Latest newsletter summarises my inflation playbook

June 16, 2026 Leave a comment

Trying to hear what's not being said

June 16, 2026 Leave a comment

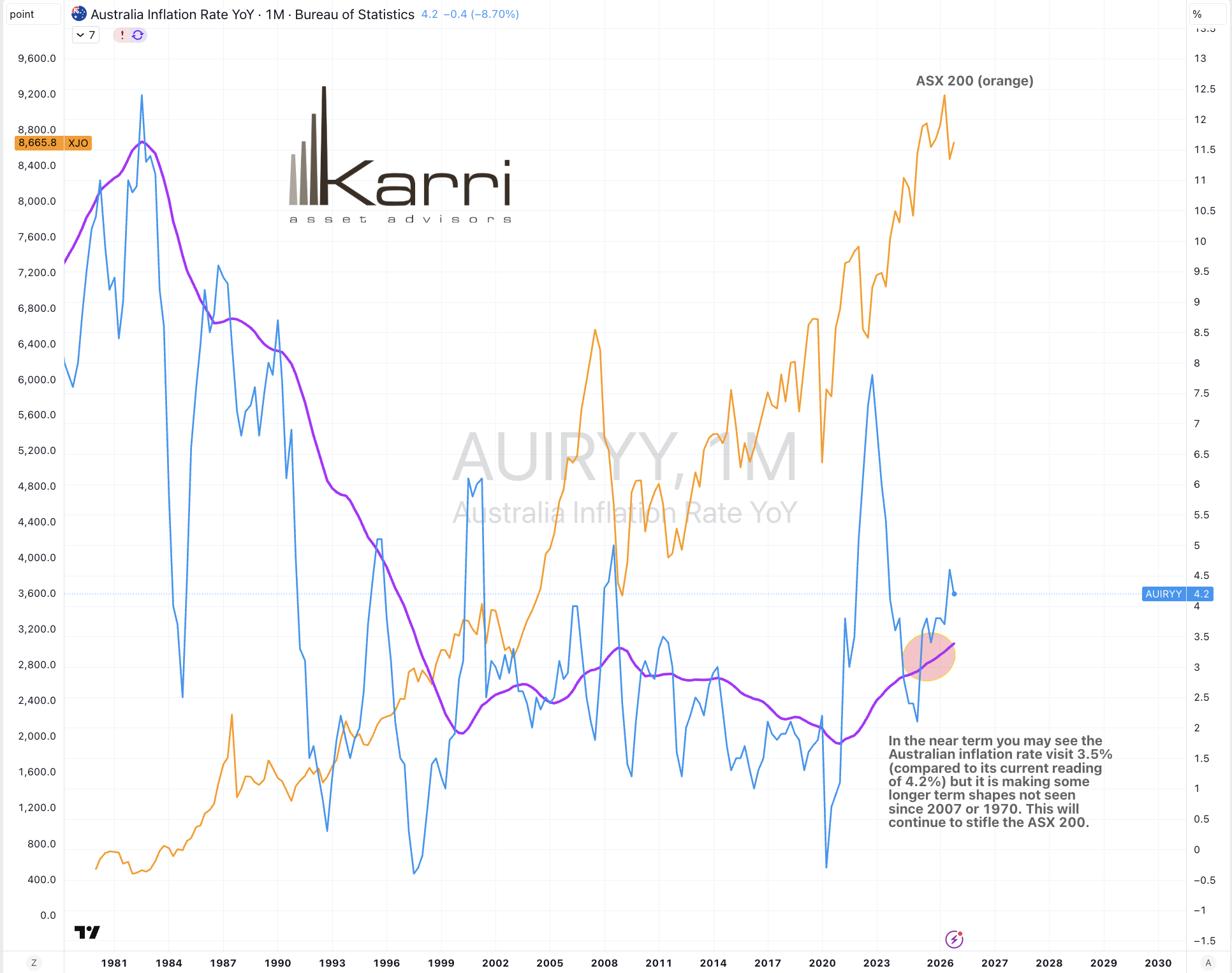

The Australian inflation rate is making similar ‘shapes’ that I’m seeing in the U.S.

