Equity bull is OK

September 17, 2025 Leave a comment

Here is a weekly price chart of the AUD/JPY……the broader equity rally is in intact.

September 16, 2025

rob@karriasset.com.au

Trying to hear what's not being said

September 17, 2025 Leave a comment

Here is a weekly price chart of the AUD/JPY……the broader equity rally is in intact.

September 16, 2025

rob@karriasset.com.au

September 16, 2025 Leave a comment

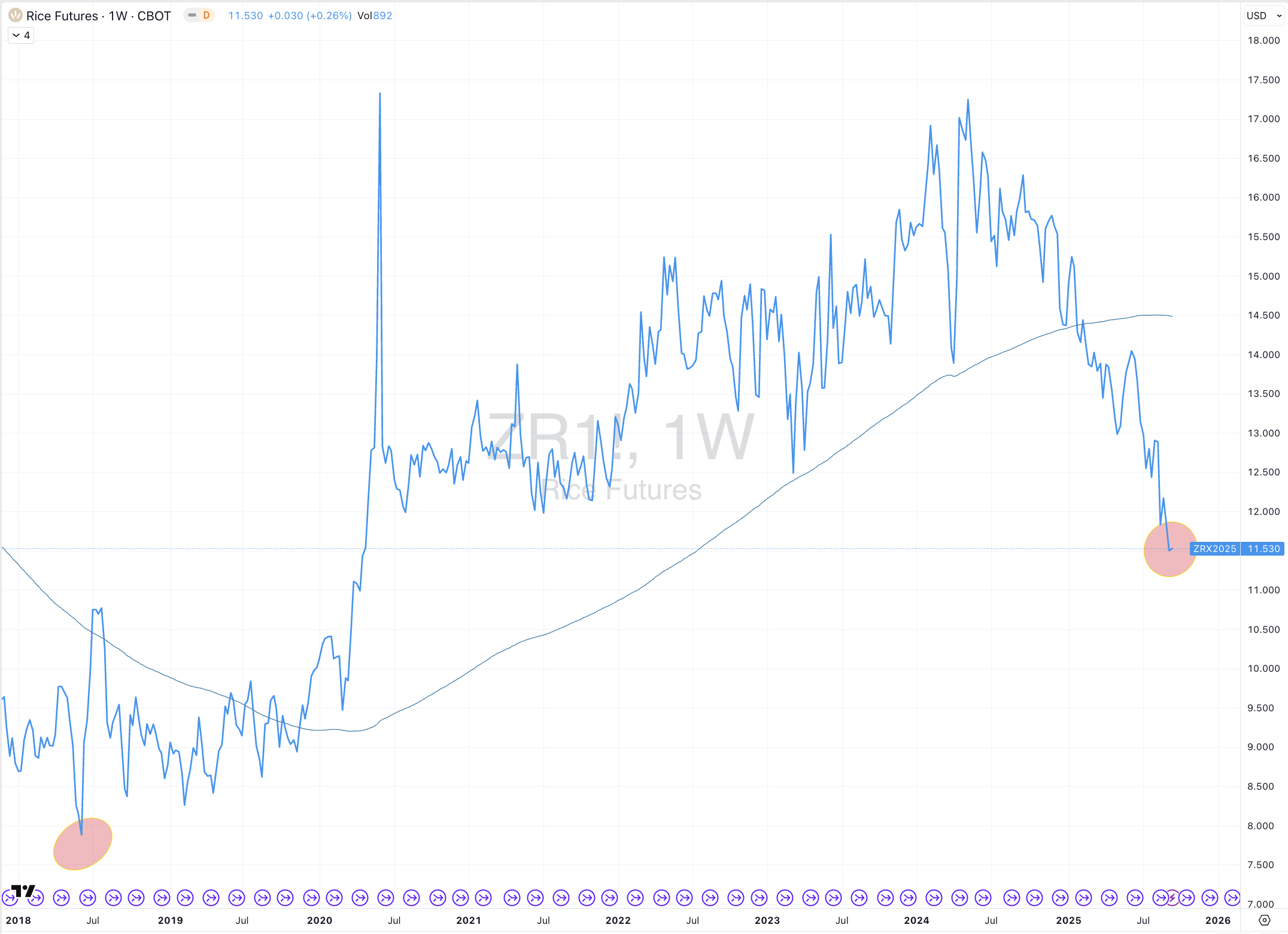

It was 2018 when the price of Rice (as traded on CBOT) saw such empirical oversold extremes.

Think cheaper inputs for baby food, cereals, rice flour and sake….

September 15, 2025

rob@karriasset.com.au

September 14, 2025 Leave a comment

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

n.b. pricing of (commodity) futures contracts is only considering the immediate front month.

* denotes multiple week inclusion

Extremes above the Mean (at least 2.5 standard deviations)

Chinese & Dutch 10 year government bond yields *

IEF & TLT *

Australian 10 year minus U.S. 10 year bond yield spread *

Gold in AUD, CHF, EUR, GBP and ZAR

AUD/IDR *

AUD/CAD *

AUD/SGD

AUD/USD

And Brazil’s BOVESPA equity index *

Overbought (RSI > 70)

Urea (Middle East) prices *

Silver in USD *

Shanghai Composite Index *

CSI 300 *

China A50

China’s FCATC

Taiwan’s TAIEX

Nasdaq Composite

Pakistan’s KSE Index *

South Korea’s KOSPI *

Japan’s Nikkei 225

Czechia’s PX Index *

South Africa’s SA40 *

Chile’s IGPA and IPSA indices *

Singapore’s Strait Times

Israel’s TA 35 Index *

Canada’s TSX *

Vietnam’s VN Index *

And the ASX Small Cap Index *

The Overbought Quinella (Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Gold in USD and CAD *

AUD/INR

IPC Mexico equity index *

Extremes below the Mean (at least 2.5 standard deviations)

