A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations

U.S. 5-7 year corporate bond yield

Australian, Brazilian, Chilean, Japanese, South Korean and U.S. 10 year government bond yield

Japanese 2 year government bond yields

U.S. 7 year government bond yields

U.S. 20 and 30 year government bond yields

TBT

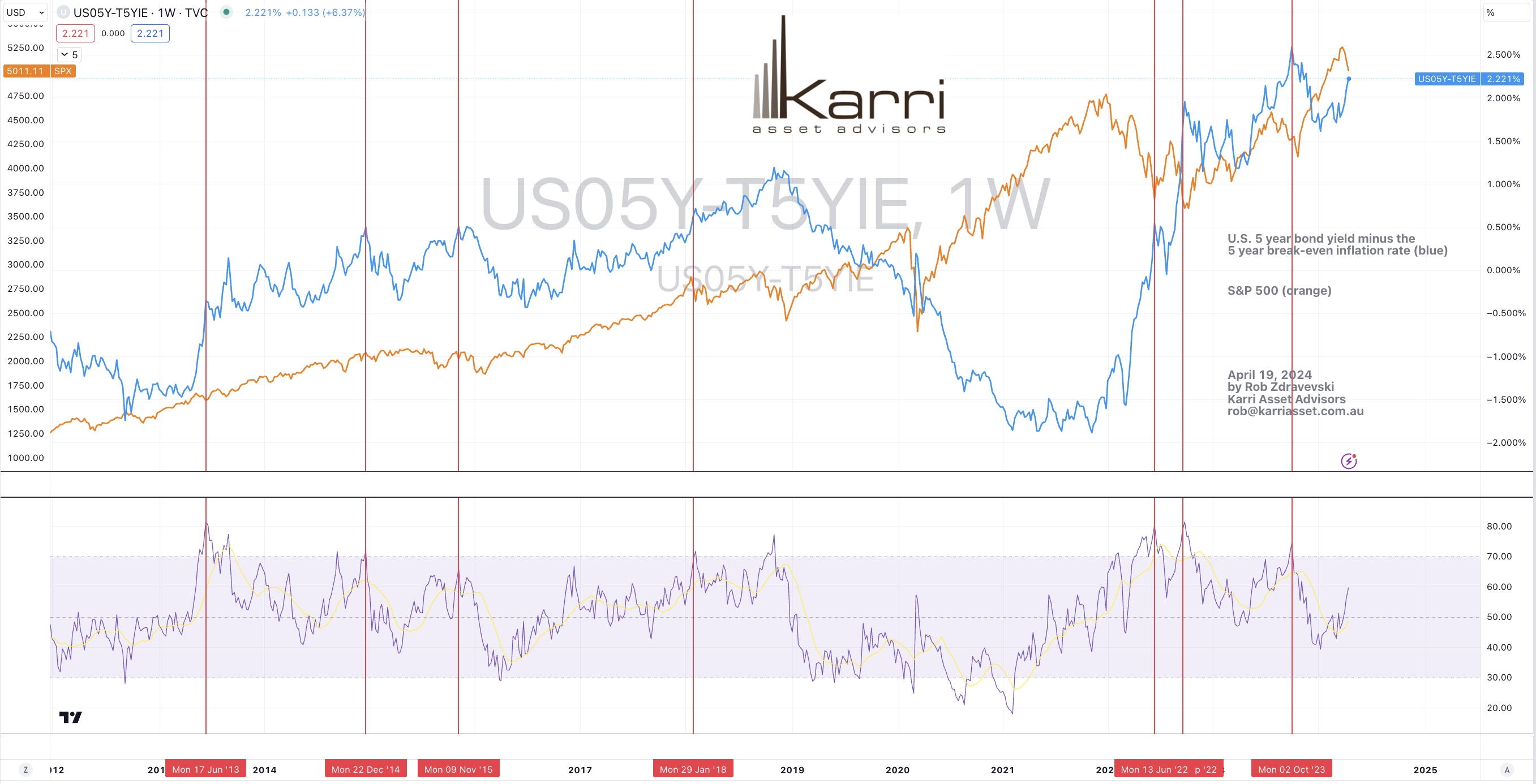

U.S. 5 year government bond yield minus U.S. 5 year inflation breakeven rate

U.S. 5 year government bond yield minus U.S. 3 month bill yield

U.S. 10 year government bond yield minus U.S. 10 year inflation breakeven rate

Gold Volatility Index

Cocoa

Nickel

Overbought (RSI > 70)

U.S. 10 year bond yield minus Australian 10 year bond yield

U.S. 10 year bond yield minus German 10 year bond yield

U.S. 10 year bond yield divided by Australian 10 year bond yield

Gold in CHF

CRB Index

Italy’s MIB

Russia’s MOEX

And Pakistan’s KSE Index

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Coffee (Arabica)

Coffee (Robusta)

Aluminium

Copper

Tin

Silver in AUD and USD

and Gold as priced in AUD, CAD, EUR, GBP, USD and ZAR

Extremes “below” the Mean (at least 2.5 standard deviations)

IEF

IEI

SHY

TLT

Australia 10 year yield minus U.S. 10 year yield

Urea (U.S. Gulf)

CAD/USD

GBP/USD

PHP/USD

DKK/USD

INR/USD

KRW/USD

SEK/USD

Dow Jones Transports

And Thailand’s SET Index

Oversold (RSI < 30)

Chinese 10 year government bond yields

Australian Coking Coal

Lithium Hydroxide

The Oversold Quinella – Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

Lumber

BRL/USD

IDR/USD

Notes & Ideas:

Government bond yields rose.

