“It’s unlikely that automobile manufacturers will walk away from the capital expenditure spent on engine development and assembly, while synthetic fuels are making ICE’s even more cleaner.

Commensurate to introducing electric vehicles into their stable, auto companies have also made statements that they still expect the ICE to be part of their business for the next 30 years.

The note also observed Palladium’s premium above the price of Platinum (implying that the gap is narrowed as Palladium declines and Platinum rises) along with my expectation of mean reversion/convergence in the Gold price.

Gold did mean revert, Platinum rose and Palladium’s premium collapsed.

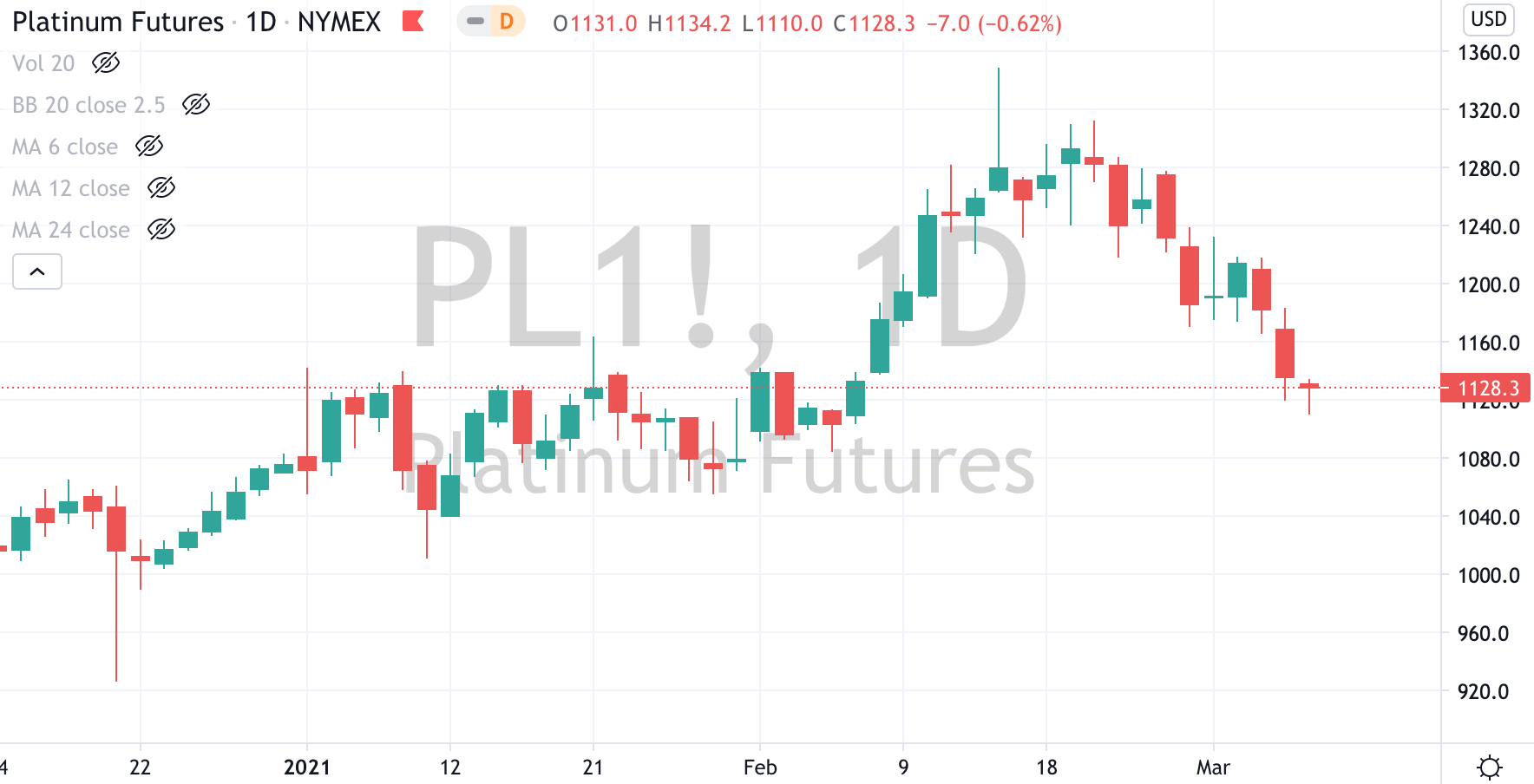

Since that note was published, both Platinum and Gold have risen 11%.

