Macro Extremes (week ending May 27, 2022)

May 29, 2022 Leave a comment

The following assets (on a weekly timeframe) registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

EUR/GBP

Overbought (RSI > 70)

Australian 2, 3, 5 & 10 year government bond yields

German, Spanish, French, Greek, Italian and Portuguese 10 year government bond yields

U.S. 2 government bond year yields

U.S. Dollar (DXY) Index

Natural Gas

Gasoline

CRB Index

Bloomberg Commodity Index

WTI Crude Oil (September ’22 and December ’22 contracts)

USD/JPY

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

None

Extremes “below” the Mean (at least 2.5 standard deviations)

HKD/USD

CNH/USD

Dow Jones Transports

S&P 400 Mid Cap index

Nasdaq Transports

S&P 600 Small Caps

Oversold (RSI < 30)

JPY/USD

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

None

Notes & Ideas:

The big news for the week was the stunning bounce in global equity indices especially in the United States.

Musings in recent edition of ‘Macro Extremes’ about Oversold moments and a 7th consecutive weekly decline in some indices portended a change of direction.

Calling such a low was highlighted in my newsletter released earlier in the week

https://mailchi.mp/karriasset/buy-signals-appearing

And in other posts such as;

https://robzdravevski.com/2022/05/21/a-different-way-looking-at-the-nasdaq/

https://robzdravevski.com/2022/05/20/a-rare-oversold-moment-for-the-sp-500/

https://robzdravevski.com/2022/05/12/mean-reversion-is-a-happening-thing/

Keep in mind that it doesn’t mean a change of trend, but merely a break of a streak.

Incidentally, there is little news in the financial media reporting that last week’s advance added a certain amount of trillions in market capitalisation, while we only hear of the trillions ‘wiped’ or ‘lost’…….and never about the trillions which are ‘found’.

In other news, the 5 and 10 year U.S. government bond yields are not Overbought.

