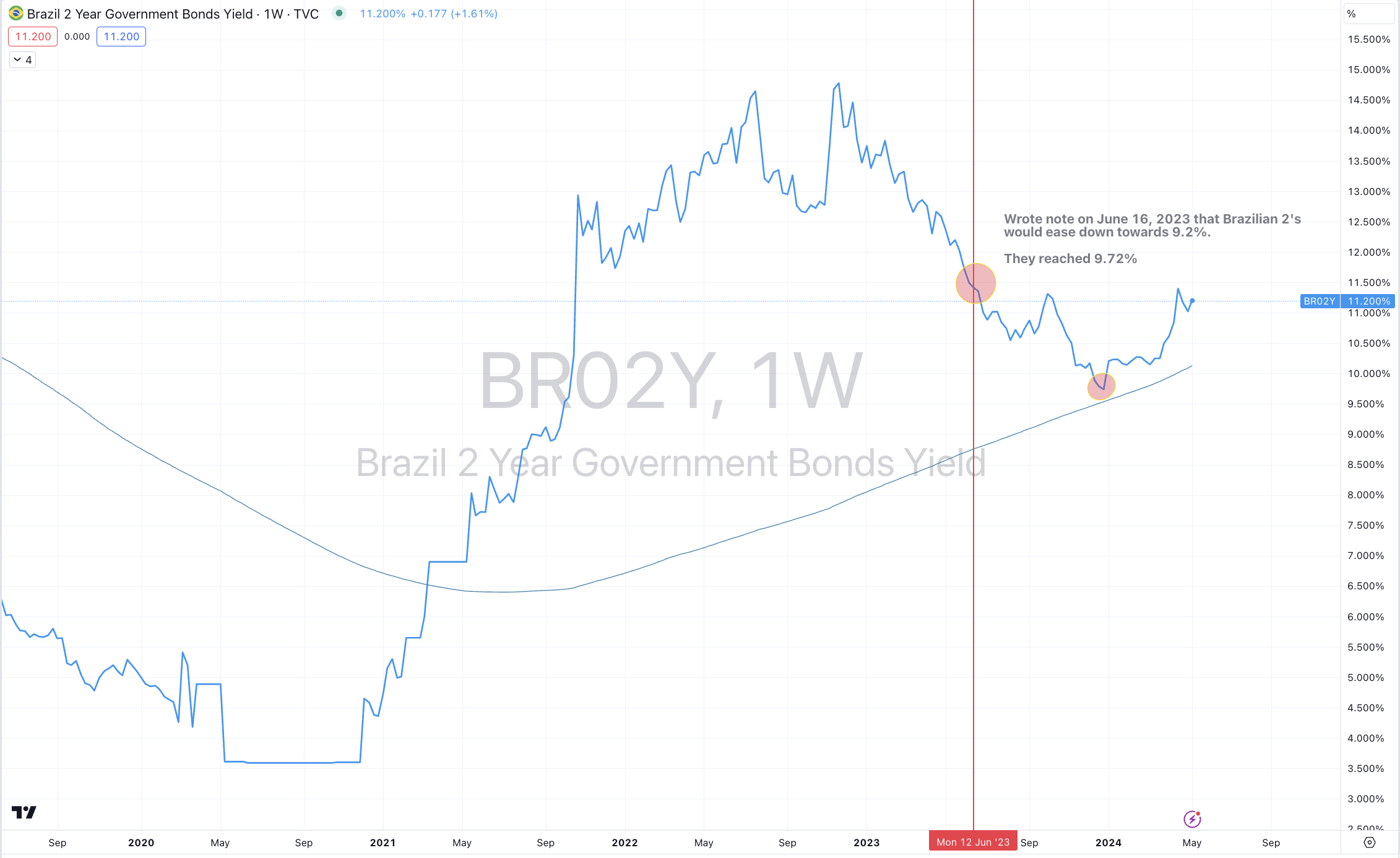

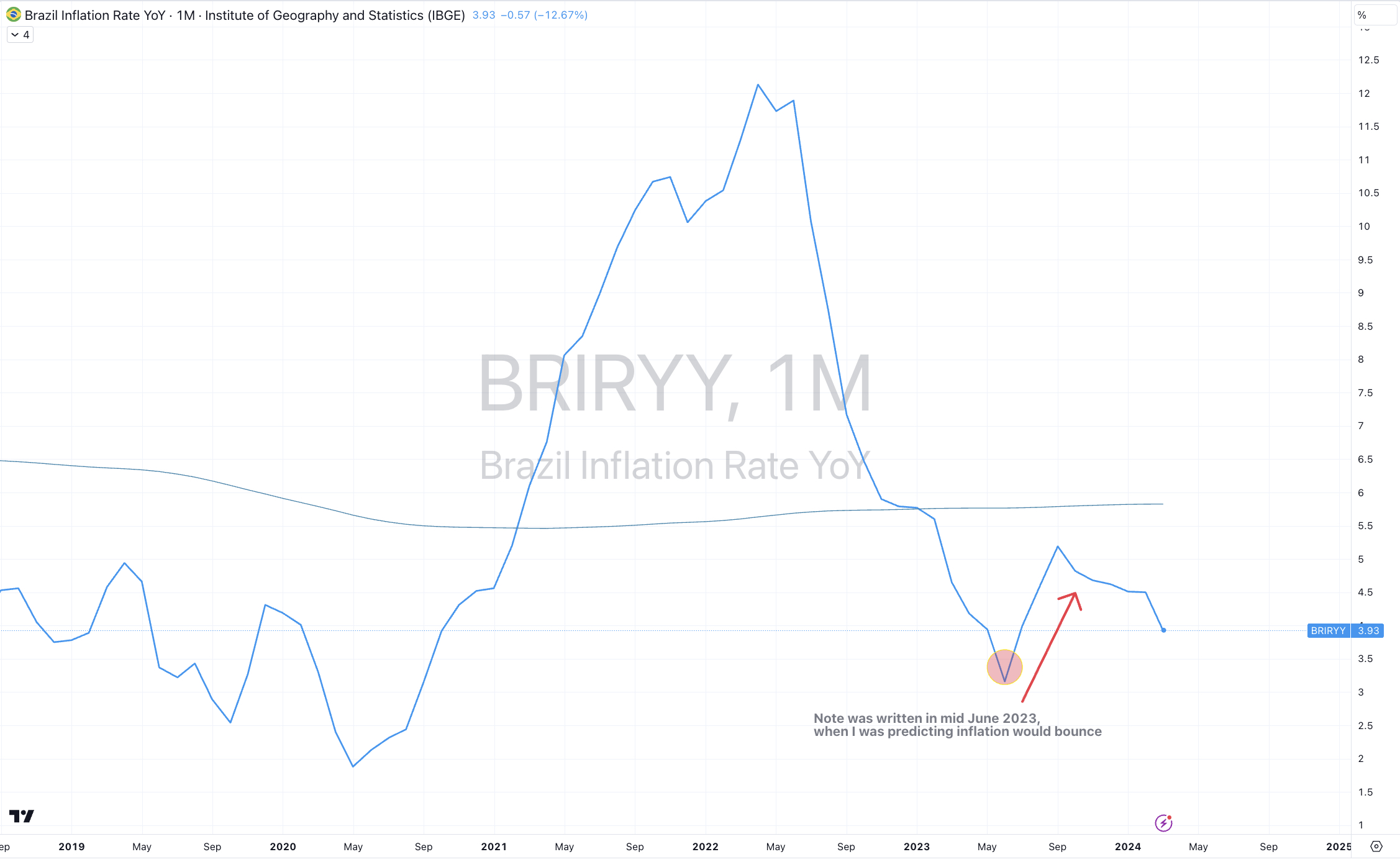

Brazilian 10 year government bond yields

Copper

Extremes “below” the Mean (at least 2.5 standard deviations)

SHY

PHP/USD *

Dow Jones Transports *

And Indonesia’s IDX30 *

Oversold (RSI < 30)

