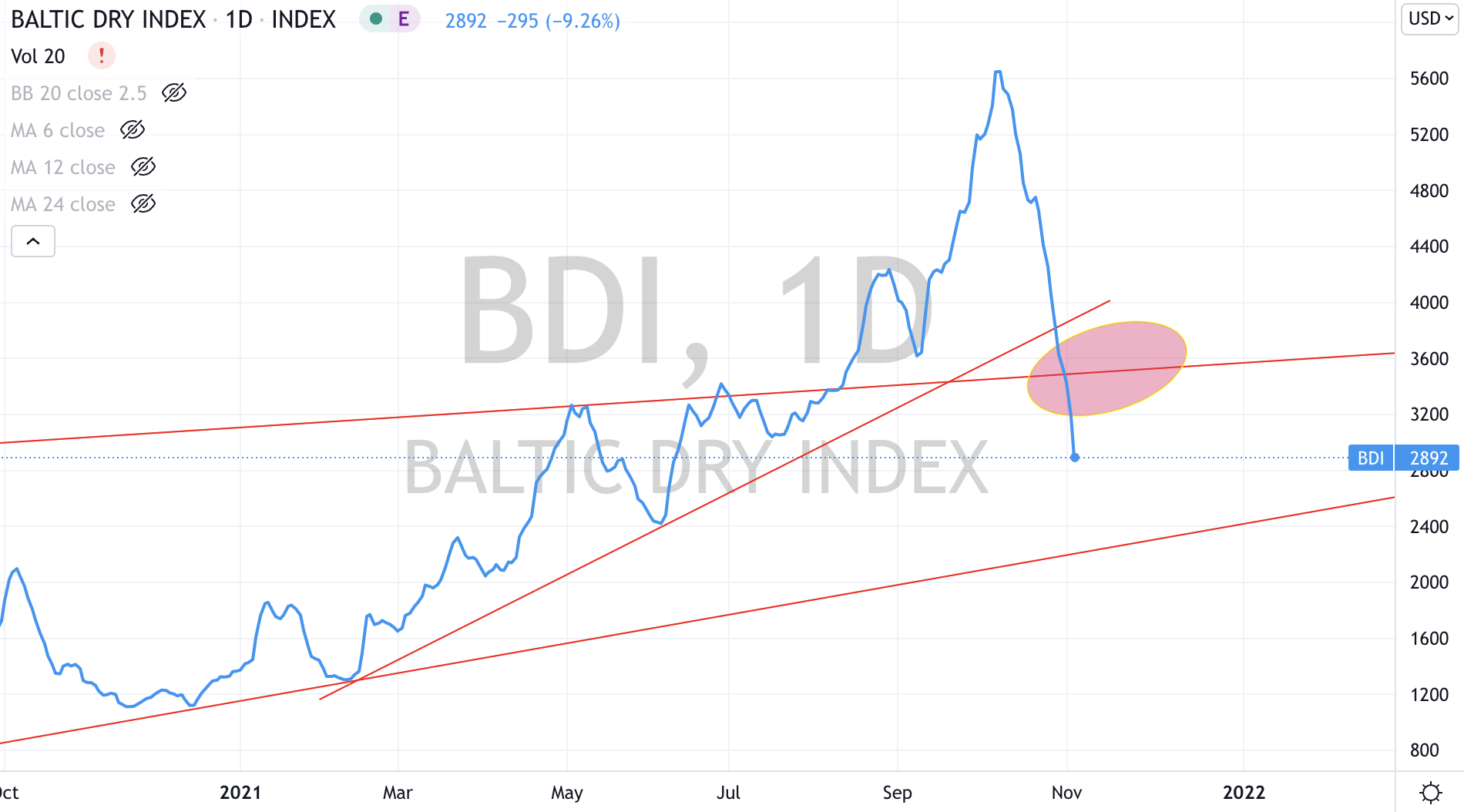

When prices triple, then they halve

November 4, 2021 Leave a comment

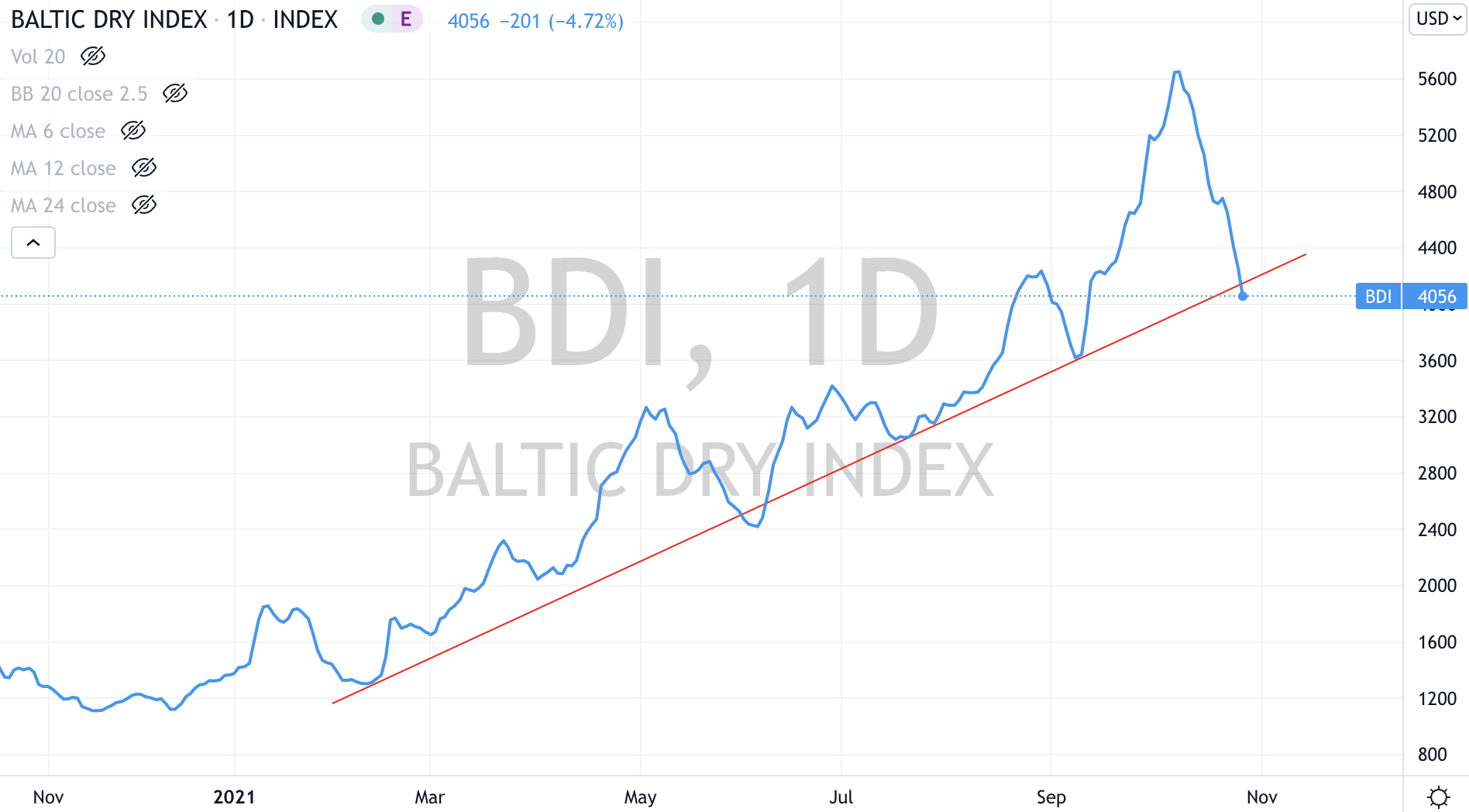

Baltic Dry Index has halved within a month. Blown past my initial target 🎯, on its way to the next.

This is good for Iron Ore shipping costs.

Trying to hear what's not being said

November 4, 2021 Leave a comment

Baltic Dry Index has halved within a month. Blown past my initial target 🎯, on its way to the next.

This is good for Iron Ore shipping costs.

November 1, 2021 Leave a comment

President Biden can try to frame America’s climate position with all the spin that his administration cares to but I found today’s criticism of President’s Putin and Xi ‘non-attendance’ at COP26 a little bit rich.

https://www.politico.eu/article/biden-says-russia-china-didnt-show-up-on-climate-change-commitments/

However, Biden should note that both Russia and China do have climate policies and commitments. In fact, Russia may be acutely feeling the ‘heat’ more than some.

Russia is warming 2.8 times faster than the global average, with the melting of Siberia’s permafrost, which covers 65% of Russian landmass, releasing significant amounts of greenhouse gases.

