The following assets (on a weekly timeframe) registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

U.S. 30 year government bond yield

EUR/GBP

Overbought (RSI > 70)

U.S. 2 year government bond yield

Spanish, French and Italian 10 year government bond yield

TBT

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

U.K. 10 year government bond yields

U.S. 20 year government bond yields

German 2 & 5 year government bond yields

Extremes “below” the Mean (at least 2.5 standard deviations)

CAD/USD

SGD/USD

Oversold (RSI < 30)

U.S. 5 year minus U.S.3 month government bond yield ‘spread’ (not inverted)

TLT

Tin

GBP/USD

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

CNH/USD

KRW/USD

JPY/USD

Notes & Ideas:

The big news for the week includes Government bond yield are amongst the ‘overbought’s’, the bounce in only some equity markets and the continued strength of the U.S. Dollar.

So telling is the strength of the USD, the Japanese Yen is now at a 24 year low against the USD. That’s September 1998.

While the British Pounds seems to be the most weakest amongst the G7. It is registering extremes lows against the USD, EUR and the AUD…..I’ll take a look at buying Sterling.

In last week’s edition, I wrote;

Government bond yields are approaching their next round of being overbought, as are Cattle prices.

<the former are so, the latter is closing in>

Gold, Silver and Platinum are nearing buys,

<Gold was flat, while Silver rose 4% and Platinum soared 7% for the week>

Last week I mentioned that the Shanghai Composite, Copper and the U.S. KBW Banking Index had traded back down to their respective 200 week moving average for the second time in as many months.

This week, they appear amongst the gainers.

In other notes, the DXY is no longer Overbought while Hot Rolled Coiled Steel moves out of Oversold territory.

Palladium, MidCap 400, the KBW Banks, Nasdaq 100 and S&P 500 all performed an Outside Bullish Reversal week. The Russell 2000 did not.

The HSCEI and Hang Seng made lower lows. Look for more weakness, which should culminate into a buying opportunity.

Aluminium and Copper both mean reverted to their 200 week moving average, with the latter doing so for the 2nd tine in as many months.

The Nasdaq biotechnology index is 23% above its mid-June 2022 intra-day low.

For perspective, much of the rise in U.S. equities merely recovered some or all of the previous week’s decline.

For example, the MidCap 400 and SmallCap 600 fell 4% last week to see a 4% this week.

Similarly, the S&P 500 made up all of last week’s 3.3% fan with a 3.7% bounce.

The Philadelphia Semiconductor Index fell 7.1% a week earlier and clawed back 4.7% this week

And while S&P 500 didn’t manage to revert to mean its 200 week moving average in mid-June 2022, it can do so in the coming weeks without creating a ‘lower low’ of the June prices.

The mean is rolling higher, which is knowns as convergence.

The larger advancers over the past week comprised of;