June 16, 2026

June 15, 2026 Leave a comment

Accenture’s share price is trading at an extreme never seen before.

June 15, 2026

June 14, 2026 Leave a comment

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

n.b. pricing of (commodity) futures contracts is only considering the immediate front month.

* denotes multiple week inclusion

Extremes above the Mean (at least 2.5 standard deviations)

U.S 3-month bill yield

U.S. 5-year bond yield minus U.S. 5-year breakeven inflation rate

COP/USD

AEX

Overbought (RSI > 70)

Japanese, Russian & Korean 10-year government bond yields *

JKM LNG

Rubber *

AUD/IDR *

CNH/USD

Austria’s ATX Index

Dow Jones Transports

Italy’s MIB

S&P Small Cap 600

TAIEX *

South Korea’s KOSPI *

Nikkei 225 *

Thailand’s SET Index *

SOX *

And Poland’s WIG Index

The Overbought Quinella (Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Copper/Gold Ratio

Indonesian 10-year bond yield

USD/IDR *

Extremes below the Mean (at least 2.5 standard deviations)

Platinum

Gold priced in CAD, CHF, EUR, GBP, USD and ZAR

Corn *

MYR/USD

Hang Seng Index

Oversold (RSI < 30)

U.S. 10 year minus U.S. 5-year govn’t bond yield spread *

U.S. 10 year minus U.S. inflation rate

North European Hot Rolled Coil Steel *

The Oversold Quinella (Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

IDR/USD

Lean Hogs

Notes & Ideas:

Government bond yields fell,

As did U.S. corporate bond yields

Chilean 2-year bond yield has declined for 5 weeks.

The U.S. 10 year minus U.S. 10-year inflation breakeven spread is nearing overbought territory.

The U.S. 5 year and 10-year inflation breakeven rates have fall for 4 weeks.

The latter finally mean reverted.

The U.S year minus U.S. inflation rate mean reverted last week.

Inversely, the U.S. 2 year rose to complete its mean reversion.

Japanese 30-year yields have sunk for 4 weeks.

Brazilian 10‘s are no longer overbought.

And Chinese 10-year yield rose and broke 4 weeks of decline.

Equities were mostly higher.

Shanghai Composite and Indonesia’s IDX rose to snap 4 weeks of losses.

Vietnan’s VN Index is in a 4-week losing streak.

The Hang Seng have fallen for 5 weeks.

The KBW Banks Index, CAC, KRE Regional Banks, Nasdaq Transports and Dow Jones transports have climbed for 4 weeks.

The Dow Jones Transports has climbed 11.6% in 4 weeks.

Thailand’s SET is in a 7-week winning streak.

While Brazil’s BOVESPA rose and broke its 8-week losing streak.

Commodities had a bias for weakness, again.

Copper, Coffee, Lumber and Lithium were the notable gainers.

Coal, Oil, Gases, Distillates, Nickel, Gold and Urea were amongst the decliners.

Bloomberg Commodity Index, S&P GSCI, CRB Index and Lean Hogs have fallen for 4 weeks.

Cotton, Platinum and Gold price in ZAR have declined for 5 weeks.

Aluminium, Rotterdam Coal and Cotton are in 4-week winning streaks.

Australian Coking Coal fell and snapped a 7-week winning streak and is no longer overbought.

Iron Ore prices eked out a gain to break 5 weeks of weakness.

Lean Hogs have fallen for 5 of the past 6 weeks.

North European Hot Rolled Coil Steel has declined for 7 straight weeks.

And U.S. Gulf Urea prices are in an 8-week losing streak.

Currencies were quiet, again.

The Aussie was mixed to lower.

The Loonie was weaker.

COP/USD has risen for 4 weeks.

Euro and British Pound rose.

Yen was mixed, while the JPY/USD rose to break 4 weeks of losses.

And the USD was mostly stronger.