And Palladium is now cheaper than Platinum.

Now, Mercedes Benz has said it will continue to make combustion-engine and hybrid vehicles “well into the 2030s,” if demand is there.

What if I don’t want to own and drive an electric vehicle?

I think the internal combustion engine is being discriminated against.

What if specialty fuels solve the lower emissions equation?

Why have #ethanol and #biofuels seemingly been removed from the vernacular?

And what if #hydrogen becomes a ‘thing’?

In amongst the hypocrisy of the #carbon ‘intensity’ that an #electricvehicle requires (or attracts), the internal #combustion#engine is not the ogre for those concerned….it is the #fuel or #energy required to fill up (or recharge) the vehicle.

What if my examples provide cleaner sources of propulsion than the mystical trickle of #electricity into an #EV?

A bet that the Internal Combustion Engine still has 30 years of life

The Discount:

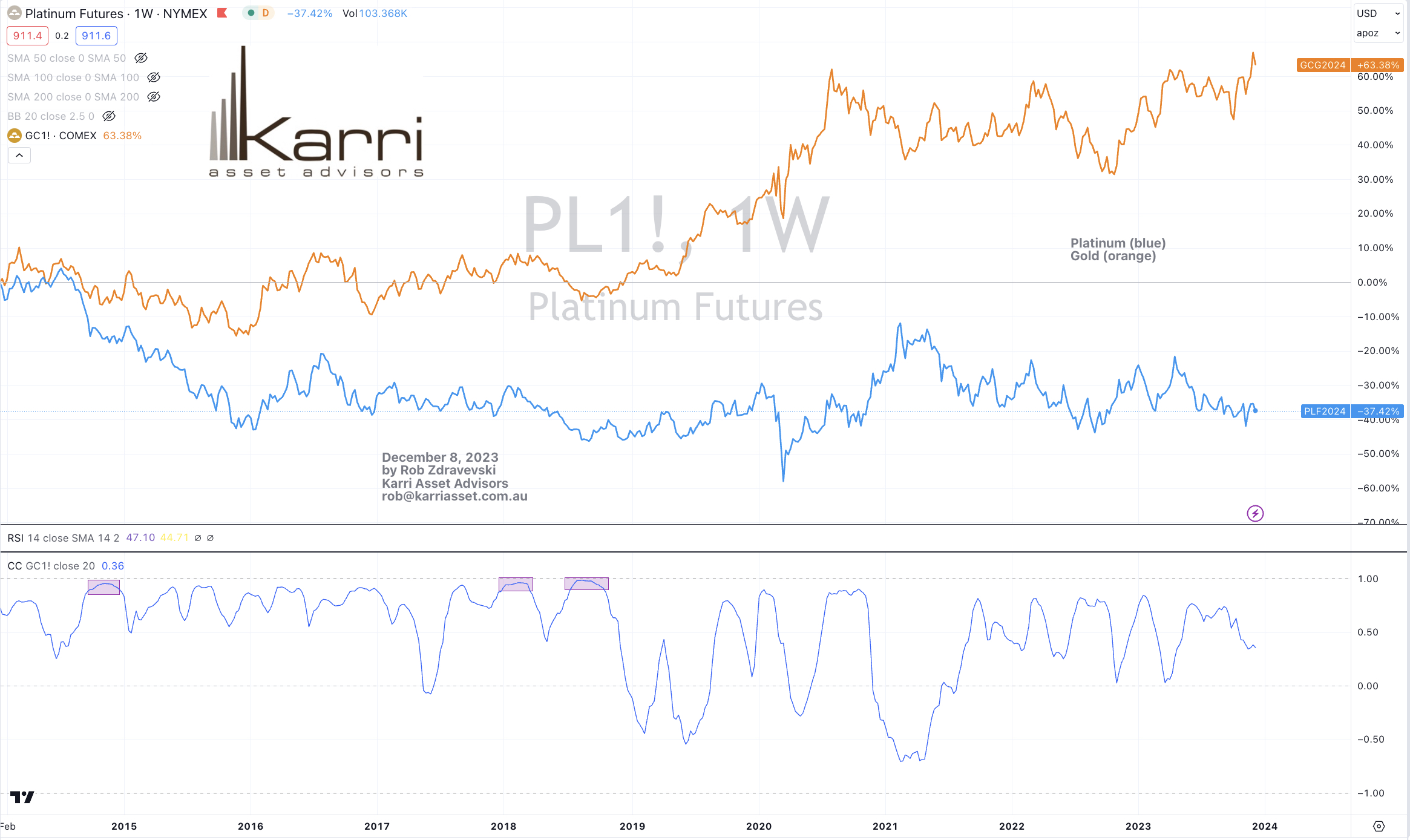

Colloquially, Platinum is considered more precious than Gold.

When it comes to pricing, Platinum has traded at either par or $200-$300 an ounce higher than the price of Gold.

In early 2015, Platinum started to consistently trade at a discount to the price of Gold.

Today, Platinum is trading at $1,000 below the price of Gold.

We haven’t seen such a percentage discount spread in 35 years.

Subjectively, there is a euphoria behind Gold’s prospects while Platinum is seemingly unloved which seems to have widened the discount.

Platinum (in orange) compared to Gold (blue line)

Production & Supply:

At least 70% of the world’s Platinum production is sourced from South Africa’s Bushveld region.

This allows us to easily monitor supply disruptions, labour disputes and political machinations.

COVID-19 has also seen the South African Government restrict mine production to a capacity of 50% and in turn, mining companies have elected to place various mines in ‘care and maintenance’.

Coupled with a latency in re-starting production, there is a distortion in price and supply upon us.

Industrial Use & a substitute for Palladium:

On the demand front, Platinum is used in ……..

jewellery, dental fillings, medical/laboratory instruments, turbine blades, computer hard disks, in the chemical industry (nitric acid, benzene, silicone), as compounds in chemotherapy drugs, as a catalyst making fuel cells more efficient and in motor vehicle engine catalytic converters.

Catalytic converters (in cars, trucks and buses) account for 50% of its utility.

On the topic of automobile catalytic converters, Palladium has been the preferred metal amongst manufacturers and rightfully so due to its lower price.

On an industrial basis, being Long Platinum is to take a view that the proliferation of vehicle electrification will take longer than suggested.

This is certainly a contrarian view.

Although, it has been noted that whenever Palladium trades at twice the price of Platinum, manufacturers opt for the cheaper Platinum substitute.

