The following assets (on a weekly timeframe) registered an Overbought reading or traded more than 2.5 standard deviations above its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

Lumber

China’s CSI 300 equity index

Overbought (RSI > 70)

the JKM “Japan/Korea (LNG) Marker”

Coffee

Cattle

Urea

Dutch TTF Natural Gas

and the U.S. Dollar (DXY) Index

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

U.S. 2 year bond yields

Assets (securities) which touched the other side of the extreme, being Oversold (where the RSI is < 30) or were at least 2.5 standard deviations below its mean are;

Extremes “below” the Mean (at least 2.5 standard deviations)

The difference between the U.S. 10 year bond yield minus the U.S. 2 year bond yield

Oversold (RSI < 30)

EUR/USD

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean.

TRY/USD – the Turkish Lira is historically weak

Notes & Ideas:

The main news over the past week is the impressive (but not surprising) rally in equity indices. The crowd tends to either be short or continue to extend the bubble commentary talk. Its inevitable that markets move to where they can do more damage and going up can damage ‘participants’ as much as it can when it comes down.

In other notes on trends and price action include;

Adding to last week’s 25% decline Henry Hub Natural Gas fell a further 5%.

Gold (in AUD) needs to holds A$2,467 and USD priced Gold equivalent level is US$1,758.

If not, I expect Gold to move lower.

Silver is making new (recent) lows and I’m watching closely if it holds $21.80.

Inversely, watching is Brent Crude trades above $77.00, which be a higher weekly high than last weeks.

Japanese (JGB’s) and American 10 year government bond yields are testing support lines. Holding these supports is constructive for the general sentiment of risk assets, such as 1.34% for the US 10’s. i.e. you don’t want the JGB’s testing the 0.03% mark nor trading below 0.02%.

Although not oversold, (its close), a declining GBP versus USD is now at my initial Buy price of 1.3260. I’ll add to British Pound positions if it goes lower.

Positively, for risk assets, the AUDJPY traded higher intra-week and closed higher than the last, although it is yet to break an important resistance line. Broadly, a “double-dip” in equities is still on, unless various currency resistances are breached.

For the contrarians, the Hang Seng China Enterprises Index (HSCEI) had a bullish outside reversal week,

And I want to finish comparing the correlation between Russia’s MOEX equity index against some interest rates and currencies to help confirm risk on/off momentum.