The larger advancers over the past week comprised of;

Copper, 2.6%, Arabica Coffee 4.4%, Lumber 2.6%, Lithium Carbonate 2.5%, Orange Juice 2.5%, Palladium 2.2%, Robusta Coffee 8.4%, Sugar #16 4.3%, AEX 2.9%, ATX 2.9%, BKX 3.4%, CAC 1.6%, China A50 1.8%, IDX 7.4%, DFM 3.2%, DJ Transports 3.1%, MIB 3.2%, IBEX 2.3%, S&P Small Cap 600 4.4%, Dublin 2.9%, Russell 2000 4%, KRE 4.6%, S&P Midcap 400 2.8%, Mexico 2.7%, NBI 1.7%, Nasdaq 100 2.3%, Portugal 1.8%, Sensex 1.7%, SMI 2.4%, SOX 9.4%, IGPA 5.7%, Euro Stoxx 50 2.1%, TA-35 1.8%, Nasdaq Transports 3.3%, TSX 1.5%, WIG 3%, XBI 4%, ASX 200 2.1%, ASX Industrials and Türkiye’s BIST rose 1.8%.

The group of largest decliners for the week included;

Australian Coking Coal (3%), Richards Bay Coal (2.6%), Aluminium (2.4%), Rotterdam Coal (2.2%), Bloomberg Commodity Index (2.4%), Brent Crude (6.2%), Baltic Dry Index (5.5%), WTI Crude (6.3%), Palm Oil (1.7%), Heating Oil (5.4%), Tin (5.4%), Newcastle Coal (1.7%), Natural Gas (3.4%), Nickel (4.2%), Platinum (4.8%), Sugar (3.1%), S&P GSCI (3.8%), CRB Index (2%), Dutch TTF Gas (3.6%), Urea U.S. Gulf (5.1%), Gasoil (8.4%), Urea Middle East (8.5%), Gold in AUD (2.5%), Gold in CAD (2.2%), Gold in CHF (2.4%), Gold in EUR (2.9%), Gold in GBP (3%), Gold in USD (2.5%), Gold in ZAR (4.2%), Oats (2.1%), Rice (2.9%), EGX (3.5%), FCATC (2.4%), TAIEX (2%), Helsinki (2.1%) and Vietnam’s VN Index fell 2.6%.