But the chart below illustrates a legacy topic which I have been harping on about for years.

It seems OK for the United States to have been ‘dirty’ while they industrialised and grew through their expansive 130 year revolution yet it’s now being critical of China’s modernisation of the past 40 years.

Perhaps much (or some) of China’s historical emissions tally may in fact ‘belong’ or should be attributed to the United States?

How much lower would China’s emissions actually be if U.S. corporations and consumers didn’t order, consume and welcome such stunning amounts of efficiently produced and priced Chinese goods?

Side note: Most of those ships floating off the Los Angeles coast waiting to dock are carrying goods made in China (some from Japan), just so Amazon can deliver them to millions of homes.

https://earthobservatory.nasa.gov/images/148956/waiting-to-unload

I think President Xi’s economic equality and prosperity directive has many prongs to it, which may amount to creating a more ‘inward’ economy, less outward bound production and resulting in lower industrial emissions.

I wrote about the ‘lower emissions’ angle in a recent post titled, China’s Climate Change policy In Disguise along with highlighting ‘de-globalisation’ posturing in another post.

November 1, 2021

by Rob Zdravevski

rob@karriasset.com.au

#cop26 #climatepolitics #spin #china

November 1, 2021 Leave a comment

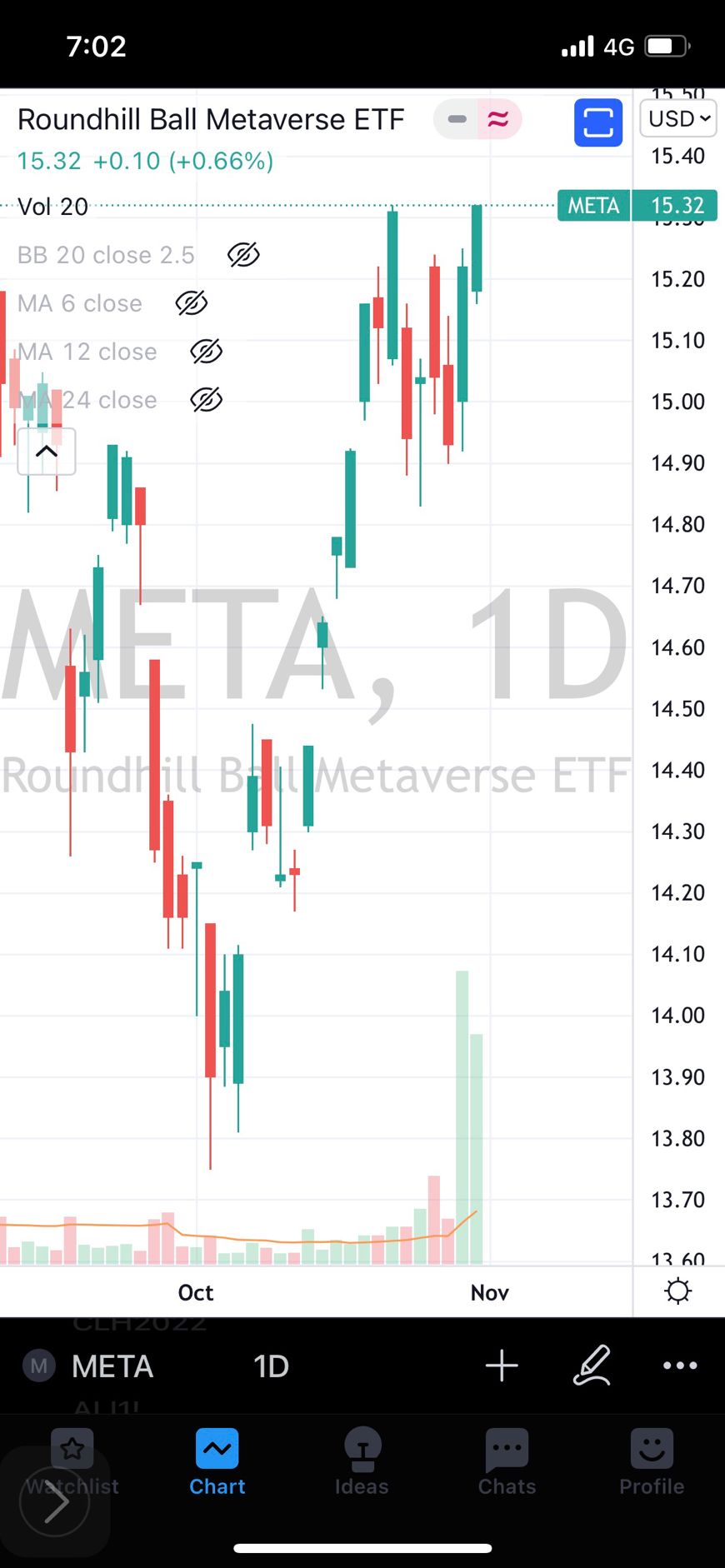

I often carry on about the importance or at least the pre-requisite of doing your homework. The picture below is a good example of financial illiteracy.

It’s a chart of a U.S. listed ETF which has the trading code “META”.

This security usually trades around 170,000 shares.

When Facebook announced that it will change its name to Meta, trading in this stock jumped to an average of 2 million shares in each of the past 2 days. (see the lower bar chart)

Step 1: check that the name of the company or product matches the code and that the price is trading somewhat near where you last remember it to be.

Facebook last traded around $323 per share and has a market cap of $900 billion.