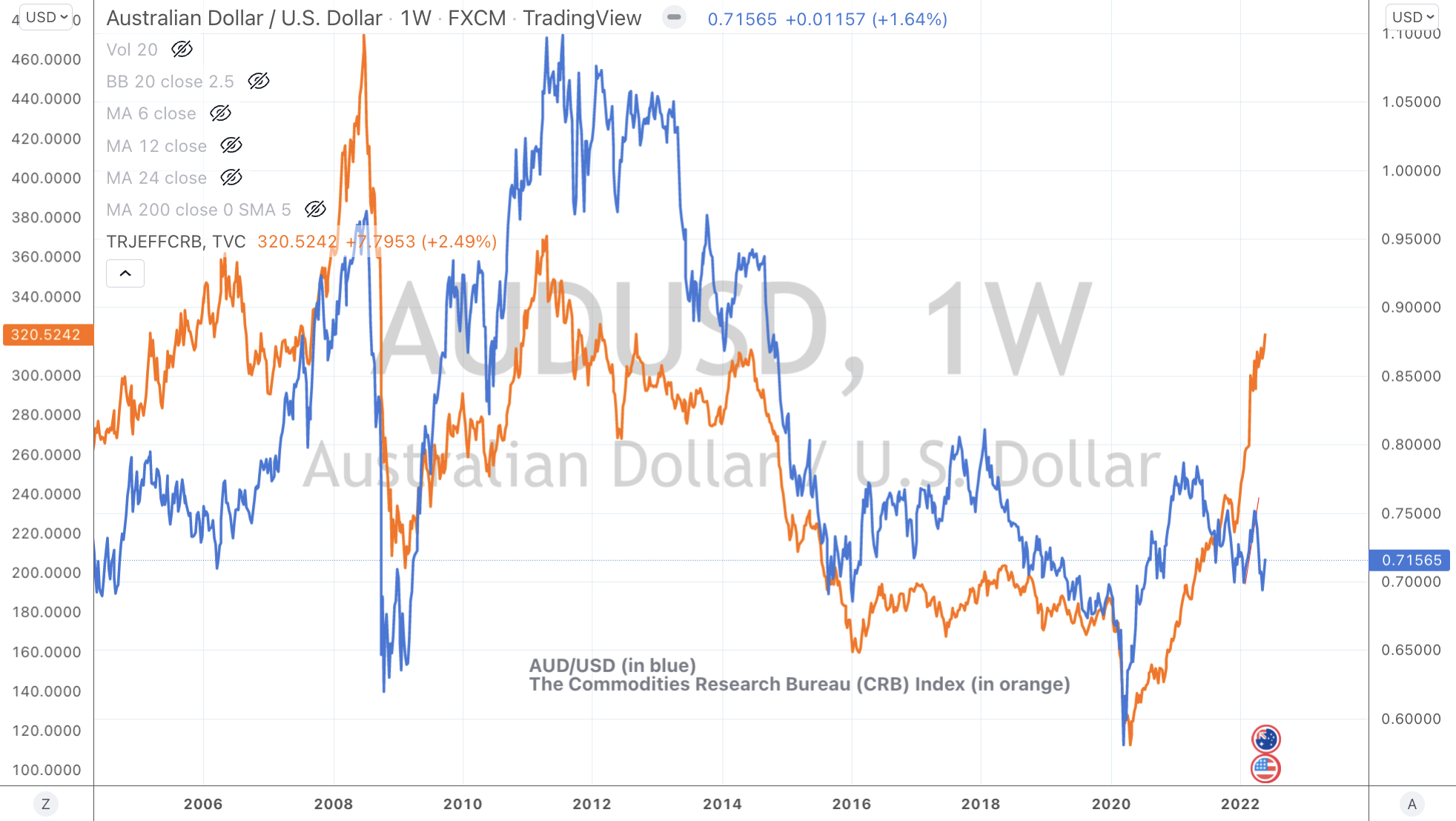

While the CRB (commodities) Index remains overbought, for the 19th consecutive week….the U.S. Dollar Index (DXY) ended 6 consecutive week of ‘overboughtness’.

The chart below shows the recent divergence of the AUD/USD and broader commodity prices.

Probability is increasing of a weaker US dollar as a means of simply retracing the recent bullish move, although there isn’t much talk about commodity prices easing, let alone reverting to any chosen mean.

The Baltic Dry Index (shipping costs) took a break and fell 20% following a 51% advance in the previous 6 weeks.

Bitcoin fell again (another 5%) and has declined 50% over the past 9 weeks.

The larger advancers over the past week comprised of;

Bloomberg Commodity Index 2.5%, China Coal 2.6%, WTI Crude 4.3%, Gasoil 9.4%, Heating Oil 7.1%, JKM LNG 3.7%, Coffee 6.3%, Lumber 4.2%, LNG 3.1%, Tin 3.3%, Natural Gas 8%, Orange Juice 6.2%, Palladium 5.4%, Gasoline 2%, Silver 2%, CRB Index 2.5%, Dutch TTF Gas 4.2%, Brent Crude 5.9%, Oats 14.9%, AEX 2.8%, KBW Banking Index 9.2%, French CAC 3.7%, German DAX 3.4%, Dow Jones Industrials 6.3%, DJ Transports 7.1%, Italy’s MIB 2.3%, Spain’s IBEX 5.3%, Bovespa 3.2%, S&P MidCap 400 6.5%, Nasdaq 100 7.2%, Osloa 3.1%, Helsinki 3.9%, Stockholm 3.2%, Russell 2000 6.5%, Swiss SMI 3%, Philadelphia Semiconductor (SOX) Index 8.1%, S&P 500 6.6%, U.K.’s FTSE 2.7%, Canada’s TSX 2.7%, S&P SmallCap 600 6.7%, Nasdaq Biotech Index 2.8% and Australia’s ASX 200 rose 0.5%.

The group of decliners included;

Baltic Dry Index (19.8%), Australian Coal (2%), Aluminium (2.6%), Rotterdam Coal (13.5%), Hot Rolled Coiled Steel (13.7%), Nickel (2.6%), Cotton (2%), Urea (5.1%), Bitcoin (4.6%), Ethereum (13.5%), Cardano (15.1%), CSI 300 (1.9%).

May 29, 2022

by Rob Zdravevski

rob@karriasset.com.au