June 14, 2026

By Rob Zdravevski

rob@karriasset.com.au

June 13, 2026 Leave a comment

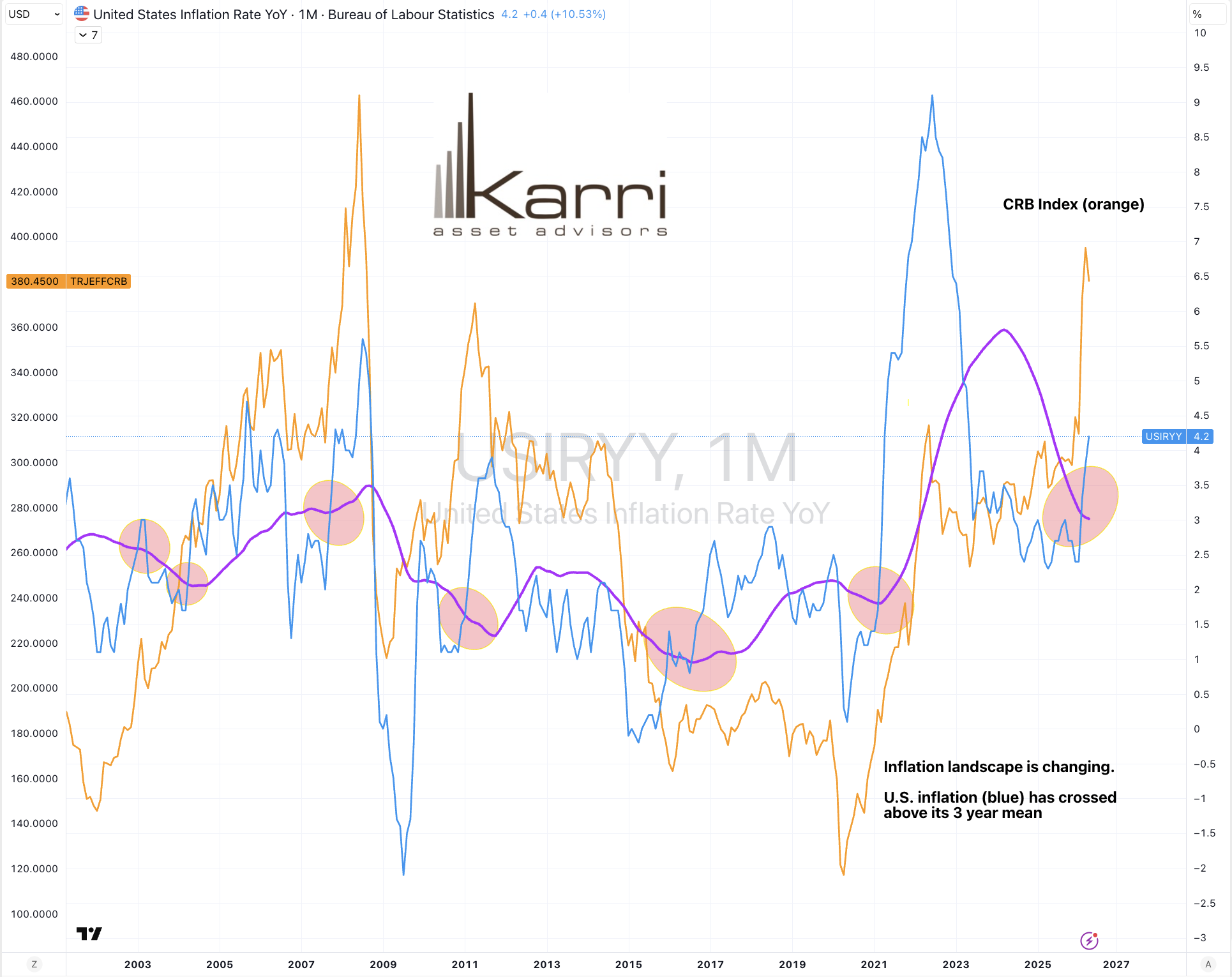

This study shows when the U.S. inflation rate crosses above its 3 year mean, commodity prices get a wriggle on….