November 1, 2021 Leave a comment

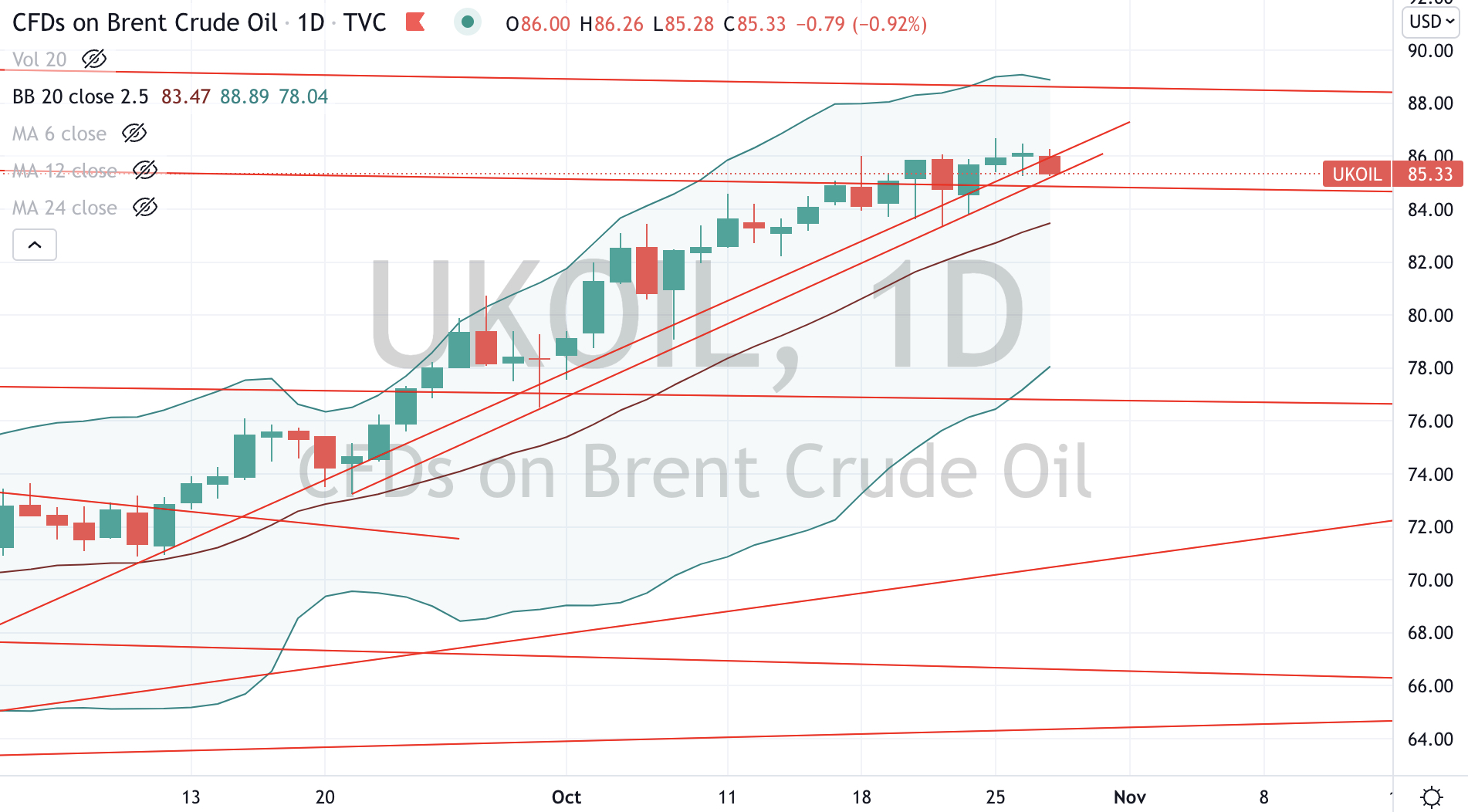

For the past week, the price of West Texas Intermediate (WTI) Crude Oil fell 0.57%.

This ended a 9 week streak of higher weekly closing prices.

The unbroken advance saw the price of WTI Crude rise 48% from its August 2021 low.

What’s so relevant about a 9 week continuous streak in the price of Oil?

Well, it doesn’t happen that often.

So much so, there has never been a 10 week streak within the 32 years of price data that I searched through.

The time surrounding August 2002 was the only other moment when we saw a 9 week streak.

That trend produced a 14% return.

8 week streaks have occurred four times.

The ~ December 1988 streak had a 37% return, the April 1999 streak saw a 35% advance, the February 2003 run climbed 25%, while the July 2004 trend rose 22%.

This recent streaks advance (of 48%) was indeed telling us that it was closer to concluding rather than starting.

The next 2-3 weeks will tell us if its a pause or a reversal.

Keep in mind, that observing and counting streaks is simply fun for statistical nerds and they don’t necessarily take into account the strength of a trend or its velocity.

Over there 32 year observation, we also saw 7 week streaks occur on 8 occasions.

Those 7 streaks had an average performance of 18%. The highest being 33% and the lowest was a paltry 8% advance over the whole 7 week streak.

It’s wise to remember that streaks do come to an end but assessing such a ‘finale’ and whether the trend reverses or merely takes a pause involves analysing a host of different indicators.