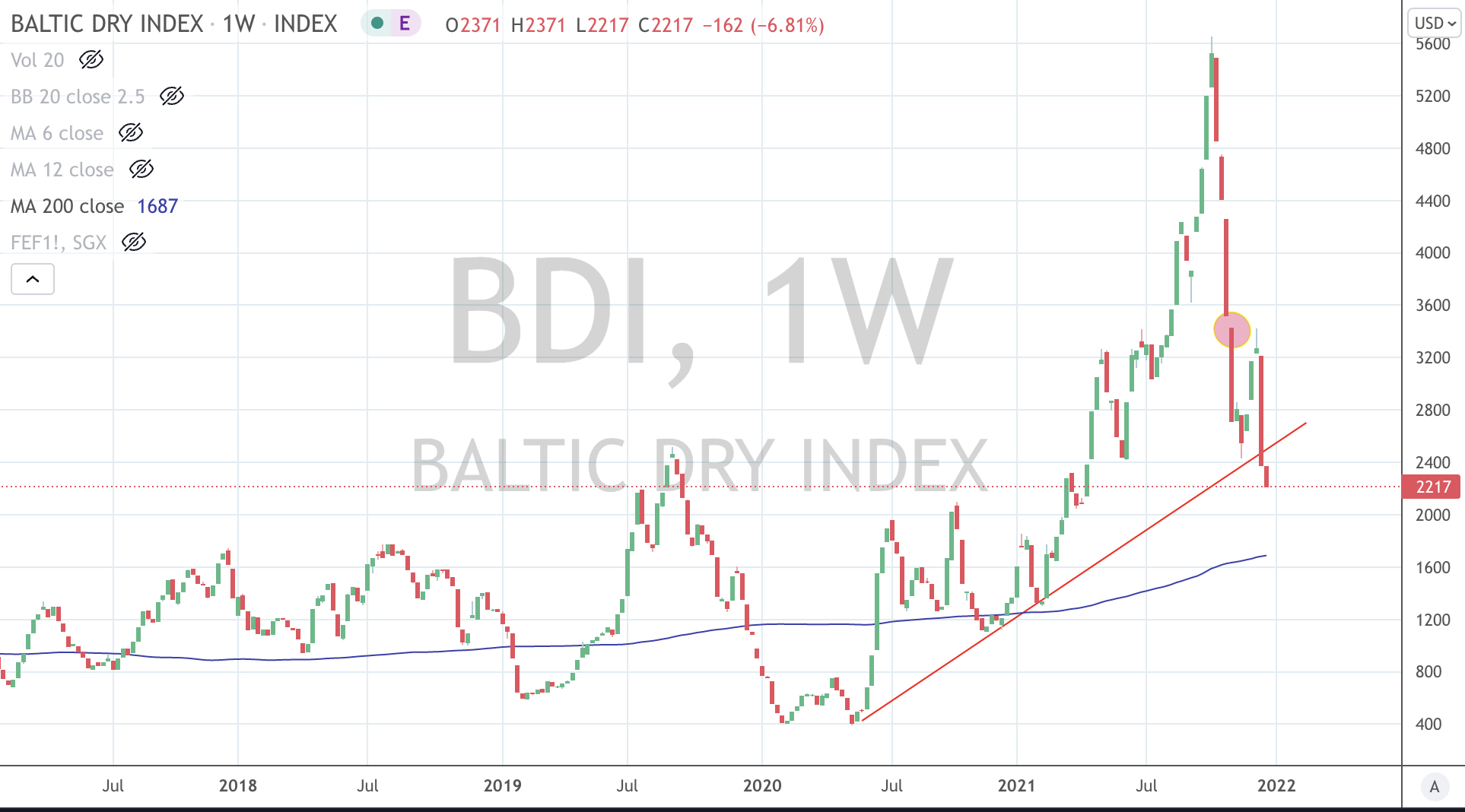

The larger advancers over the past week comprised of the Baltic Dry Index 3.2%, (up 27% in 3 weeks), WTI Crude 8.2%, Gasoil 4.4%, Heating Oil 7.3%, JKM 3%, Lumber 17.3% (adding to last week’s 18.3% rise), Dutch TTF Gas 18.2%, Orange Juice 5%, Gasoline 9.4%, Sugar 5.1%, CRB Index 2.4%, Rotterdam Coal 11%, Australian Coal 9.7%, Shanghai Composite 1.6%, Amsterdam’s AEX 2%, , KBW Banking Index 2.2%, CAC 3.3%, CSI 300 3.1%, DAX 3%, Dow Jones Industrial 4%, Dow Jones Transports 2.7%, Italy’s MIB 3%, BOVESPA 2.6%, S&P 400 Midcap 3%, Nasdaq 100 4%, Sensex 1.8%, Copenhagen 3.9%, Helsinki 2.4%, FTSE 100 2.4%, Stockholm 3.3%, Russell 2000 2.4%, Swiss SMI 3.6%, SOX 2.9%, Nasdaq Transports 2.9%, the S&P 500 3.9%, Australia’s ASX 200 1.6% and Istanbul’s BIST equity index rose 7%, giving it a 46% return in the pasty 8 weeks.

The group of decliners included Aluminium (1.8%), Coffee (4.4%), Natural Gas (5%), Gold in AUD (2.5%), Rice (1.7%), Wheat (2.3%) and Russia’s MOEX equity index (3.9%).

December 12, 2021

by Rob Zdravevski

rob@karriasset.com.au