June 13, 2026

June 9, 2026 Leave a comment

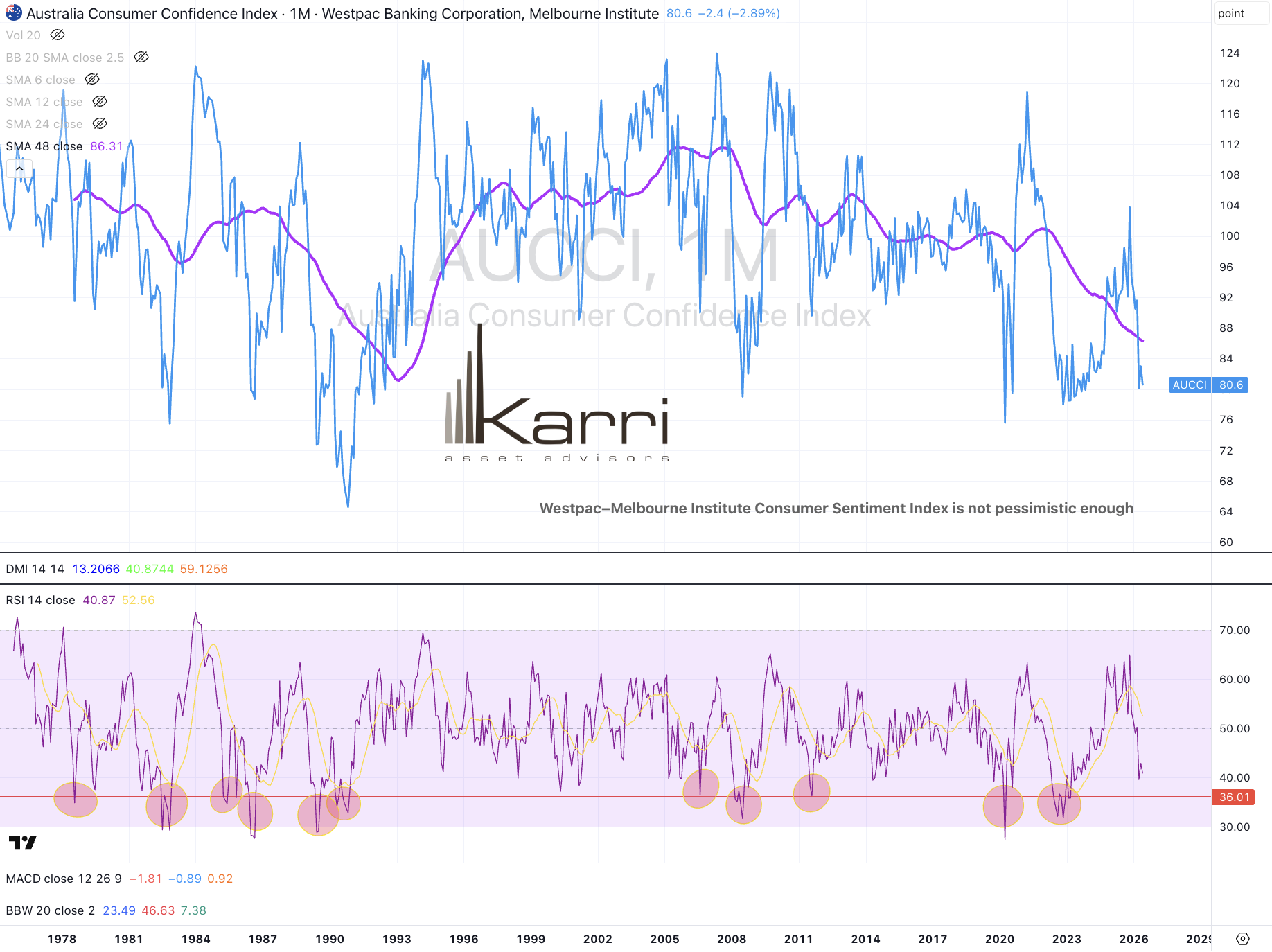

The news says…..the Westpac–Melbourne Institute Consumer Sentiment Index declined 2.9 per cent to 80.6 in June 2026.

So what!

It’s not the notional number that’s of interest.

Australian Consumer Sentiment as measured by this survey, isn’t pessimistic enough.

June 9, 2026

June 9, 2026 Leave a comment

This chart of the #KOSPI tells me when not to chase. I’ve missed plenty but I won’t buy something which I have no business buying, especially when the shape looks like this.

Who were the investors, allocators, speculators (and why) buying this index over the past few months?

Bless them for being profitable but the extremes suggest “look out below”.

And some may ponder the antithesis and better probability of being short the KOSPI…..

by Rob Zdravevski

rob@karriasset.com.au

June 9, 2026

June 8, 2026 Leave a comment

Put aside all the narratives from the storytellers, Bitcoin (in USD) eased on down to kiss its long term mean.

It’s just what prices do !

See my April 29th post https://robzdravevski.com/2026/04/29/bitcoins-correlation-to-risk-on-off-continues/

or my February 6th post https://robzdravevski.com/2026/02/06/bitcoin-is-near-to-some-mean-reversion/

June 8, 2026

June 7, 2026 Leave a comment

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

n.b. pricing of (commodity) futures contracts is only considering the immediate front month.

* denotes multiple week inclusion

Extremes above the Mean (at least 2.5 standard deviations)

Brazilian 10 year bond yield

Copper/Gold Ratio

U.S. 5 year bond yield minus U.S. 5 year breakeven inflation rate

Copper

USD/KRW

Singapore’s Strait Times Index *

Overbought (RSI > 70)

Japanese & Korean 10-year government bond yields *

Richards Bay Coal

Aluminium *

Rubber *

AUD/IDR *

TAIEX *

Finland’s OMX-H *

And Thailand’s SET Index *

The Overbought Quinella (Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Australian Coking Coal *

USD/IDR *

KOSPI *

Nikkei 225 *

SOX *

Extremes below the Mean (at least 2.5 standard deviations)

U.S. 30 year minus U.S. 10-year govn’t bond yield spread *

Corn

Oversold (RSI < 30)

U.S. 10 year minus U.S. 5-year govn’t bond yield spread *

North European Hot Rolled Coil Steel *

Indonesia’s IDX Composite Index *

The Oversold Quinella (Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

IDR/USD

Notes & Ideas:

Government bond yields rose.

