The VIX is not what it seems

September 3, 2020 Leave a comment

I had a topical discussion with a peer about why the VIX is hovering around the 23 mark yet the S&P 500 is making new highs?

Today, the VIX rose again (to 26.6) while the S&P 500 and Nasdaq climbed 1.5%.

He pointed out that an extraordinary amount of call options are being traded compared to put options and this may be distorting the call/put calculation of the VIX and changing its traditional guide of measuring “fear” or risk.

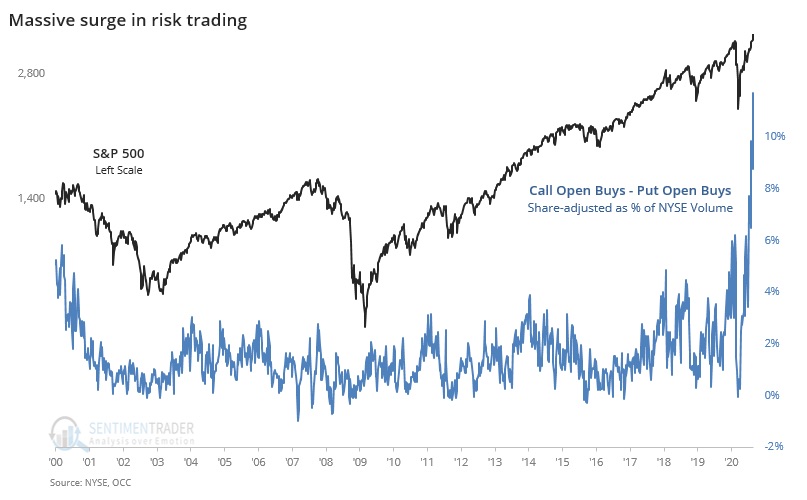

I found a reference that we are recently seeing something like $3 or $4 billion worth of call options traded each day versus the normal $1 billion.

Temporarily, this is changing the VIX’s behaviour and the indicator isn’t all that it seems.

Then I looked at the VXN (the Nasdaq’s volatility index) and it has been rising for 10 days all while the Nasdaq has also forged higher.

It should not be so correlated.

There is speculation in certain popular names which is dramatically pushing up the prices of call options associated with those companies, relative to their put options.

Speculative options trading is near 12% of the NYSE volume last week. (see graphic below)

And market makers who are selling call options to those speculative buyers are forced to hedge their position and buy the underlying shares.

September 3, 2020

by Rob Zdravevski

rob@karriasset.com.au