Lithium Hydroxide

North European Hot Rolled Coil Steel

The Oversold Quinella (Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

Lumber

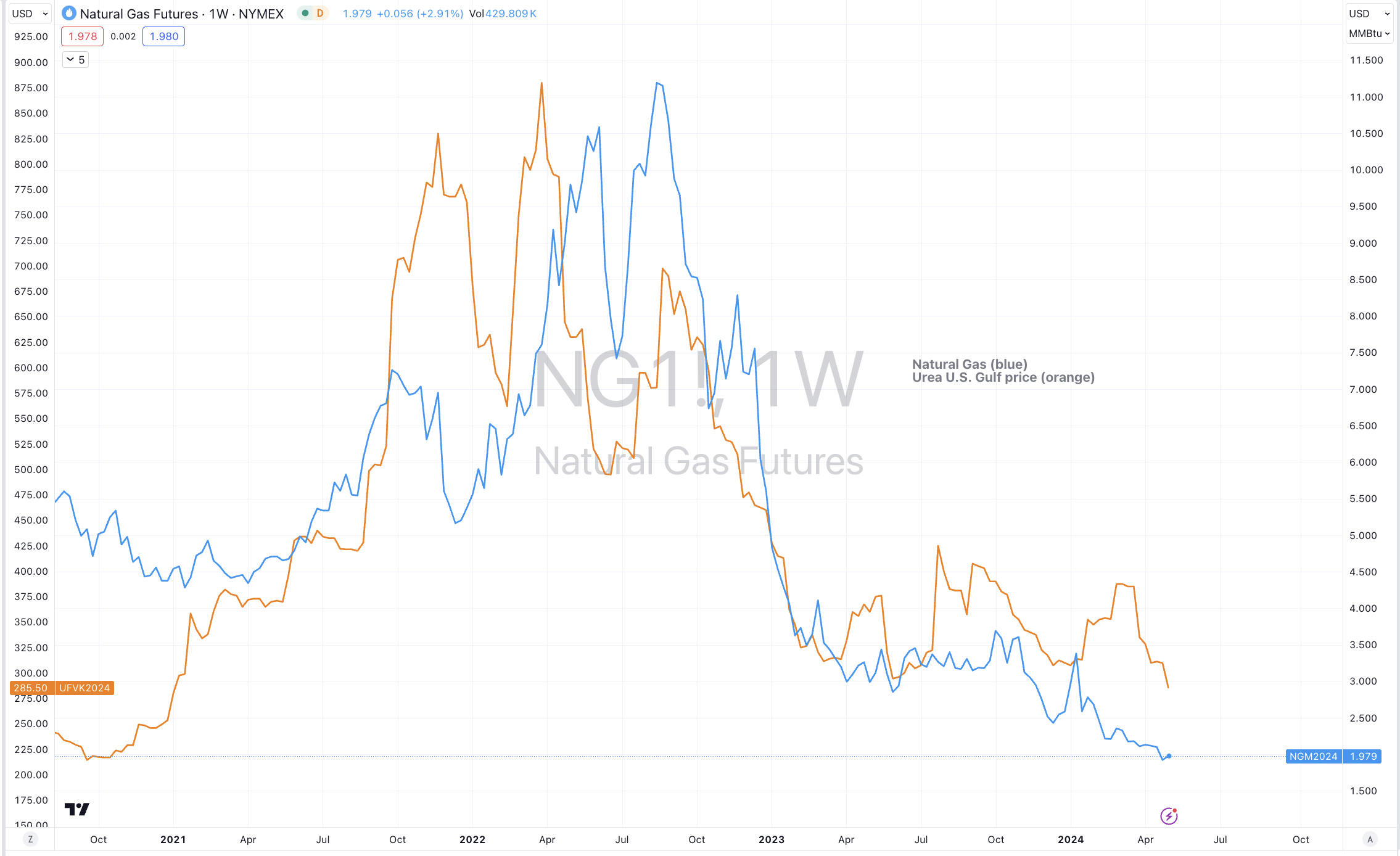

Urea

Notes & Ideas:

Government bond yields fell.

