A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

n.b. pricing of (commodity) futures contracts is only considering the immediate front month.

* denotes multiple week inclusion

Extremes above the Mean (at least 2.5 standard deviations)

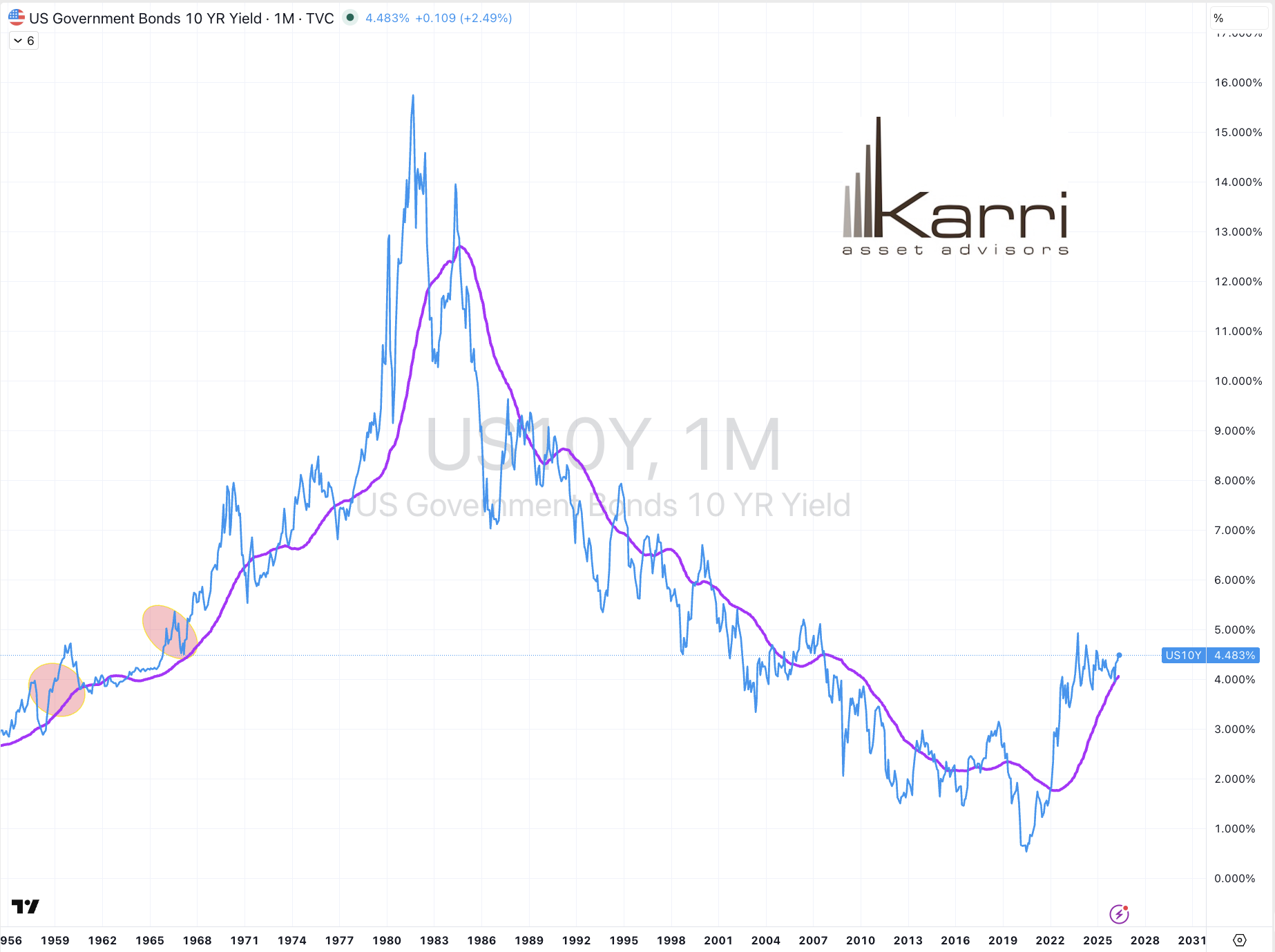

U.S. 5 and 7-year bond yields *

Norwegian, Swiss & U.S. 10-year yields

U.S. 20-year government bond yield

German & U.S. 30-year bond yields *

TBT & TBX *

U.S. 5-year bond yield minus 5-year breakeven inflation rate

U.S. 5 year minus U.S. 3-month yield spread *

U.S. 10 year minus Australian 10-year bond yield spread

U.S. 10 year minus German 10-year bond yield spread

U.S. 10-year bond yield minus 10-year breakeven inflation rate

U.S. 10 year divided by Australian 10-year bond yield spread

Rice *

Overbought (RSI > 70)