Chilean 10’s have risen for 6 consecutive weeks and have risen for 10 of the past 11.

Across the curve, British yields have climbed for 4 straight weeks as have South Korean and Japanese 10’s.

And Russian 10 year bond yields aren’t overbought anymore.

Equities broadly fell everywhere…..

with the exception of Chinese stocks and U.S. banks.

Impressively the Dow Jones Industrials were flat for the week.

The Russell 2000 has declined 2.8% for 3 consecutive weeks, enough to see it touch its 200 week moving average.

The DAX fallen for 3 straight weeks, while Copenhagen and Switzerland’s SMI have done so for 4 weeks.

Oslo broke its 7 week winning streak after last week’s posting of an outside bearish reversal.

And South Africa broke its 4 weeks winning streak.

Commodities were mixed.

We saw strength in base metals, softs and coals, again.

Weakness was seen in Oils, Lumber, Cotton, Soybeans, Sugar and the PGM’s.

Biodiesel and Brent Crude Oil isn’t overbought this week.

Gold, Aluminium, Copper, Coffee, Tin and Silver all appear in the overbought quinella column this week.

Gold’s weekly winning streak is at 5 while Silver has risen for 7 of the past 8 weeks.

Coffee prices were amongst the largest gainers for the week, again. Robusta Coffee has risen 31% over the past 8 weeks.

Cotton has fallen for 6 straight weeks, while Lumber’s declining streak is at 4 week.

Gasoline broke its 5 week winning streak.

The LNG JKM price (in Yen) has risen 20% over the past fortnight.

Cocoa has been overbought for 26 weeks, while putting together a recent 9 week winning streak.

Cocoa remains more expensive than Copper.

Aluminium has risen for 8 straight weeks, rising 24% over that time.

And Lithium Hydroxide has now spent 40 consecutive weeks in weekly oversold territory, however it rose 8%.

Currencies are seeing continued action.

U.S. strength is keeping many reciprocals in oversold territory.

The AUD and the Yen were weaker.

The CAD was firmer as was the Euro.

And the BRL has fallen for 7 straight weeks against the USD.

The larger advancers over the past week comprised of;

Australian Coking Coal 5.7%, Aluminium 10%, Baltic Dry Index 11%, Cocoa 9.4%, China Coking Coal 4.2%, Lean Hogs 2.5%, Copper 5.6%, Coffee 5.2%, JKM LNG in Yen 7.5%, Tin 3.5%, Newcastle Coal 6%, Nickel 9.5%, Robusta Coffee 4.7%, Shanghai Iron Ore 2.1%, Silver in AUD 3.6%, Silver in USD 2.9%, Gold in AUD 2.8%, Gold in EUR 1.9%, Gold in GBP 2.7%, Gold in USD 2.1%, Oats 2%, Rice 7.5%, Shanghai Composite 1.5%, CSI 300 1.9%, KBW Bank Index 2%, Chian A50 3.4% and Pakistan’s KRE Index rose 1.7%.

The group of largest decliners from the week included;

WTI Crude Oil (3.4%), Cotton (4.5%), Heating Oil (5.4%), Lumber (5.9%), Lithium (3.4%), Orange Juice (3.2%), Palladium (3.1%), Platinum (5.8%), Gasoline (3.3%), Biodiesel (2%), Sugar (3.5%), S&P GSCI (1.4%), Brent Crude Oil (3.3%), Gasoil (7%), Soybeans (2%), All World Developed ex USA (2.3%), AEX (2.7%), Budapest (3.3%), DJ Transports (2.7%), HSCEI (2.3%), Hang Seng (3%), IDX (4.4%), S&P SmallCap 600 (1.2%), Russell 2000 (2.8%), Nasdaq Composite (5.5%), KOSPI (3.4%), FTSE 250 (1.7%), S&P MidCap 400 (2.2%), Nasdaq Biotech (3.1%), Nasdaq 100 (3.4%), Nikkei (6.2%), Nifty (1.7%), Oslo (2.5%), PSE (3.3%), J’burg 40 (2.7%), SET (4.6%), SOX (9.2%), Chile (2.9%), S&P 500 (3.1%), TAIEX (5.8%), FTSE 100 (1.3%), Vietnam (8%), ASX 200 (2.8%), ASX Materials (2.2%), ASX Industrials (2.9%) and the ASX Small Caps fell 3.9%

April 21, 2024

by Rob Zdravevski

rob@karriasset.com.au