November 1, 2021

by Rob Zdravevski

rob@karriasset.com.au

#oil

October 31, 2021 Leave a comment

The following assets (on a weekly timeframe) registered an Overbought reading or traded more than 2.5 standard deviations above its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

Cattle

Gasoline

USD/CNH (suggesting a weak Chinese Yuan)

USD/TRY (meaning a weak Turkish Lira)

Oslo’s equity index

the Nasdaq Transports index

And Instanbul’s BIST equity index

Overbought (RSI > 70)

Canadian and French 10 year government bond yields

WTI Crude Oil

Gasoil

the JKM “Japan/Korea (LNG) Marker”

the CRB commodity indices

Australian coal

Amsterdam’s AEX equity index

Dow Jones Transports index

And the USD/JPY (which means a weak Yen and at it’s the weakest since early 2019, so sell USD and Buy JPY and use it to buy cheap Japanese equities).

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Australian 2, 5 & 10 year government bond yields

U.S. 2 year and 5 year govn’t bond yields

German 2 & 5 year bond yields

Greece 10’s (with a yield of 1.33%)

Italian, Korean and New Zealand 10’s

Urea

Assets (securities) which touched the other side of the extreme, being Oversold (where the RSI is < 30) or were at least 2.5 standard deviations below its mean are;

Extremes “below” the Mean (at least 2.5 standard deviations)

USD/CNH – for context, inverse to an overbought reading, suggesting a strong Chinese Yuan

EUR/AUD – telling us the Euro is weaker and we have a strong Australian Dollar, so sell your AUD and Buy EUR (there are some bargains amongst European equities)

And EUR/GBP

Oversold (RSI < 30)