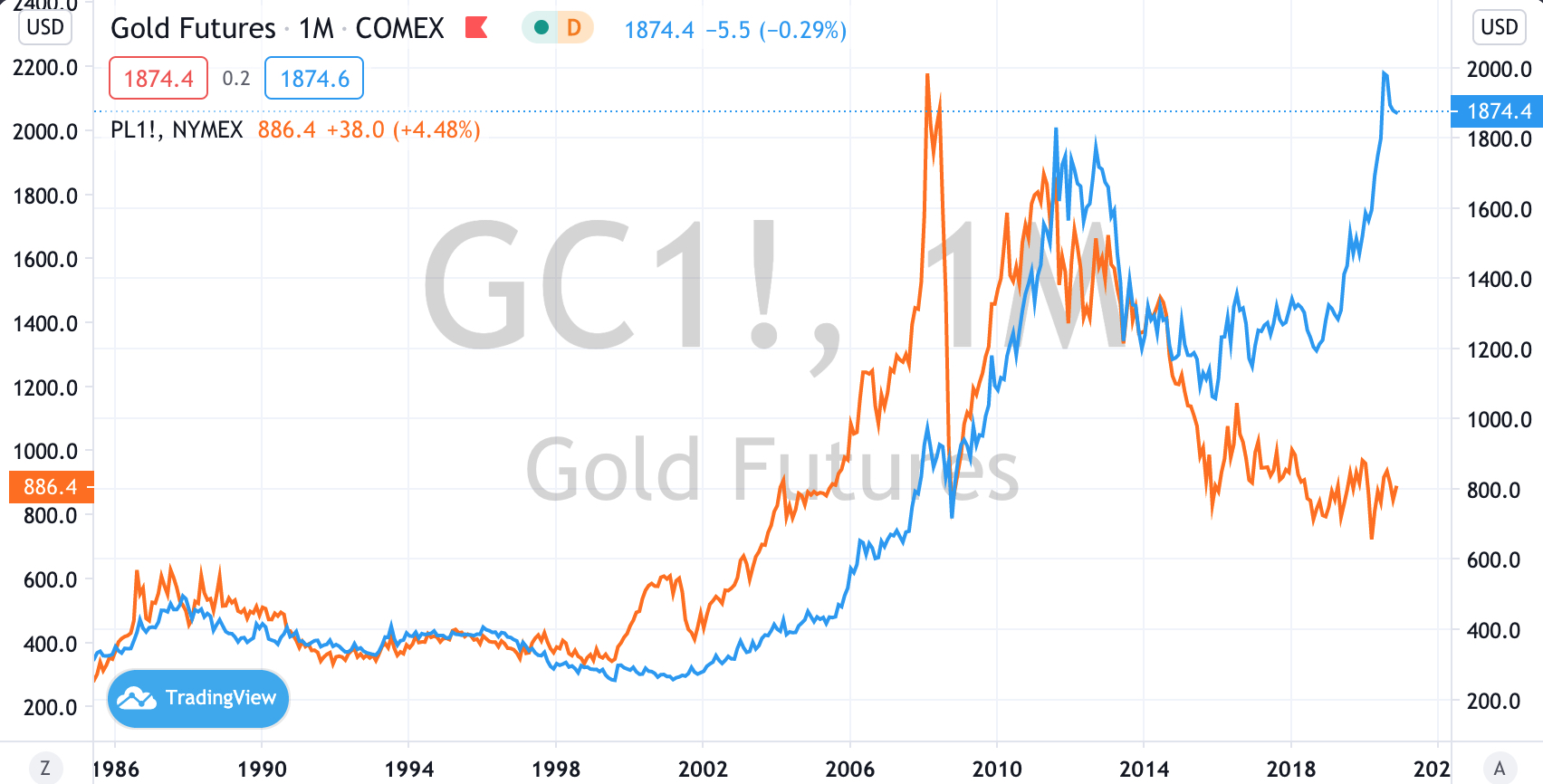

Today, Palladium is trading at $2,457 is trading nearly 3 times Platinum’s current price of $887.