Japanese 2 & 5-year government bond yields

Australian Coking Coal *

Richards Bay Coal *

JKM LNG *

Gasoline *

CRB Index *

Urea Middle East *

AUD/EUR *

AUD/IDR *

AUD/INR *

AUD/JPY *

AUD/THB *

CNH/USD *

TAIEX *

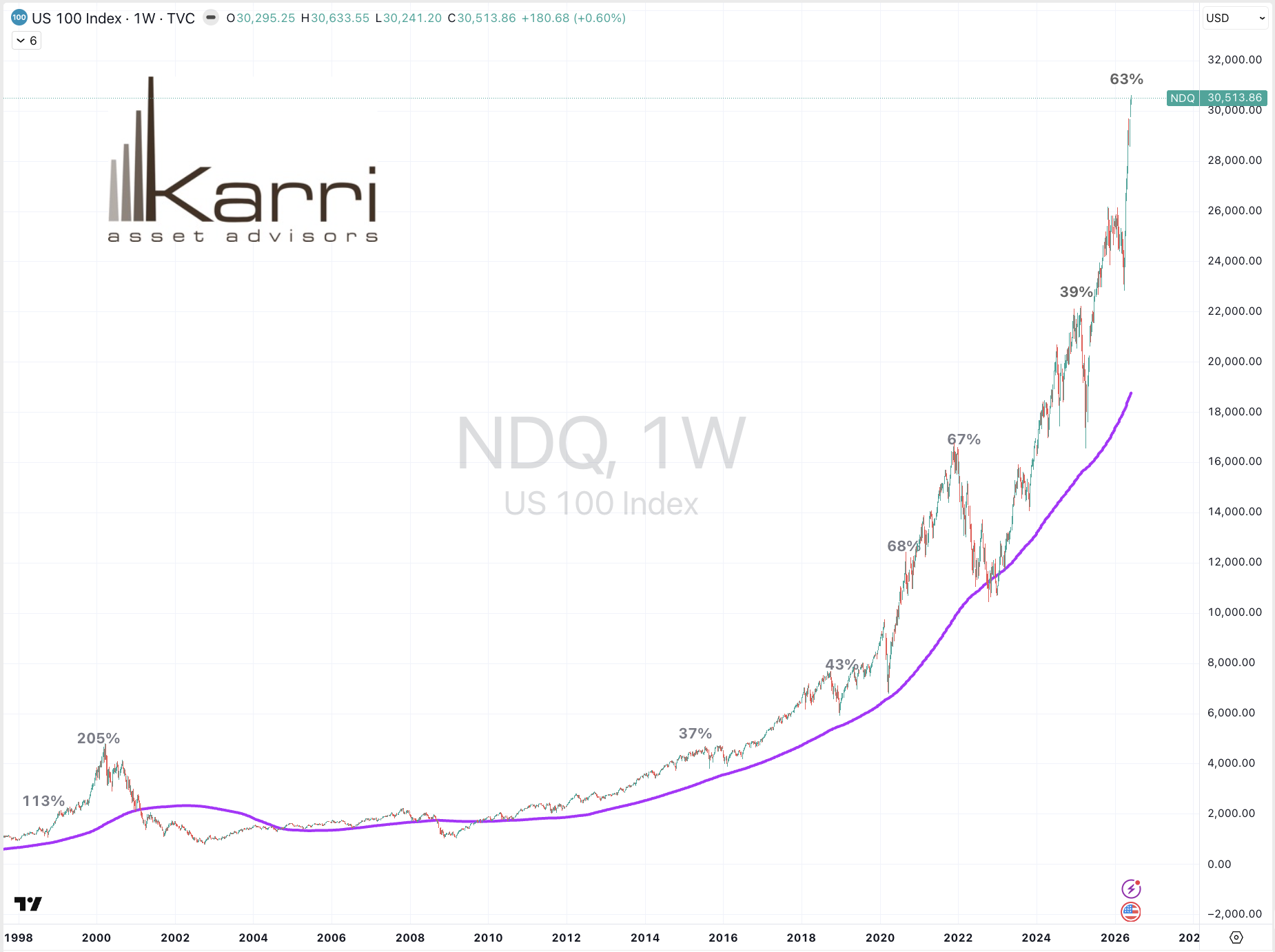

Nasdaq Composite

KOSPI *

Nasdaq 100 *

Nikkei 225

Norway’s OBX

Finland’s OMXH

Singapore’s Strait Times Index

Philadelphia’s SOX Index *

And the S&P 500

The Overbought Quinella (Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Japanese 10 and 30-year government bond yields *

South Korean 10-year bond yield *

USD/IDR

Extremes below the Mean (at least 2.5 standard deviations)

Australian 10-year minus U.S. 10-year bond yield spread

IEF & TLT

U.S. 10 year minus U.S. 5-year government bond yield spread

Lean Hogs

Oversold (RSI < 30)

JPY/AUD *

Indonesia’s IDX Composite Index

The Oversold Quinella (Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

IDR/USD

Notes & Ideas:

Government bond yields fell,

Except for Chilean 10’s, Japanese 2’s & 3’s along with U.S. 2’s and 3’s.