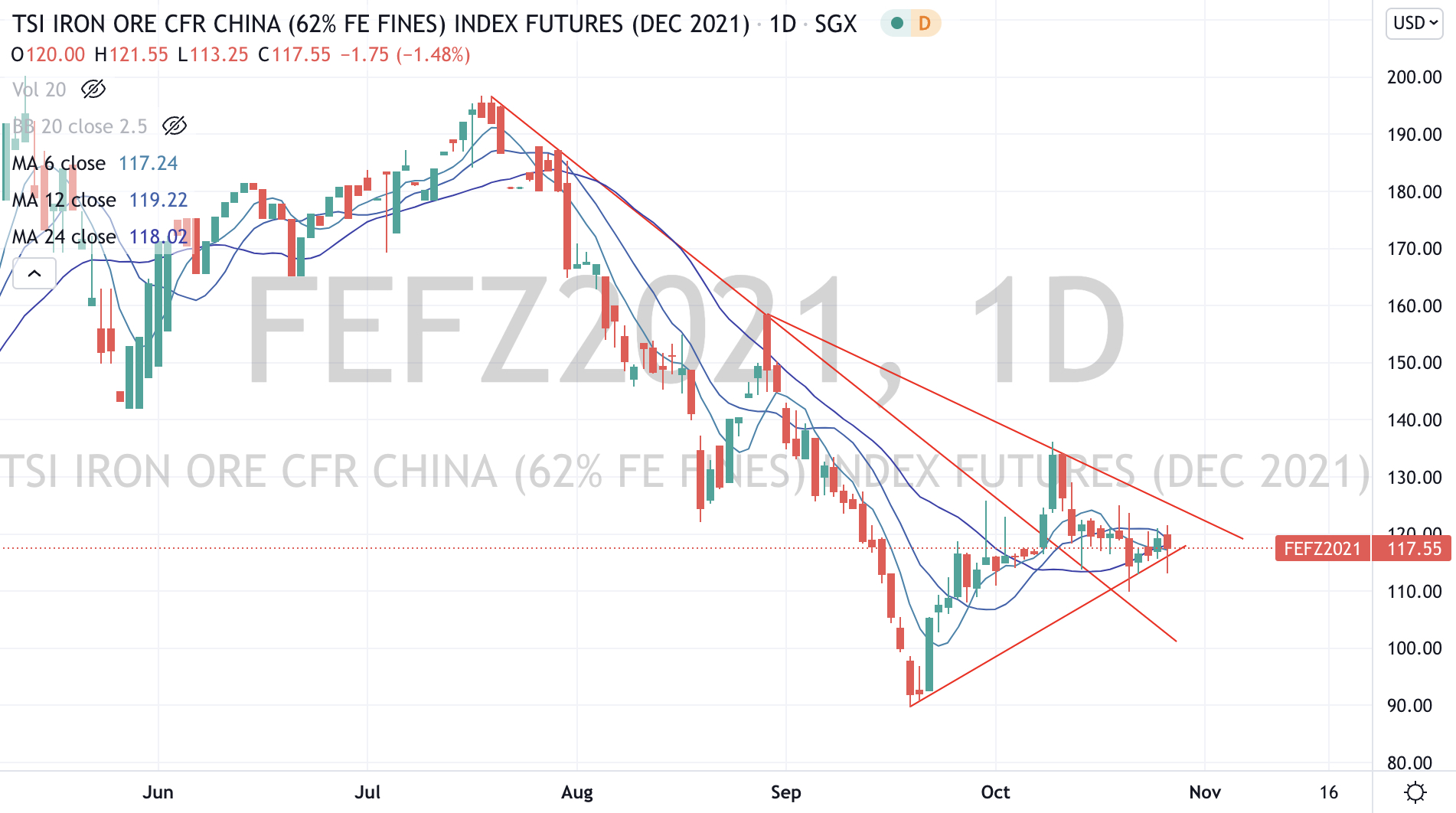

Iron Ore

Brazil’s Bovespa equity index

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean.

None

Notes & Ideas:

The massive news this past week was bond yields rising dramatically. This means bonds were being sold and then its up to interpretation whether funds raised were being used elsewhere (seeking higher risk, perhaps equities) or whether the bond market is pricing in inflation and the pending higher cost of credit.

Take the moves in Australian government bond yields as an example; the 2 year bond yield moved rom 0.13% to 0.67%, while the 5’s went from 1.19% to 1.44% and the Aussie 10’s rose from 1.77% to 1.95% (seeing a high of 2.13%).

The latter is an interesting contrast to Greek 10 year bonds yielding 1.33%.

In other happenings, Hot Rolled Coiled Steel (HRC) broke its 56 consecutive weekly Overbought streak, as it declined 5.3% for the week.

The Baltic Dry Index (the cost of shipping) fell 20%, adding to weeks of recent declines. The price is nearing a price target mentioned in a recent blog post.

Many energy commodities continue to decline (since their recent euphoric media emphasised peaks) with some exhibiting the mean reversion essence of this weekly post.