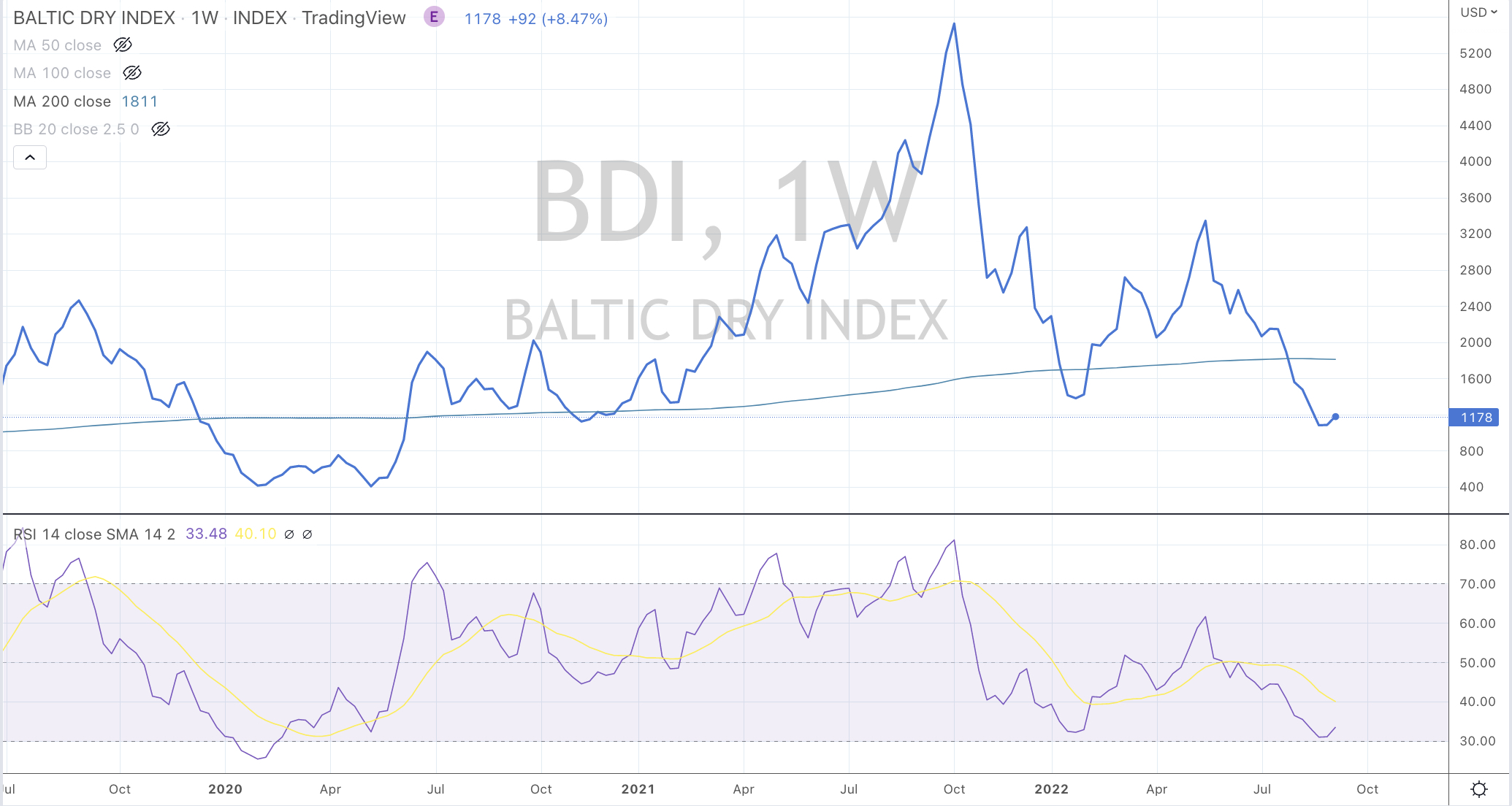

Baltic Dry Index 11.7%, China Coal 6%, Lean Hogs 3.5%, Copper 4.5%, HRC 4.9%, Lumber 7.2%, Palladium 7.5%, Platinum 7.2%, Uranium 5.7%, Silver in AUD 3.8%, Silver in USD 4.3%, Corn 2.9%, Oats3.6%, Wheat 7.2%, Shanghai 2.4%, KBW Banks 5%, CSI 300 1.7%, Dow Jones Industrials 2.7%, DJ Transports 2.4%, S&P MidCap 400 4.4%, Nasdaq 100 4.1%, Nikkei 2%, Russell 2000 4%, SOX 4.7%, S&P 500 3.7%, STI 1.8%, Istanbul’s BIST 4.5%, Toronto’s TSX 2.6%, S&P SmallCap 600 2.8% (partially recovering last week’s decline of 5.2%), Nasdaq Biotechnology 5.5%, Nasdaq Composite 4.1% and Australia’s ASX 200 recouped a fraction of the previous week’s 3.9% decline, it rose 1%.

The group of decliners included;

Australian Coking Coal (2.3%), Rotterdam Coal(10.4%), Cocoa (2.3%), Gasoil (2.9%), JKM (2.4%), Tin (6.9%), Natural Gas (9%), Orange Juice (1.9%), Dutch TTF (3.5%), U.S. Gulf Coast Urea (5.4%), Middle East Urea (8.3%) and Oslo’s equity index fell 2.4%.

September 10, 2022

by Rob Zdravevski

rob@karriasset.com.au