Except for Chilean 2’s, Japanese and Turkish 10’s and Japanese 30’s.

Chilean 2-year bond yield has declined for 4 weeks.

And the U.S. 10 year minus U.S. 5-year yield spread rose and broke a 5-week losing streak.

Equities were weaker.

Many more indices have exited the overbought list.

Shanghai Composite, IDX and the Hang Seng have fallen for 4 weeks.

Indonesia’s IDX has declined for 7 weeks.

The Dow Jones Transports has climbed 8.5% in 3 weeks.

Thailand’s SET is in a 6-week winning streak.

The S&P 500 fell and broke its 9-week winning streak.

While Brazil’s BOVESPA is in a 8 week losing streak.

Commodities had a bias for weakness, again.

Coal, Crude Oil, LNG, Lumber and Distillates were the notable gainers.

Precious Metals, Lithium, Coffee, oats, Corn and Shipping Rates were amongst the decliners.

Aluminium, Rotterdam Coal and Cotton are in 4-week winning streaks.

Australian Coking Coal has climbed for 7 weeks.

Platinum, Silver and Gold have declined for 4 weeks.

Iron Ore prices have sunken for 5 weeks.

Lean Hogs have fallen for 5 of the past 6 weeks.

North European Hot Rolled Coil Steel has declined for 6 straight weeks.

And U.S. Gulf Urea prices are in a 7-week losing streak.

Currencies were quiet.

The Aussie fell.

The Loonie was mixed, again.

CHF/JPY fell and snapped its 4-week winning streak.

CNH/USD eased out of overbought territory.

GBP was mixed.

The Yen firmed.

While the JPY/USD has fallen for 4 weeks.

And the USD/IDR has risen for 4 weeks.

CHF/JPY fell and snapped its 4-week winning streak.

And the EUR/CHF rose and broke its 5-week losing streak.

The larger advancers over the past week comprised of;

Australian Coking Coal 2.5%, Richards Bay Coal 4.8%, Rotterdam Coal 2.9%, Brent Crude 2.2%, WTI Crude 3.6%, Heating Oil 2.8%, JKM LNG 2.6%, Lumber 3.5%, JKM LNG 4.8%, Newcastle Coal 5.4%, Dutch TTF Gas 5.4%, Gasoil 5.4%, KBW Banks 2.6%, DJ Transports 2.4% and the Philippines PSE rose 2.9%.

The group of largest decliners for the week included;

Bloomberg Commodity Index (1.8), Baltic Dry Index (7.5%), Cocoa (4.1%), Cotton (3.2%), Copper (1.6%), Arabica Coffee (7.2%), Lithium Carbonate (8.8%), Lithium Hydroxide (5.5%), Aluminium (2.5%), Natural Gas (1.9%), Nickel (2.8%), Palladium (8.6%), Platinum (6.8%), Robusta Coffee (4.6%), Tin (4.9%), China Iron Ore (2.4%), Urea U.S. Gulf (3.1%), Silver in AUD (8.2%), Silver in USD 10%), Gold fell b/w 2.8% and 4.6% with USD being the worst, Corn (6.6%), Oats 12.9%, Rice (1.7%), Soybeans (5.5%), Wheat (5%), CSI 300 (1.5%), All World Developed ex USA (1.9%), China A50 (3%), IDX (8.7%), DAX (1.4%), IBB (2.2%), Bovespa (2.7%), Russell 2000 (3%), Nasdaq Composite (4.7%), KSE (2%), KOSPI (3.7%), Mexico (2.6%), NBI (2.5%), Nasdaq 100 (4.5%), Copenhagen (1.6%), SOX (4.7%), IGPA (4.4%), S&P 500 (2.6%), SA40 (3.2%), IPSA (4.8%), TA35 (4.2%), WIG (1.7%), XBI (5.9%), ASX Financials (2.1%), ASX Materials (2.4%) and the ASX Small Caps fell 1.6%.