New Zealand 10 year government bond yield

Australian 10 year bond yield minus its 5 year bond yield

TBT

U.S. 3, 5, 7, 10, 20 and 30 year bond yields

U.S. 10 year bond yield minus 10 year breakeven inflation rate

Newcastle Coal

AUD/THB

CAD/AUD

USD/SEK

And Philippines’ PSI equity index

Oversold (RSI < 30)

Rice

The Oversold Quinella (Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

U.S. 3 month bill yield *

Richards Bay Coal

Lumber *

Notes & Ideas:

Government bond yields rose, except for U.S. and UK 30’s, which rose.

Last week’s overbought sovereign 10’s are no longer.

U.S. corporate bond yields (and the high yield effective yield) are a whisker from oversold levels and at are at their most oversold since December 2020.

The U.S. 5 year breakeven rate bounced out of oversold territory.

Canadian 10 year yields have fallen for 4 weeks.

U.S. 7 year bond yields mean converged.

U.S. 2 and 30 year yields rose and broke for their 4 weeks falling streak.

And the U.S 10 year minus inflation rate spread is at its most oversold level since March 2022.

Equities were firmer, again.

The overbought list grew this week with notable new entrants including the Nasdaq Composite and the Nikkei 225.

Chinese indices are crowding the overbought list too.

Amidst all the concerns surrounding tariffs, Mexico has registered an overbought quinella.

The Dow Jones Transports have fallen for 3 weeks while the Philippines PSE has slumped for 5 weeks.

The Strait Times is in a 4 week wining streak.

Bovespa fell and broke a 5 week winning streak.

The Russell 2000, TSX and ASX Small Caps have put together a 6 week winning streak.

And the S&P 500 has risen for 9 of the past 12 weeks.

Commodities were generally stronger.

Crude Oil, Aluminium, Coffee, Orange Juice, Shipping Rates and Corn were amongst the notable gainers.

