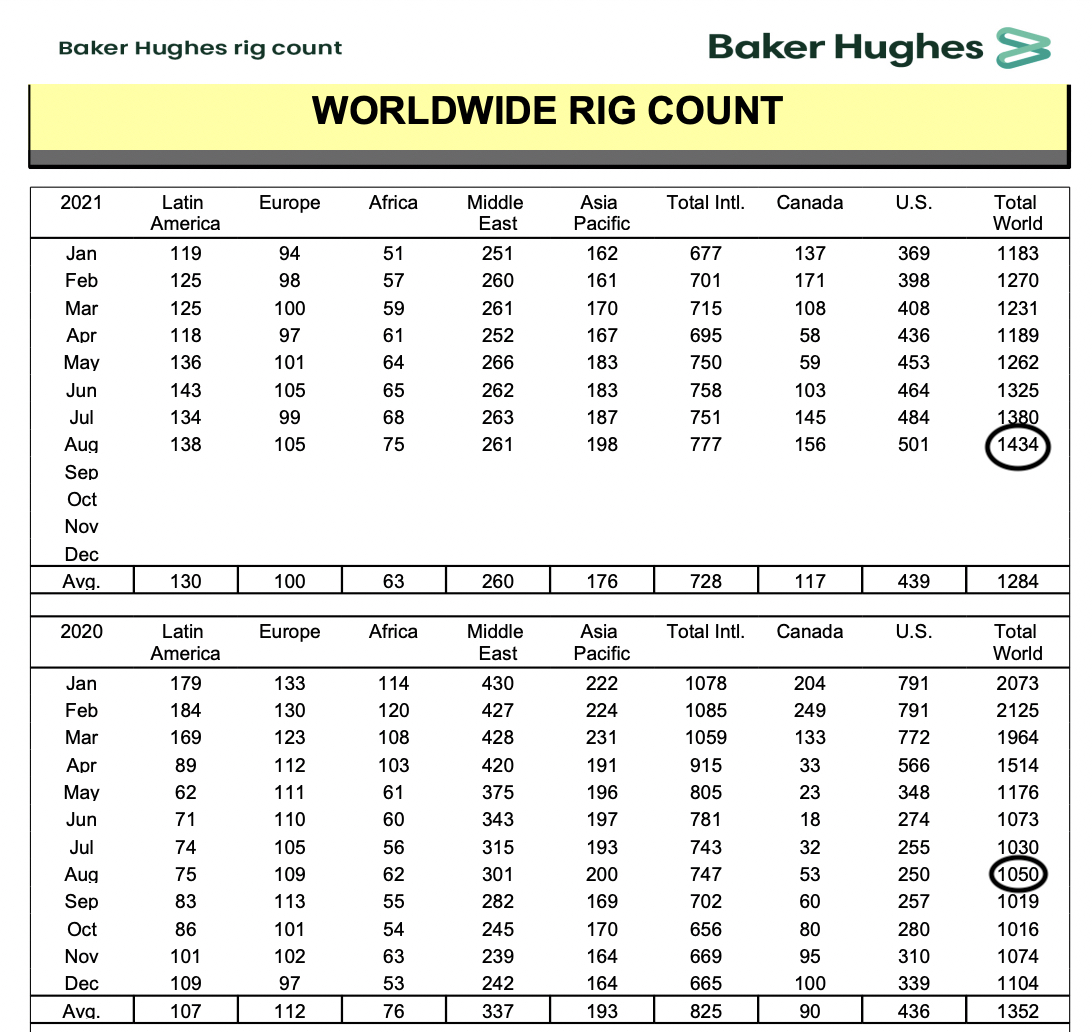

More rigs, more output, lower oil price

September 8, 2021 Leave a comment

Globally, 40% more oil and gas rigs have been put to work compared to 12 months ago.

In the U.S., the amount of rigs which snapped back to life doubled since last August.

Rigs in operation throughout Latin America have nearly doubled in number.

While the Canadian’s have trebled.

Interestingly, the amount of rigs deployed in the Middle East and Europe have declined.

Overall, more drilling leads to more output which puts a lid on the price of oil, which coincides with my bearish call on crude.

What else does the table below tell us?

The Saudi’s are trying to keep output tight in order to keep prices high, because ‘petro-nations’ need ‘petro-dollars’.

Carbon conscious Europe and their headquartered hydrocarbon giants (BP, Total, Statoil, Shell, Repsol, ENI) are trying to drill less.

The Americans need to drill to service the consuming citizens, make money, use their capex, satisfy shareholders and avoid being a net importer of oil.

And the Canadians are just ecstatic that extracting tar sands oil became economically viable again.

September 8, 2021

by Rob Zdravevski

rob@karriasset.com.au.