June 7, 2026

By Rob Zdravevski

rob@karriasset.com.au

June 7, 2026 Leave a comment

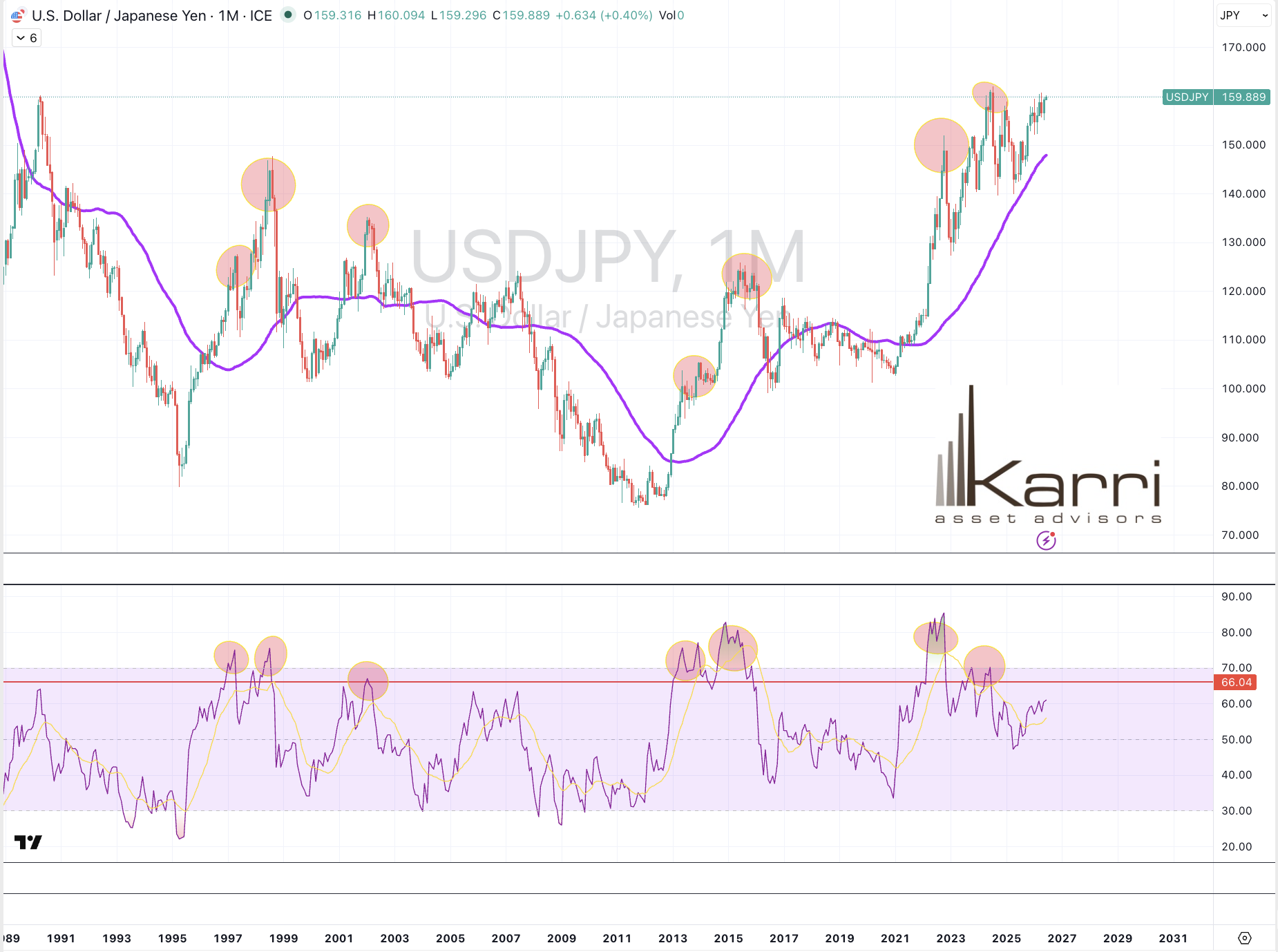

USD/JPY is not at the major extremes seen in other Yen pairs.

My read of the tape suggests that it moves to 167 (vs. current 160), before assessing its next shape.

rob@karriasset.com.au

June 7, 2026