Coal, Rice, Natural Gas, Cattle and Lithium Carbonate dominated the losers category.

Sugar rose from being oversold with Rice taking its place.

The Copper/Gold ratio is nearing oversold levels.

Corn, Lean Hogs, Silver in AUD & USD along with Gold in AUD, CAD, CHF, and EUR are all in a 4 week rising streak.

Platinum has risen for 6 weeks.

Cocoa has declined for 4 weeks.

Richards Bay Coal, Lumber and U.S. Gulf urea prices are in 6 week losing streaks.

Currencies were active, again.

The Aussie rose notably.

While the Yen, Loonie and the Euro fell.

The Swissie has risen against the Yen for 4 weeks.

The CHF/USD has climbed for 5 weeks.

USD/SEK has declined for 6 weeks.

And the NZD/AUD is a 7 week losing streak.

The larger advancers over the past week comprised of;

Aluminium 3.6%, Brent Crude 2.3%, Baltic Dry Index 7.4%, WTI Crude 1.3%, Copper 2.2%, Arabica 6.2%, Orange Juice 6.2%, Palladium 10.8%, Platinum 1.8%, Robusta Coffee 6.8%, Sugar 1.5%, Tin 1.9%, Dutch TTF Gas 2.2%, Gasoil 1.8%, Silver in USD 2.9%, Gold in CAD 1.7%, Gold in USD 1.6%, Corn 2.9%, Soybeans 1.9%, Shanghai Composite 1.5%, KBW Banks 2%, CAC 2%, China A50 2.1%, FCATC 6.4%, MIB 2.3%, HSCEI 3.4%, Hang Seng 3.8%, IBEX 3.1%, TAEIX 4%, Nasdaq Composite 2%, KLSE 1.4%, KOSPI 5.9%, Mexico 2.2%, Nasdaq 100 1.9%, Nikkei 225 4.1%, Nifty 1.5%, Oslo 1.8%, Helsinki 1.5%, South Africa 3.1%, Sensex 1.5%, SET 2.3%, SOX 4.2%, TA35 1.5% and the S&P 500 rose 1.6%.

The group of largest decliners from the week included;

Richards Bay Coal (2.4%), Rotterdam Coal (2.4%), EHR (2%), Cattle (2.5%), Lithium Carbonate (2.2%), Newcastle Coal (7.5%), Natural Gas (3.5%), Rice (3.3%), BUX (1.9%), IBB (1.5%), NBI (1.6%), SMI (1.4%), IGPA (2.1%), IPSA (2.4%), BIST (3.3%) and the ASX Industrials index fell 1.3%.

September 13, 2025

By Rob Zdravevski

September 12, 2025 Leave a comment

Amidst the hootin’ and a hollerin’ about the Gold price…..

here is the Gold price in Canadian Dollars…..

and when it trades at its upper 3 standard deviation point, it goes sideways to lower for a period of time afterwards.

September 11, 2025

rob@karriasset.com.au

September 9, 2025 Leave a comment

Reprising my view from a month ago, warning about the resumption of lower stock prices in listed Lithium companies…..

Back then lithium stocks were advancing on the news that CATL was seeing supply disruptions.

Today, there is news that Chinese battery giant Contemporary Amperex Technology (CATL) is expected to soon resume production at its lithium mine in Yichun.

September 9, 2025

September 7, 2025 Leave a comment

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

n.b. pricing of (commodity) futures contracts is only considering the immediate front month.

