A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

Russian 10 year government bond yield

Australian Coking Coal

Nasdaq Composite and Nasdaq 100 Index

Overbought (RSI > 70)

German 2 year government bond yields

Cattle

Italy’s MIB equity index

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

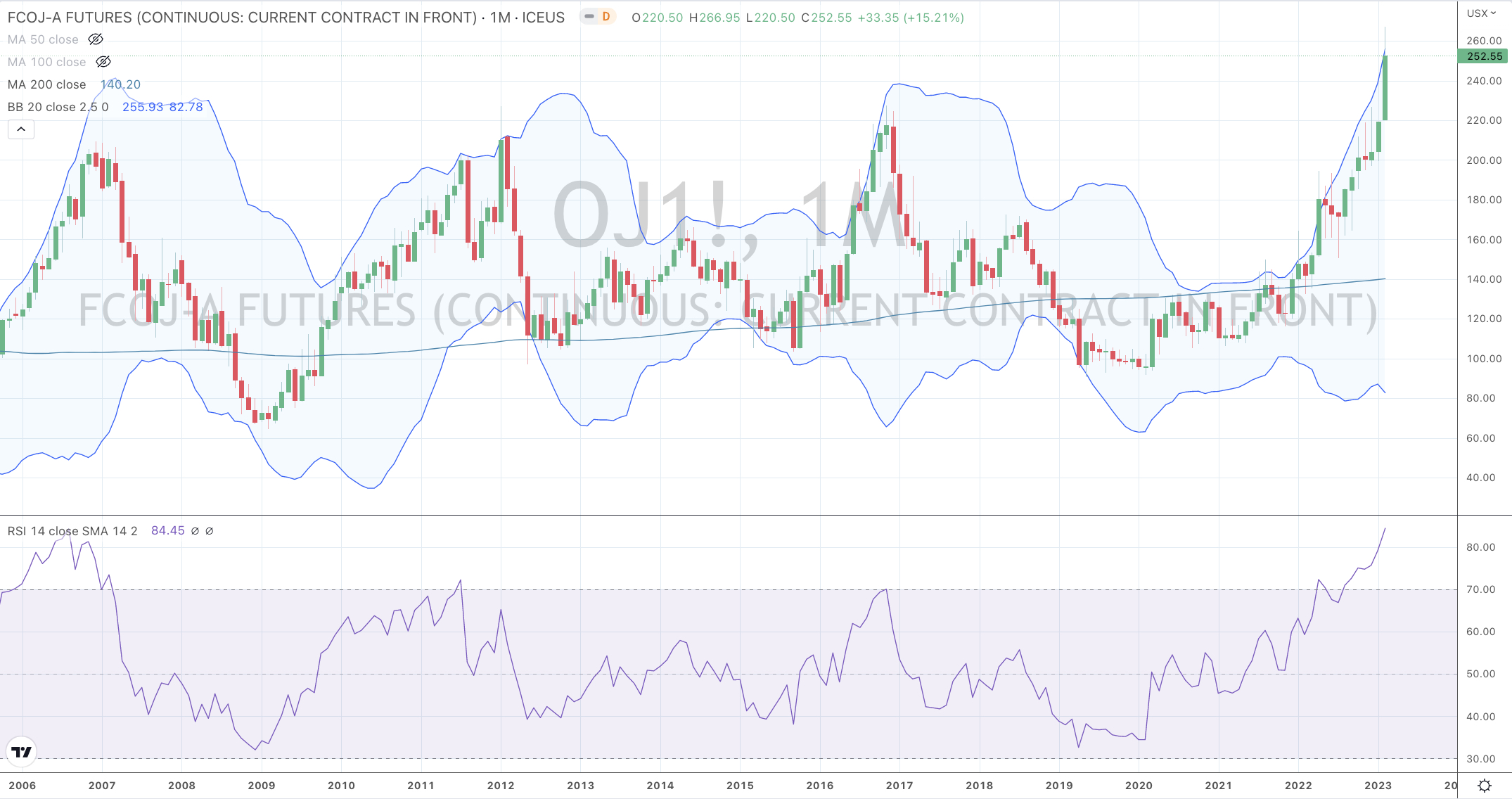

Orange Juice

Extremes “below” the Mean (at least 2.5 standard deviations)

None

Oversold (RSI < 30)

U.S. 5 year yield minus U.S. 3 month bill yield spread

Natural Gas

Urea (U.S. Gulf)

Urea (Middle East)

Baltic Dry Index

Rotterdam Coal

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

None

Notes & Ideas:

This week’s edition is complimented by referencing last week’s.