Some declines in gas and coal have been rapid. European (Rotterdam delivery) Coal fell 38% and Dutch (European) Gas prices slumped 26% in the week.

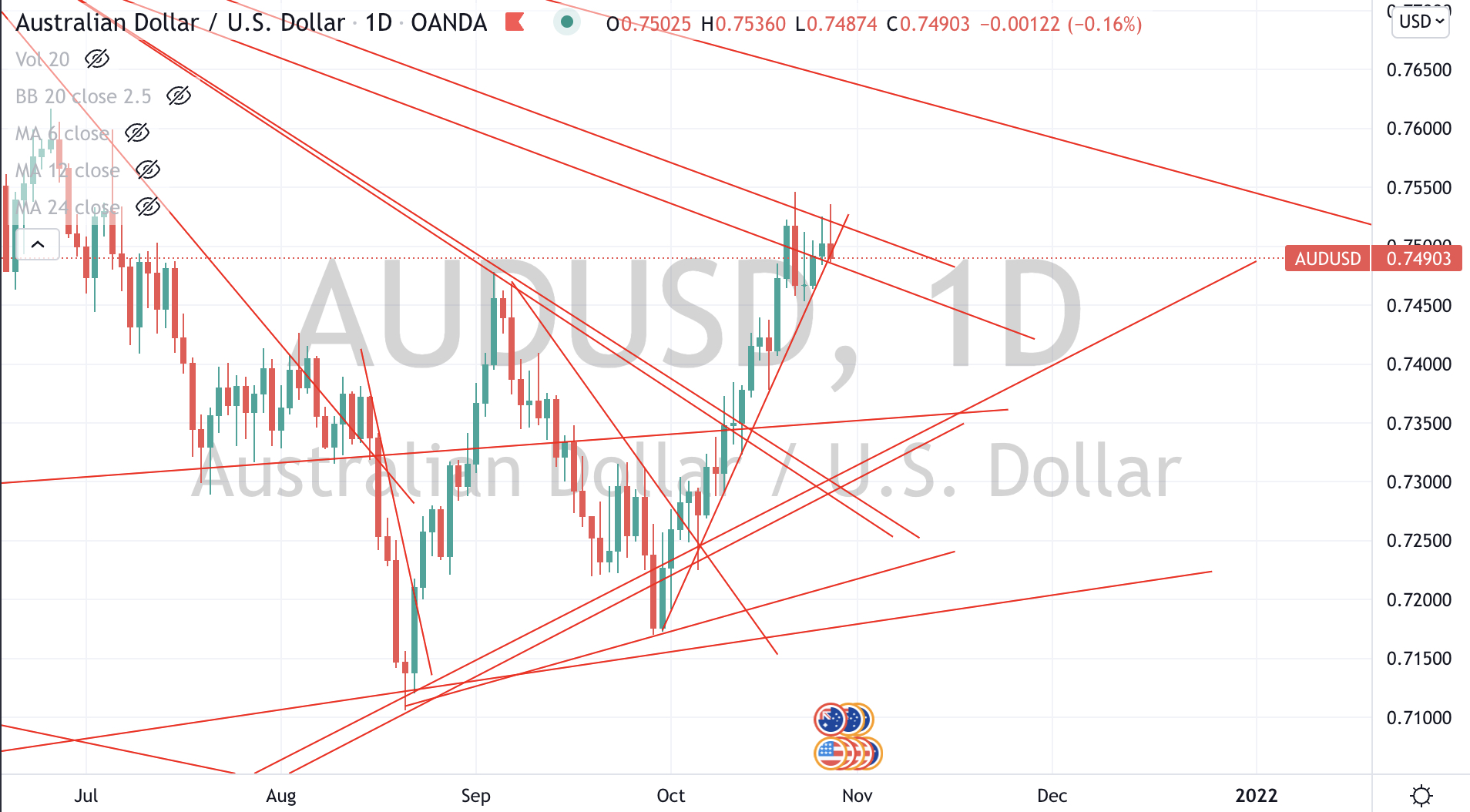

Watching the AUD/USD poke up against 0.7520 is also mesmerising. A break above this means 0.7645 is the next stop.

Other things to watch include the Spanish 10’s are nearing Overbought extremes, the Japanese 10’s are trending higher (currently at 0.11%) and suggesting “risk-on”, the US10 minus US2 year yields are suggesting an equities rally and Corn looks like entering a new medium term bullish trend.