* denotes multiple week inclusion

Extremes above the Mean (at least 2.5 standard deviations)

Chinese, French, British, Greek Norwegian & Swedish 10 year government bond yields *

30 year British bond yield

IEF & IEI

Australian 10 year minus U.S. 10 year bond yield spread

Italian 2 and 10 year bond yields

U.S. 10 year minus U.S. 2 year bond yield spread

U.S. 10 year minus U.S. 5 year bond yield spread *

Gold in AUD, GBP and ZAR

AUD/IDR

AUD/CAD

BOVESPA

IPC Mexico equity index

Overbought (RSI > 70)

Cattle *

Urea (Middle East) prices *

Silver in AUD & USD

Gold in CHF & EUR

Shanghai Composite Index *

Pakistan’s KSE Index *

South Korea’s KOSPI *

Czechia’s PX Index

South Africa’s SA40 *

Israel’s TA 35 Index

Canada’s TSX *

Vietnam’s VN Index *

And the ASX Small Cap Index *

The Overbought Quinella (Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

U.S. 10 year minus U.S. 5 year bond yield spread

Gold in US and CAD

CSI 300 *

Chile’s IGPA and IPSA indices *

Extremes below the Mean (at least 2.5 standard deviations)

Belgian 10 year government bond yield

U.S. 2, 3, 5, 7 and 10 year bond yields

U.S. 5 year bond yield minus 5 year breakeven inflation rate

U.S. 10 year bond yield minus Australian 10 year bond yield

U.S. 10 year bond yield minus 10 year breakeven inflation rate

U.S. 10 year bond yield divided by Australian 10 year bond yield

Australian Coking Coal

Philippines PSI equity index

Oversold (RSI < 30)

Sugar

The Oversold Quinella (Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

U.S. 3 month bill yield *

Lumber *

Notes & Ideas:

Government bond yields fell.

Some overbought entrants this week appeared as so due to intra week highs.

U.S. corporate bond yields are nearing oversold levels.

U.S. 7 year bond yields are close to some mean reversion.

Indonesian 10 year yields rose and broke a 4 week falling streak.

U.S. 2 and 3 year yields have fallen for 4 weeks.

U.S. 3 month bill are oversold and in a 6 week losing streak.

Indian 10 year yields fell and halted their 8 week climb,

And June 2019 was the last time the U.S. 5 year real interest rate simultaneously mean reverted and registered an oversold extreme.

Equities rose mixed with a slight bias towards weakness.

This has resulted in half of last week’s overbought entrants no longer being so, this week.

A couple Chinese indices left overbought extreme territory.

Shanghai, CSI 300, KBW Banks index, ASX 200 and FCATC fell and ended their 4 week winning streak.

The following indices are in 5 week winning streaks; Bovespa, Russell 2000, TSX and the ASX Small Caps.

While the HSCEI and Hang Seng rose.

Commodities were mixed, again.

Gases, Precious Metals and Rubber were amongst the notable gainers.

Crude Oil, Coffee, Coal, Lithium, Orange Juice, Sugar, Oats and Wheat dominated the losers category.

The Copper/Gold ratio is nearing oversold levels.

Richards Bay Coal, Lumber and U.S. Gulf urea prices are in 5 week losing streaks.

Arabica Coffee, Tin and Uranium broke their 4 week winning.

Platinum has risen for 5 weeks.

Middle East Urea prices have risen for 10 weeks.

Cattle broke its 10 straight weeks of gains.

Currencies were active.

The Aussie, Euro and Swissie rose.

The CHF/USD has risen for 4 weeks.

The Loonie fell.

The British Pound and Yen were slightly softer, again.

The U.S. Dollar was slightly weaker.

USD/SEK has declined for 5 weeks.

And the NZD/AUD is a 6 week losing streak.

The larger advancers over the past week comprised of;

Palm Oil 1.6%, LNG in Yen 3.9%, Natural Gas 1.7%, Silver in AUD 3%, Silver in USD 3.3%, Gold in AUD 3.8%, Gold in USD 4%, Rubber 2.9%, Gold in CHF 3.7%, Gold in EUR 3.7%, Gold in GBP 4%, Gold in CAD 4.7%, Gold in ZAR 3.7%, IBB 3.6%, KSE 3.8%, Mexico 3%, NBI 3.6%, SET 2.3%, SMI 1.5%, SOX 1.6%, IGPA 3.3%, IPSA 3.5%, XBI 6.3% and Canada’s TSX rose 1.7%.