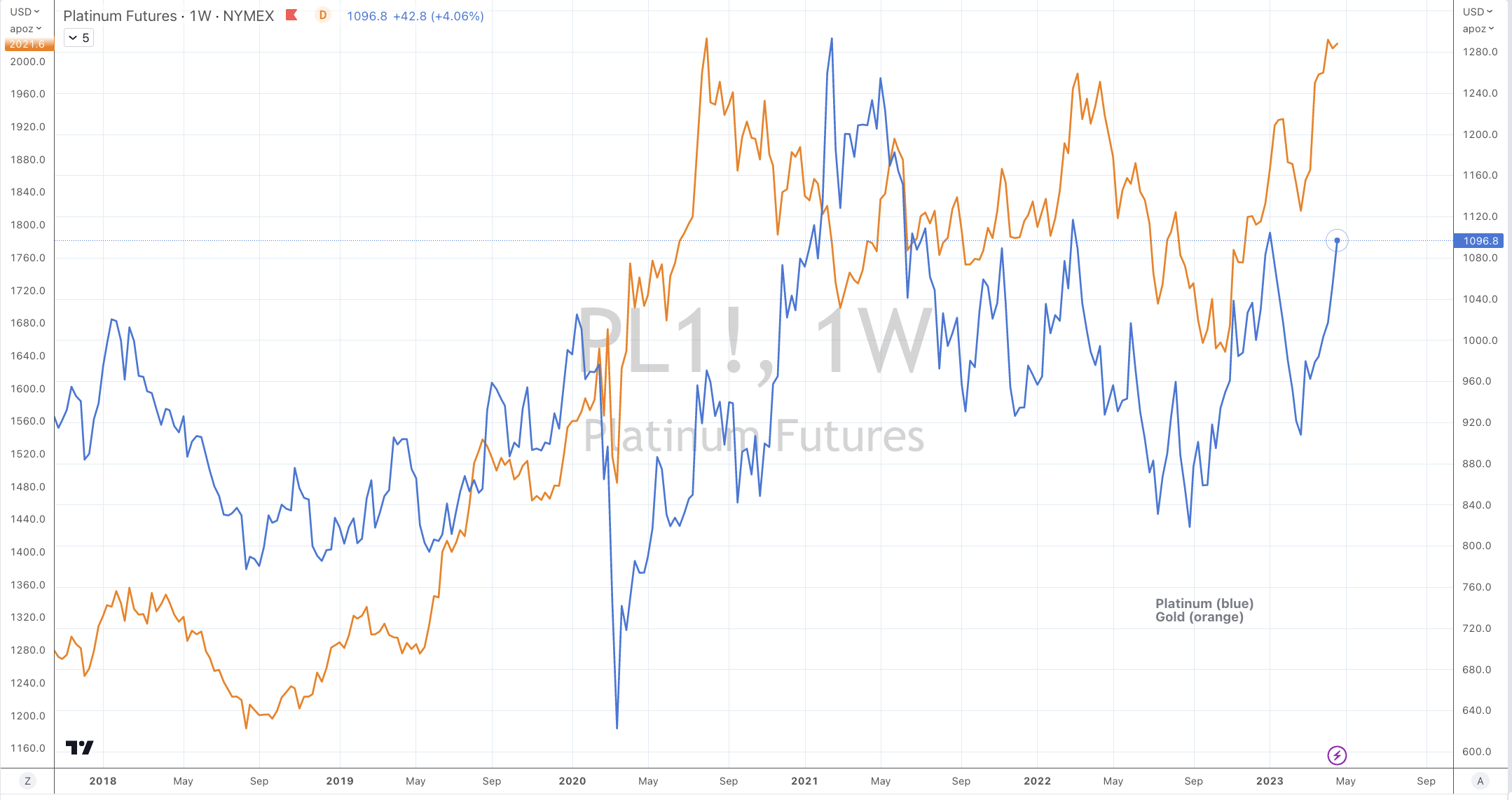

The price of Platinum appears in orange, while Palladium is in blue.

Mean Reversion

Gold is currently trading at 64% above its 200 day moving average (on a monthly basis) while Platinum is 27% below its monthly 200 DMA. It is plausible to expect a convergence and mean reversion in both assets.

When pondering how this gap will narrow, a rising Platinum price seems more probable than a collapse in the Gold price in the current asset and ‘expected’ price inflation environment.

Correlation to CME Futures Contract Margins:

The case for an interim peak (for Gold) also lies in my historical analysis of futures contract margin requirements tend to coincide with an extreme in the price of Gold.

Platinum’s futures margin requirements are not reaching any historical peaks. In fact, I think there is growing probability that Platinum margins are decreased soon.

The Internal Combustion Engine (ICE)

It’s unlikely that automobile manufacturers will walk away from the capital expenditure spent on engine development and assembly, while synthetic fuels are making ICE’s even more cleaner.

Commensurate to introducing electric vehicles into their stable, auto companies have also made statements that they still expect the ICE to be part of their business for the next 30 years.

Incumbent industry and job protectionism is another topic that won’t dissipate anytime soon.

Electric Vehicles (EV)

While their purchase is subsidised in many jurisdictions, EV’s remain expensive and have yet to reach a pricing equilibrium making them affordable and a mass viable financial alternative to owning an ICE vehicle.

The EV charging network isn’t widespread and will require notable investment while facing a formidable fuel retailing industry. Range anxiety and the speed of re-charging also remains a challenge.

Hence, EV’s account for 2.5% of global car sales and 1% of the global car ‘population’.

Bloomberg New Energy Finance predicts that electric vehicles (EVs) will hit 10% of global passenger vehicle sales in 2025, with that number rising to 28% in 2030 and 58% in 2040.

I’m not hanging onto the past and while EV market penetration should grow; we are still making cars, trucks and buses with ICE’s.