The larger advancers over the past week comprised of Coffee 2.1%, Cattle 4.2%, Natural Gas 2.8%, Corn 5.6%, Wheat 2.2%, Urea 14%, the Nasdaq 3.2%, the Philly SOX 2.4%, the nasdaq Transports 2.6% and Istanbul’s BIST 2.9%.

The group of decliners included Aluminium (5.1%) adding to last week’s 8.3% rout, Baltic Dry Index (20%), Iron Ore (12.6%), Gasoil (2%), Copper (2.9%) further to last week’s 5% fall), HRC (5.3%) LKM LNG (9.8%), Lumber (15.1%), Orange Juice (3%), Australian Coal (4.7%), Dutch TTF Gas (25.7%), Platinum (3%), Gasoline (4.5%), Silver (2.1%), Brent Crude (2.4%), China Coal (11.4%), Rotterdam Coal (38%), Uranium (5.5%), KBW Banking index (2.8%), HSCEI (4.2%), Hang Seng index (2.9%), the Bovespa (2.6%) – its lowest since November ’20, Stockholm (2.5%), the Sensex (2.5%), Oslo (2.1%) and Helsinki (2.2%).

October 31, 2021

by Rob Zdravevski

rob@karriasset.com.au

October 30, 2021 Leave a comment

I found this article very interesting that I re-read it many times.

An extract from the article includes, “Coal emissions must fall by four-fifths in one pathway to 1.5C”

What I don’t seem to find in calls for burning less coal, is that coal fired power remains (generally) cheap and also simple to operate.

This translates to it being cheaper.

We can also argue that western based resources companies shouldn’t mine and sell coal and we should limit our general consumption BUT it remains a fact, that the lowest cost producer prevails in many cases.

Using coal is overwhelmingly an economic topic.

October 28, 2021 Leave a comment

My inadvertent political comment is pointed towards the recent ‘sudden’ and ‘rushed’ coincidence of Australia’s Prime Minister electing to visit the Glasgow COP26 climate event aligning with the subsequent release of a (albeit feeble) net zero climate policy in order to support his reason to ‘show face’ at the event.

Imagine being a political eunuch showing up to a pro-climate change conference without a pro-climate change position.

The poor soul faces an almighty dilemma.

The consequence of his absence at COP26 (as the leader of a nation which is the 2nd largest per capita carbon emitter) would be palpable.

Although having a firm view on global warming (notice how we don’t call it that anymore) and setting an appropriate policy carries a risk, for it has been the re-election downfall of the past 4 Australian Prime Ministers.

But all is averted……

Furthermore, in the coming week, fully vaccinated Australians can now depart Australia much more freely and return from international travel without the need to quarantine.

What a wonderfully coordinated convenience for the travelling ministerial delegation to Glasgow.

There is nothing illegal here, but it’s just a prompt to be aware of how things are framed and presented.

Happy travels!

October 28, 2021 Leave a comment

One month ago, do you remember hearing that European Gas prices were soaring higher?

It was all across the financial media.

Since then, that price was fallen 40%.

It’s funny how you don’t hear this news in the media.

Conserve your energy and mental bandwidth.

Just be careful being sucked into the noise vortex and the financial media’s chosen narrative which only lasts a day or two.

During all of that, some dill paid a high of EUR 130 per megawatt hour.

October 28, 2021

by Rob Zdravevski

rob@karriasset.com.au

October 27, 2021 Leave a comment

Readers of my weekly editions of “Macro Extremes” will remember my commentary about unloved Chinese equities when they were wallowing in oversold territory.

Then we had a plethora of “American” analysts and portfolio managers telling us that China 🇨🇳 is ‘uninvestible’.

On Bloomberg Radio today, a pundit expressed disappointment in the Chinese governments lack of interest (unlike American authorities) to intervene in the affairs of indebted property developers who may risk destabilising the economy.

Let me get this straight….the capitalist is advocating socialism?

p.s. over the past 3 weeks, the Hang Seng China Enterprises Index (HSCEI) has risen 10% while Alibaba has climbed 28%.

October 27, 2021

by Rob Zdravevski

rob@karriasset.com.au

October 27, 2021 Leave a comment

Referencing my previous post, here are price charts of the Baltic Dry Index, Iron Ore, Brent Crude and the AUDUSD.

October 27, 2021

by Rob Zdravevski

rob@karriasset.com.au