A host of yield spreads appear in this week’s list.

Korean 10-year yields fell and snapped 5 weeks of advance.

Aussie and Canadian 10-year yields put in a bearish outside reversal week.

U.S. 2- and 3-year yields along with U.S. 5-year real interest rates have risen for 5 weeks.

U.S. minus German 10-year yield spread has climbed for 6 weeks.

While U.S. 30 year minus U.S. 10-year yield spread has fallen for 5 weeks.

And the Copper/Gold Ratio have risen for 7 straight weeks.

Equities had a positive bias.

A few more indices left overbought territory.

Thailand’s SET is in 4-week winning streak.

The S&P 500 has climbed for 8 consecutive weeks.

Vietnam fell and snapped a 7-week winning streak.

The CAC, DJ Transports, IGPA and FTSE 100 rose and snapped 4 weeks of decline.

The ASX Financials broke a run of 5 weeks of a lower close.

The ASX small caps have fallen for 5 weeks.

While Brazil’s BOVESPA has declined 11% over the past 6 weeks.

Commodities were mixed and a little quieter, relatively.

Aluminium, Coal, Gases, Coffee and Tin were the notable gainers.

Crude Oil, Distillates, Cocoa, Cotton, Cattle and Palladium were amongst the decliners.

Richards Bay Coal and Rice have risen for 4 weeks, the latter climbing 15% over that time.

Cotton has given up 9% over the past fortnight.

Palladium is 12% lower in 3 weeks.

U.S. Gulf Urea is in a 5-week losing streak.

Australian Coking Coal fell to snap its 5-week winning streak.

And the Baltic Dry Index fell and broke a 7-week losing streak.

Currencies were quiet.

The Aussie and Loonie eased.

Yen was mixed.

The Swissie and Pound Sterling firmed.

NZD/AUD rose and departed oversold territory.

EUR/CHF is in a 4-week losing streak.

Aussie/Rupee fell and broke a 6-week winning streak.

And the Aussie fell to snap 7 weeks of gains against the Euro.

The larger advancers over the past week comprised of;

Aluminium 3.4%, Rotterdam Coal 3.2%, Arabica Coffee 2%, JKM LNG in Yen 2.3%, Orange Juice 4.3%, Robusta Coffee 2.7%, Tin3.6%, Corn 1.7%, Rice 3.3%, Soybeans 1.7%, Wheat 1.7%, All World Developed ex USA 2.1%, AEX 3.4%, ATX 2.1%, KBW Banks 3.4%, CAC 2.1%, DAX 3.9%, DJ Industrials 2.2%, DJ Transports 3.2%, FCATC 1.5%, IBEX 2.1%, S&P SmallCap 600 2.6%, Dublin 4.9%, Russell 2000 2.&%, TAIEX 2.7%, KRE Regional Banks 3.6%, KOSPI 4.7%, FTSE 250 2.5%, S&P MidCap 400 1.7%, Nikkei 225 3.1%, Helsinki 3.5%, Stockholm 3.6%, PSI 1.8%< SMI 2.1%, SOX 5.3%, IGPA 1.4%, STI 1.6%, Eurostoxx 3.3%, Nasdaq Transports 2.4%, TSX 1.9%, FTSE 100 2.7%, WIG 2.9% and the ASX Financials rose 2.1%.

The group of largest decliners for the week included;

Bloomberg Commodity Index (1.6%), Brent Crude Oil (5.2%), Baltic Dry Index (5.1%), Cocoa (5.2%), WTI Crude Oil (4.4%), Cotton (4%), Lean Hogs (2.5%), Heating Oil (3.8%), Cattle (3.4%), Lithium Carbonate (2.5%), Natural Gas (1.8%), Palladium (4.6%), Platinum (2.6%), Gasoline (5.8%), S&P GSCI (2.6%), CRB Index (1.7%), Dutch TTF Gas (3%), Gasoil (5.7%), Urea Middle East (1.8%), Uranium (1.7%), Gold in ZAR (2%), BUX (1.6%), China A50 (1.8%), IDX (8.4%), EGX (2%), HSCEI (1.6%), Hang Seng (1.4%), KLSE (1.6%), Vietnam (2.3%), BIST (3.9%) and the ASX Industrials fell 2.2%.

May 24, 2026

By Rob Zdravevski

rob@karriasset.com.au