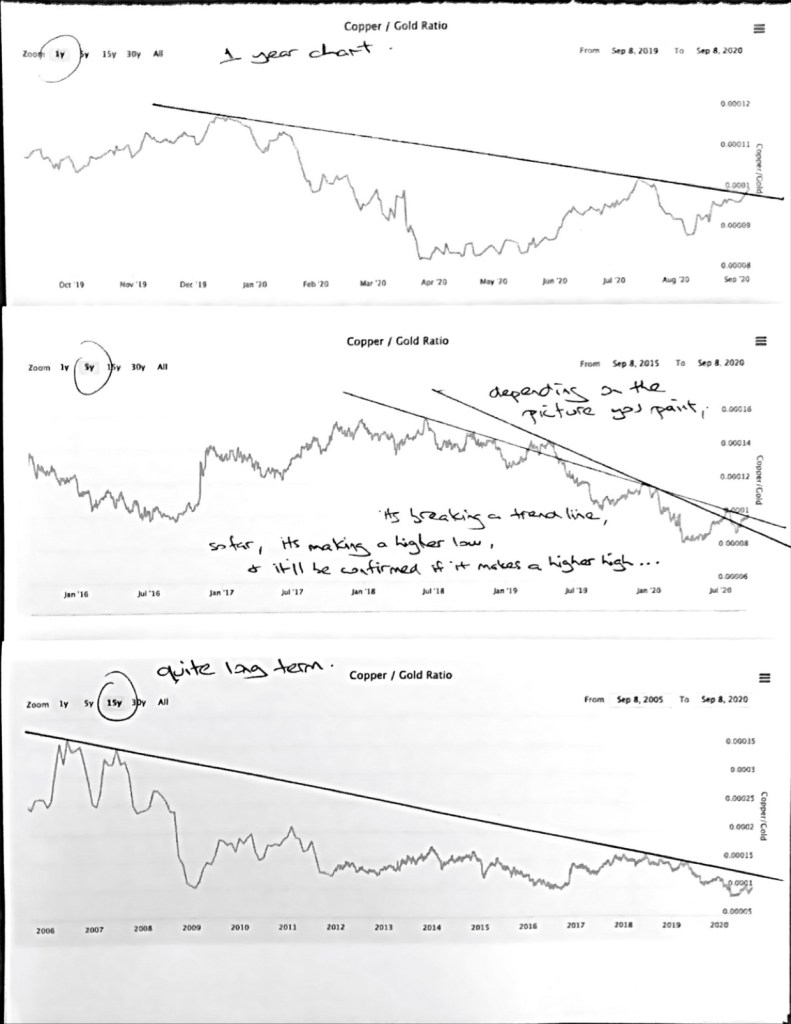

Predicting interest rates with the Copper/Gold Ratio

September 10, 2020 Leave a comment

Interest Rates at the longer end of the curve may be poised to rise.

I think many concur (mainly through central bank guidance) that shorter term rates will stay lower, for longer.

In the interim, I may have views that 10 & 20 year debt at the consumer levels may become cheaper (perhaps 2.8% for mortgages);

however my interest in the Gold/Copper ratio has less to do with predicting price action in those underlying commodities, but more so with the direction of U.S. government bond yields.

I think it is plausible that short term rates stay low but I think longer dated bonds will rise.

Take a look at my printed, line drawing, stacking different time line (1yr, 5yr & 15yr) charts on top of each other, old school effort below…..

FYI, today, the U.S. 10 year government bond is yielding 0.70%.

September 10, 2020

by Rob Zdravevski

rob@karriasset.com.au