The group of largest decliners from the week included;

Richards Bay Coal (1.8%), Brent Crude (2.9%), BDI (2.3%), Cocoa (3.1%), WTI Crude (3.3%), Arabica Coffee (3.2%), Lumber (1.5%), Lithium Carbonate (4.6%), Newcastle Coal (1.4%), Nickel (1.4%), Orange Juice (5.2%), Robusta Coffee (10.5%), Sugar (5%), Tin (2.3%), CRB Index (1.5%), Urea U.S. Gulf (1.9%), Oats (3.7%), Rice (2.3%), Soybean (2.6%), Wheat (2.8%), KBW Bank Index (1.6%), DAX (1.3%), Egypt (2.7%), FCATC (2.7%), BIST (5%) and Italy’s MIB fell 1.4%.

September 7, 2025

By Rob Zdravevski

August 31, 2025 Leave a comment

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

n.b. pricing of (commodity) futures contracts is only considering the immediate front month.

* denotes multiple week inclusion

Extremes above the Mean (at least 2.5 standard deviations)

Austrian, Chinese, French, British and Indian 10 year government bond yields *

IEF

U.S. 10 year minus U.S. 2 year bond yield spread

AUD/INR

RMB/USD

KLSE

Overbought (RSI > 70)

Cattle *

Urea (Middle East) prices *

Shanghai Composite Index *

Egypt’s EGX 30 equity index *

Pakistan’s KSE Index *

South Korea’s KOSPI *

South Africa’s SA40 *

Chile’s IGPA and IPSA indices

Canada’s TSX *

Vietnam’s VN Index *

The ASX 200 *

ASX Industrials *

And the ASX Small Cap Index *

The Overbought Quinella (Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

U.S. 10 year minus U.S. 5 year bond yield spread

U.S. 30 year minus U.S. 10 year bond yield spread

CSI 300 *

China’s A50 equity index *

FCATC Index *

Extremes below the Mean (at least 2.5 standard deviations)

Belgian and New Zealand 10 year government bond yield

NZD/AUD

NZD/USD *

Oversold (RSI < 30)

Indonesian 10 year government bond yield

The Oversold Quinella (Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

U.S. 3 month bill yield *

Lumber *

Notes & Ideas:

Government bond yields mostly eased…..

with the exception of Sweden, Russia and Portugal.

Indonesian 10 year yields are in a 4 week falling streak.

U.S. 3 month bill are oversold and in a 5 week losing streak.

And Indian 10’s have climbed for 8 weeks.

Equities rose mixed with a slight bias towards weakness.

This has resulted in half of last week’s overbought entrants no longer being so, this week.

Chinese indices persist with their overbought extreme quinella’s.

The following indices are in 4 week winning streaks; CSI 300, KBW Banks, China A50, FCATC, Bovespa, Russell 2000, KRE Regional Banks, IGPA, IPSA, TSX, Vietnam, ASX 200 and ASX Small Caps.

The ASX Financials fee and broke their 4 week rising streak.

The Aussie Industrials broke their 5 weeks of consecutive advance.

Karachi fell and saw its 9 week winning streak end.

And the HSCEI and Hang Seng performed bearish outside reversals.

Commodities were mixed.

Hogs, Precious Metals, Coffee, Corn, Rice and Tin were amongst the notable gainers.

Palm Oil, LNG Gas, Palladium, Steel and Lumber dominated the losers category.

Rice rose and left the oversold region.

Richards Bay Coal, Lumber and U.S. Gulf urea prices are in 4 week losing streaks.

Arabica Coffee, Platinum, Tin and Uranium have risen for 4 weeks straight.

Robusta Coffee has climbed for 5 weeks.