Those who exhibited ‘extremes’ then, aren’t now.

Equities were mostly flat. They were so benign that we saw many ‘inside weeks’.

Any notable losses were seen in the U.S. and Scandinavia.

Understandably, Turkish equities slumped (10%) during the week.

Although, the larger news is that the indices which appeared Overbought in last week’s are not, this week.

Amongst bonds, yields generally rose. The U.S. 2 year closed at its highest level since November 14, 2022.

In commodities, energy prices understandably bounced while precious metals eased with Lumber, Tin and Aluminium being the more notable decliners.

Natural Gas rose 4.3% for week. The probability of a positive week grew after the commodity completed its 7th consecutive losing week and simultaneously touched Oversold extremes…..

Speak of losing streaks, Urea (U.S. Gulf) has seen 9 consecutive losing weeks. To boot 13 of the last 14 weeks have been negative as have 18 of the last 21 weeks.

Palladium and Platinum prices have fallen 16% and 14% respectively over the past 5 weeks.

Dutch TTF Gas and Rotterdam delivered Coal finally mean reverted to their 200 week moving average, thus honouring a retracement of the extraordinary parabolic moves seen in 2021 and 2022.

The latter has tanked 51% in the past 10 weeks.

Platinum also performed the same mean reversion. Now watching for Brent Crude to do the same, which although rose 8% for the week, has generally traded sideways for 5 months as is the same price as September 19, 2022.

Softs are in no-man’s land.

Orange Juice has soared 22% in 2 weeks, Cattle is Overbought for the 17th consecutive week and Tin is no longer 2.5 standard deviations above its weekly mean.

The Japan Korea LNG Marker (JKM) touched its lowest price since August 30th, 2021.

Shipping Rates weakened further with the Baltic Dry Index notching up a 7 week losing streak.

And a positive is that Australian Coking Coal has risen 17% in the past 2 weeks and 41% over the past 7 weeks.

In currencies, it was a boring and listless week.

The larger advancers over the past week comprised of;

Australian Coking Coal 7.l%, Gasoil 2.1%, Heating Oil 3.2%, Natural Gas 4.3%, Orange Juice 4.5%, Gasoline 7.9%, CRB Index 2.4%, Brent Crude 8.4%, Rice 1.9%, Wheat 3.9% and Argentina’s MERVAL rose 5.1% (and 11% over the past 3 weeks)

The group of decliners included;

Aluminium (4.8%), Rotterdam Coal (4.7%), Baltic Dry Index (3.1%), JKM (2.9%), Lumber (16.1%), Tin (4.3%), Palladium (5.8%), Platinum (2.9%), Dutch TTF Gas (6.8%), Urea U.S. Gulf (6.5%), Urea Middle East (7.7%), Silver AUD & USD (1.5%), Oats (1.8%), KBW Banks (1.8%), HSCEI (3.5%), HSI (2.2%), Nasdaq Composite (2.4%), S&P MidCap 400 (2.6%), Nasdaq Biotech (2.6%), Nasdaq 100 (2.1%), S&P SmallCap 600 (3.6%), Helsinki (1.9%), Stockholm (4.1%), Russell 2000 (3.4%), Swiss SMI (1.9%), SOX (2.3%), Mexico (2.9%), DJ Transports (3.1%) and Istanbul’s BIST Index slumped 10.2%

For reference, the S&P 500 fell 1.1%, the DJ Industrials eased 0.2%, Toronto’s TSX fell 0.7%, the ASX 200 declined 1.7% and the ASX Small Caps swooned 4%.

February 12, 2023

by Rob Zdravevski

rob@karriasset.com.au