30 year bond yield triples

September 19, 2022 Leave a comment

It’s the quantum of the rate rises which I am watching.

When you have a lot of debt and potentially stretched, it doesn’t matter what the absolute interest rate is.

You risk being wiped out if you can’t service the interest payments once your interest cost triples.

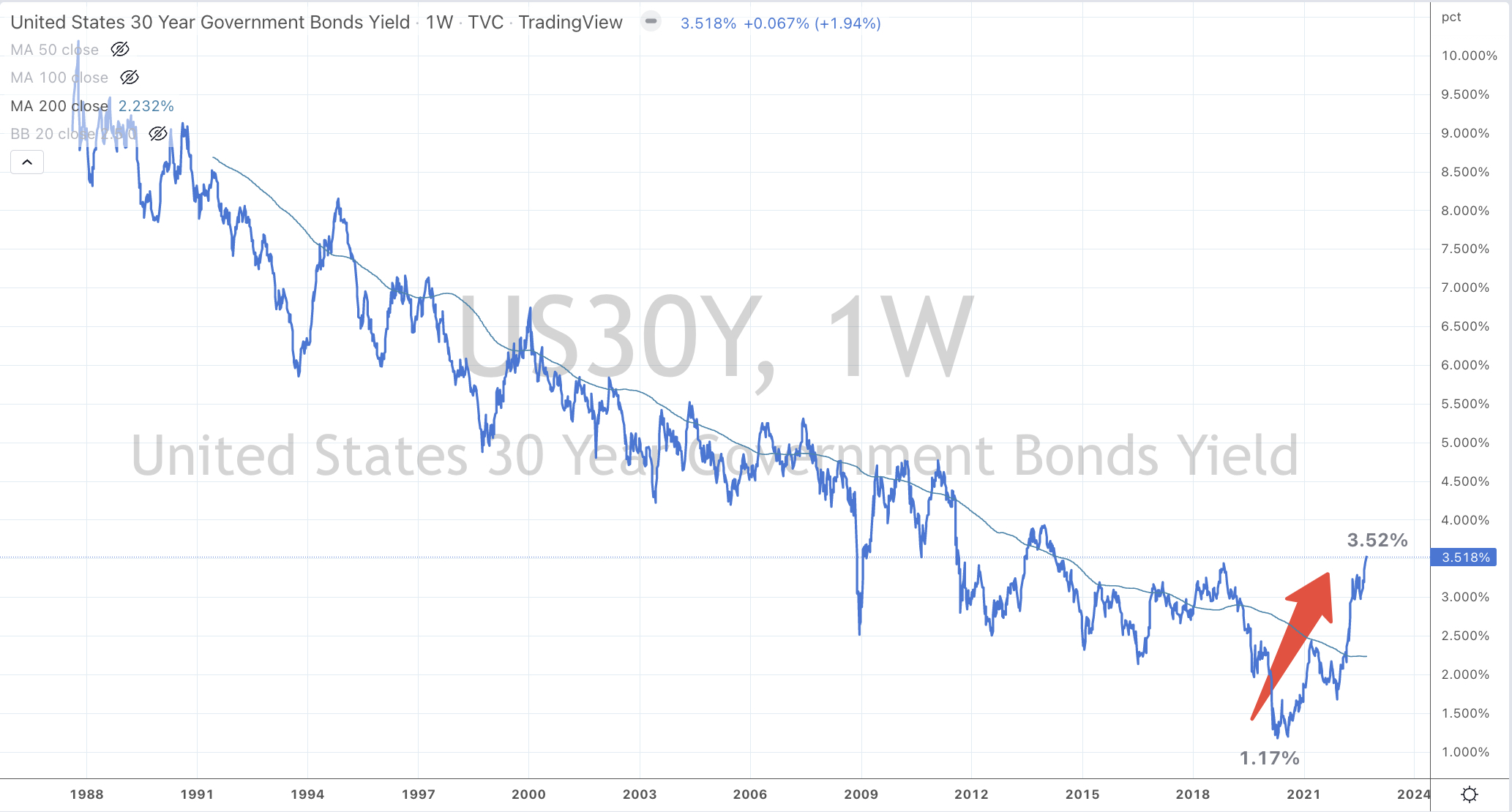

The chart below shows the travels of the U.S. 30 year government bond yield.

When rates were 6% in 1993 and then rose to 8% by 1995, it’s only a rise of 33%.

A rise from 5% to 6.7% as seen in 1998-2000 was only 33%.

During 2012-2014, 30 year rates moved from 2.5% to 3.9%. That’s an increase of only 55%.

The current rate cycle equals an increase of 300%.

My analysis is focused on the quantum of rate rises required, in order to temper credit applications and expansion which when combined with rhetoric will hopefully achieve the desired moderation of inflation.

And when we look at the developed world, we are much more closer to the end of the rate hikes than the beginning.

If the quantum of the rate rises expands, then there is risk to that large asset class known as residential real estate.

After all, the citizens of the developed world are awfully indebted while those in the developing economies (mentioned in the post below) have already experienced rate hikes of between 10 and 13 fold.

You can call it ‘front loading’ or anything else, but the cash rates along with 1, 2 or 3 year government yields of the developed world economies have already risen by the same factor of between 10 and 13 times.

So all this energy spent debating on where G12 central banks need to raise the absolute rate to, is futile.

But for the record, Canada currently has the highest interest rate out of all the G12 and a commodity sensitive (exporting) nation, they will a central bank to monitor for they have increased their policy rate 13 fold from 0.25% to 3.25%. The next BOC meeting is on October 26, 2022.

It’s time to get used to a new interest rate base from which central banks will work from and the investing effect is clear.

The absolute cost of capital has markedly increased and the return on investments will be adjusted lower.

September 19, 2022

by Rob Zdravevski

rob@karriasset.com.au