Middle East Urea prices have risen for 9 weeks.

Cattle has closed higher for 10 straight weeks.

Henry Hub Natural Gas rose 8% and snapped a 5 week losing streak.

And Oats rose to break a 7 week losing streak.

Currencies were subdued.

The Aussie and Loonie were stronger.

The British Pound and Yen were slightly softer.

This saw the AUD/GBP rise and end its 4 week losing streak.

Euro was weaker.

USD/SEK has declined for 4 weeks.

And the NZD/AUD is a 5 week losing streak.

The larger advancers over the past week comprised of;

Baltic Dry Index 4.2%, North European Hot Rolled Coiled Steel 1.9%, Lean Hogs 4.2%, Arabica Coffee 2.1%, Lithium Carbonate 1.6%, Tin 3.8%, Natural Gas 8.2%, Nickel 2.1%, Robusta Coffee 3.6%, uranium 3.2%, Silver in AUD 1.4%, Silver in USD 2.1%, Gold in AUD 1.5%, Gold in CAD 1.6%, Gold in CHF 2.2%, Gold in EUR 2.6%, Gold in GBP 2.4%, Gold in USD 2.2%, Gold in ZAR 3.5%, Corn 2.1%, Oats 2.2%, Rice 2.9%, Wheat 1.3%, CSI 300 2.7%, KBW Banks 1.9%, FCATC 3%, BOVESPA 2.5%, TAEIX 2%, TA35 2.5%, Vietnam 2.2%, ASX Materials 2.6% and ASX Small Caps rose 3.1%.

The group of largest decliners from the week included;

Palm Oil (3.3%), Heating Oil (1.5%), HRC (4.1%), JKM LNG (2.9%), Lumber (9%), LNG in Yen (5.6%), Palladium (2.5%), Gasoline (1.3%), Dutch TTF Gas (6.4%), AEX (1.8%), ATX (3.6%), BUX (2.8%), CAC (3.3%), DAX (1.9%), MIB (2.6%), HSCEI (1.5%), IBEX (3%), IDX (2.8%), FTSE 250 (2.1%), NIFTY (1.8%), Copenhagen (2.8%), Helsinki (1.8%), Stockholm (2.4%), PSE (2%), PX (1.4%), SENSEX (1.8%), SET (1.3%), SOX (1.5%), Nasdaq Transport (2.3%), WIG (2.7%) and the FTSE 100 fell 1.4%.

August 31, 2025

By Rob Zdravevski

August 30, 2025 Leave a comment

This is 6th notable moment that the Canadian Dollar is trading at extreme pricing versus the Euro, over the past 20 years.

While not all of my qualifying metrics aren’t shown for reasons to not upset my paying clients, there are many tangents and derivatives that spin off from this observation.

August 29, 2025

by Rob Zdravevski

rob@karriasset.com.au

August 24, 2025 Leave a comment

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

n.b. pricing of (commodity) futures contracts is only considering the immediate front month.

* denotes multiple week inclusion

Extremes above the Mean (at least 2.5 standard deviations)

Austrian, Chinese, British and Dutch 10 year government bond yields

British 30 year bond yields

FCATC Index *

Overbought (RSI > 70)

Indian 10 year government bond yields

Cattle *

Urea (Middle East) prices *

All World Developed (ex USA) equity index

Hungary’s BUX Index *

Egypt’s EGX 30 equity index *

Italy’s MIB

Spain’s IBEX *

Pakistan’s KSE Index *

South Korea’s KOSPI *

Czechia’s PX Index *

South Africa’s SA40 *

Chile’s IGPA and IPSA indices

Isreal’s TA35

Canada’s TSX *

FTSE 100

Vietnam’s VN Index *

The ASX 200 *

ASX Industrials

And the ASX Small Cap Index *

The Overbought Quinella (Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Shanghai Composite Index *

CSI 300

China’s A50 equity index

Extremes below the Mean (at least 2.5 standard deviations)

Rice

AUD/SGD

NZD/USD

Oversold (RSI < 30)

Indonesian 10 year government bond yield

Lumber *

CAD/EUR

The Oversold Quinella (Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

U.S. 3 month bill yield

Notes & Ideas:

Government bond yields fell……

with the exception of British, Japanese and Brazilians.