Many streaks were broken such as the 5 week winning streak in Canadian and South Korean 10’s along with all the yields across the British curve.

Chinese 10 year bond yields is no longer oversold as its yield rose.

Equities were mostly higher.

However, selected European bourses did see weakness.

China’s A50 Index and the U.S. KBW Bank Index have risen 7.5% and 5.2% respectively, over the past 3 weeks.

IBEX, MIB, & Stockholm’s OSX 30 aren’t overbought anymore.

The HSCEI and Hang Seng both rose 4.5% for the week, adding to last week’s 9% advance.

Furthermore, the Hang Seng and U.S. (KRE) Regional Banks Index are in a 3 week winning streak.

The SOX finished flat following last week’s stunning 10% rise.

Karachi broke its 6 week winning streak.

The Nasdaq Transports has declined for 5 consecutive weeks.

And Toronto’s TSX registered a bearish outside reversal week.

Commodities were mostly lower, again.

Weakness was seen in Cocoa, Coffee, Precious Metals, Oils and Distillates.

Strength was evident in Base Metals, Coal, Gases and Grains.

Some of the grains have strung 3 weeks of consecutive gains.

Aluminium, Tin & Nickel are not overbought anymore, nor is Cocoa, Coffee or Gold (in any currency).

Cocoa has fallen 31% in the past fortnight and has broken its overbought streak of 27 weeks.

While Australian Coking Coal isn’t oversold this week.

Robusta Coffee has fell 15% accounting for nearly half of the 39% rise seen in the prior 9 weeks.

Cotton has fallen for 8 consecutive weeks while Rubber has sunk for 6 weeks straight.

Iron Ore in a 5 week winning streak.

U.S. Hot Rolled Coil Steel performed a bearish weekly outside reversal.

And Lithium Hydroxide has now spent 42 consecutive weeks in weekly oversold territory.

Currencies are providing stealth guidance for the health of various asset trends.

The big news was the strength in the Japanese Yen and it’s no longer at last weeks extremes.

The AUD rose against all except the Yen.

The Canadian Loonie fell while the Euro was mixed.

The British Pound fell with the exception of the USD pair.

The Thai Baht broke its 7 week losing streak against the USD.

And the USD/SEK registered a outside weekly bearish week.

The larger advancers over the past week comprised of;

Australian Coking Coal 3.2%, Baltic Dry Index 9%, China Coking Coal 4.7%, Tin 2%, Newcastle Coal 5.8%, Natural Gas 11.4%, Platinum 4.7%, Dutch TTF Gas 5.5%, Uranium 5.5%, Corn 2.3%, Oats 7.9%, Soybeans 3.2%, China A50 2%, HSCEI 4.4%, Hang Seng 4.7%, Russell 2000 1.8%, KRE Regional Bank Index 3%, FTSE 250 1.7%, Nasdaq Biotechs 5.9%, Chile 2.6% and the BIST 100 rose 3.6%.

For reference, the S&P 500 rose 0.6% for the week.

The group of largest decliners from the week included;

Aluminium (1.9%), Cocoa (23.1%), WTI Crude (6.9%), Cotton (3.5%), Lean Hogs (2%), Heating Oil (4.7%), Coffee (Arabica) (10.4%), Lumber (2.7%), Lithium (5.7%), Gasoline (6.9%), Coffee (Robusta) (14.7%), SPGSCI (3.8%), CRB Index (3.5%), Brent Crude Oil (6%), Gasoil (5.3%), Urea Middle East (2.1%), Silver in AUD (3.6%), Silver in USD (2.4%), Gold in AUD (2.7%), Gold in CHF (2.6%), Gold in EUR (2.2%), Gold in GBP (2%), Gold in ZAR (3%), CAC (1.6%), MIB (1.8%) and Spain’s IBEX fell 2.7%.

May 5, 2024

by Rob Zdravevski

rob@karriasset.com.au