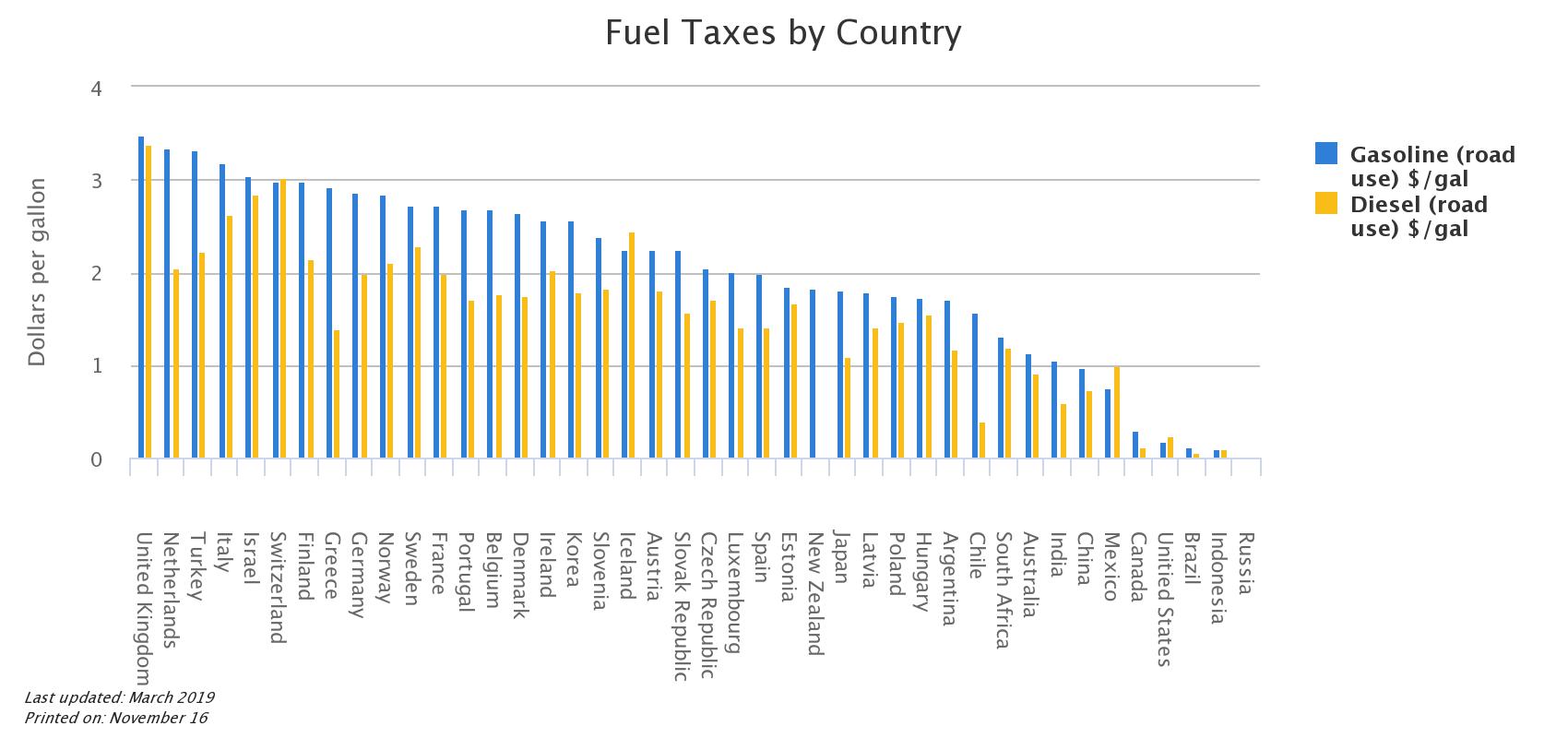

Government & Tax

Government love things which they know how to tax; items such as tobacco, alcohol and fuel.

The fuel excise tax is a hefty component of many government revenues and the funds raised assist with maintaining not only roads & bridges, but also hospitals and schools.

EV’s are currently not providing a comparable revenue replacement for potential lost petroleum taxes.

Another challenge for governments is figuring out how to tax the electricity trickle from your residential power outlet, the solar panels located on your roof or from a public charging station.

We are now seeing governments announces “road usage taxes” for EV’s.