Turkish 10 year and Chilean 2 year yields rose and broke their 4 week declining streaks.

U.S. 3 month bill are oversold this week and in a 4 week losing streak.

Indian 10’s have climbed for 7 weeks.

Russian 10 year bonds yield rose and broke 13 straight weeks of decline.

Equities rose nearly everywhere, again.

This week sees the FTSE 100 and the ASX Industrials join many other overbought indices.

While Chinese indices register an overbought extreme quinella.

The Nordic bourse, U.S. midcaps, U.S. banks and Aussie financials all had a good week.

Czechia’s OX Index fell and ended a 7 week winning streak.

Bangkok fell and broke its 8 week winning streak.

Karachi is in a 9 week winning streak.

Commodities were mainly firmer.

Oils, Gases, Precious Metals, Coffee and Cattle were the notable gainers.

Coal, Cocoa, Orange Juice, Oats and Rice dominated the losers category.

This week Lithium Hydroxide followed its Carbonate peer leaving oversold territory

Palladium, Wheat and Hesting Oil rose and broke its 4-week losing streak.

Robusta Coffee and Cattle prices are in a 9-week winning streak.

Henry Hub Natural Gas is in a 5-week losing streak.

And Oats have fallen for 7 weeks.

Currencies saw some movement.

The Aussie and Loonie were weaker, again.

Swissie rose, again.

The USD was mostly weaker, again.

The BRL/USD fell to end its 4 straight weeks of gains.

The Colombina Peso has risen for 4 weeks against the USD.

The AUD has fallen for 4 weeks against the GBP.

The Yen and Euro were firmer.

And the U.S. Dollar fell versus the Indian Rupee to end its 7-week rising streak.

The larger advancers over the past week comprised of;

Bloomberg Commodity Index 1.3%, Brent Crude Oil 2.9%, WTI Crude Oil 2.7%, Cattle 3.1%, Heating Oil 3.7%, JKM LNG 5.5%, Arabica Coffee 13.2%, LNG in Yen 2.2%, Gasoline 4.5%, Robusta Coffee 15.8%, S&P GSCI 2%, CRB Index 1.5%, Dutch TTF Gas 8.2%, Gasoil 3.7%, Uranium 1.7%, Silver in AUD 2.5%, Silver in USD 2.3%, Soybean 1.5%, Shanghai 3.5%, CSI 300 4.2%, AEX 1.9%, KBW Banks 3.5%, China A50 4.7%, DJ Industrials 1.6%, DJ Transports 2.8%, Oslo 1.9%, Copenhagen 3.7%, Helsinki 1.9%, Stockholm 1.8%, SMI 1.6%, S&P 500 0.3%, Nasdaq Transports 1.5%, TSX 1.5%, FTSE 100 2%, ASX Financials 3.5%, ASX Industrials 2.5% and BIST rose 4.6%.

The group of largest decliners from the week included;

Australian Coking Coal (3.3%), Baltic Dry Index (4.9%), Cocoa (6%), Natural Gas (7.5%), Orange Juice (2.1%), Oats (2.7%), Rice (8.2%), ATX (1.2%), TAIEX (2.3%), Nasdaq Composite (0.6%), KOSPI (1.8%), Nikkei 225 (1.7%), WIG (1.6%) and the ASX Materials fell 2.4%.

August 24, 2025

By Rob Zdravevski

August 18, 2025 Leave a comment

It’s been 4 years since the ASX Small Caps Index has been this type of overbought.

August 18, 2025

rob@karriasset.com.au