Unloved coal

March 10, 2025 Leave a comment

Equity prices of Coal mining companies are troughing as last seen in 2020.

March 10, 2025

rob@karriasset.com.au

Trying to hear what's not being said

March 10, 2025 Leave a comment

Equity prices of Coal mining companies are troughing as last seen in 2020.

March 10, 2025

rob@karriasset.com.au

March 10, 2025 Leave a comment

The circle shows the last time ASX listed Wisetech (WTC.ASX) was oversold on a weekly basis.

March 10, 2025

March 9, 2025 Leave a comment

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

n.b. pricing of (commodity) futures contracts is only considering the immediate front month.

* denotes multiple week inclusion

Extremes above the Mean (at least 2.5 standard deviations)

Austrian, Swiss, Czech, German, Danish, Spanish, French, Greek, Italian, Dutch, Portuguese and Swedish 10 year government bond yields

German 5 year government bond yields

IEI

Copper/Gold Ratio

U.S. 30 year minus U.S. 10 year bond yield spread

Lumber

CHF/AUD

CHF/CAD

JPY/AUD *

JPY/CAD *

PHP/USD

SEK/USD

Vietnam’s equity index

Overbought (RSI > 70)

Japanese 2 & 5 year government bond yields *

Arabica Coffee

Gold in AUD, CAD and ZAR *

Hungary’s BUX Index *

Germany’s DAX Index *

Italy’s MIB Index

Spain’s IBEX Index *

Pakistan’s KSE Index

Czech Republic’s PX Index *

Switzerland’s SMI Index *

Chile’s IPSA and IGPA Indices *

And Singapore’s Strait Times

The Overbought Quinella (Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Japanese 10 year government bond yield

Austria’s ATX *

HSCEI Index *

Hang Seng Index *

Extremes below the Mean (at least 2.5 standard deviations)

TBX *

U.S. 2 year and 5 year government bond yields

Australian 3 year and 5 year government bond yields

Canadian and Finnish 10 year government bond yields

U.S. 5 year government bond yield minus U.S. inflation rate

U.S. 5 year government bond yield minus U.S. 5 year breakeven inflation rate

U.S. 10 year government bond yield minus U.S. 10 year inflation rate

Cotton

Lean Hogs

JKM LNG priced in Yen

AUD/EUR

AUD/GBP

AUD/JPY

CAD/CHF

S&P SmallCaps 600 Index

Russell 2000

Nasdaq Composite

S&P MidCap 400

Nasdaq 100

Philadelphia SOX Index *

S&P 500

And the Nasdaq Transportation Index

Oversold (RSI < 30)

U.S. 3 month government bill yield *

Australian Coking Coal *

North European Hot Rolled Coil Steel *

Lithium Carbonate *

Lithium Hydroxide *

Newcastle Coal *

Orange Juice *

Uranium *

And Thailand’s SET Index *

The Oversold Quinella (Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

U.S. 10 year government bond yield minus German 10 year bond yield spread

Jakarta Composite Index

Notes & Ideas:

Government bond yields rose.

except for Belgian and Brazil’s bond yields.

Brazilian 10’s aren’t overbought anymore

U.S. 7’s & 10’s broke their 7 week falling streak.

The U.S. 10 year and 5 year real interest rate remains in extreme territory.

Swiss yields rose further following last weeks bullish reversal.

Equities were mixed.

Asian markets were stronger as was Germany and Central Europe.

A bunch of European and Asian indices appear in the overbought category.

U.S. indices were amongst the weakest and dragged many others lower.

This week sees a range of American indices at oversold extremes.

The notable winners and losers for the week are listed at the end of this note.

Italy’s MIB broke its 5 week winning streak.

Germany’s DAX Index is overbought for 6 weeks.

Thailand’s SET has fallen for 6 consecutive weeks.

Vietnam’s main index has risen for 7 weeks.

Spain’s IBEX broke its 10 straight weeks of advance.

The S&P SmallCap 600, MidCap 400 and Russell 2000 have declined for 6 consecutive weeks.

The Hang Seng and the HSCEI were registering overbought quinella prices.

And Switzerland’s SMI has climbed for the past 4 weeks and 10 of the past 11 weeks.

Commodity prices were better than the past couple weeks.

Crude Oil and related products, Cocoa, Urea and Lithium were amongst the losers. i

Coffee, Cattle, Coal, Natural Gas, Nickel, Palladium and Silver were the notable advancers for the week.

The Baltic Dry Index has soared 63% over the past 3 weeks.

Cocoa has fallen for 5 of the past 6 weeks.

Gasoline and Rubber are in 4 week losing streaks.

Urea and Richards Bay Coal isn’t overbought anymore

Orange Juice declines further, extends its losing streak to 11 weeks

U.S. Hot Rolled Coil Steel has climbed for 6 weeks.

Platinum broke its 4 week losing streak.

Cattle rallied 5% and broke its 5 week losing streak.

Brent Crude and WTI Crude have fallen for 7 straight weeks.

Tin prices have soared 16% over the past 5 weeks.

while Lithium Hydroxide has now lingered in weekly oversold territory for 92 consecutive weeks.

Currencies saw much action.

The DXY (USD) Index fell 3.4%.

The Aussie was weaker with a host of pairs at extremes.

The Aussie has fallen for 4 weeks against the British Pound.

The Canadian Dollar was weaker.

The Loonie and the Swiss appear in this weeks list,

As does the Yen.

Risk has been off and we’ve been buying Yen and Swissie.

The larger advancers over the past week comprised of;

Richards Bay Coal 1.7%, Aluminium 3.9%, Rotterdam Coal 4.3%, Bloomberg Commodity Index 2%, Baltic Dry Index 13.9%, Lean Hogs 4.4%, Copper 3.6%, Coffee 3%, Cattle 4%, Tin 4.1%, Newcastle Coal 6%, Natural Gas 14.7%, Nickel 6.7%, Palladium 4.8%, Platinum 3.1%, Silver in AUD 2.8%, Silver in USD 4.4%, Gold in USD 1.8%, Shanghai Composite 1.6%, All Developed World ex USA 2.5%, PSE 3.7%, PX 2.9%, SA40 3.4%, Vietnam 1.6%, WIG 1.8%, BIST 8.8% and Jakarta Composite rose 5.8%.

The group of largest decliners from the week included;

Australian Coking Coal (1.9%), Brent Crude (3.7%), Cocoa (9.1%), WTI Crude Oil (3.9%), Heating Oil (4.3%), JKM LNG in Yen (14.3%), Lithium Carbonate (4.7%), Lithium Hydroxide (1.7%), Gasoline (5.1%), Dutch TTF Gas (9.8%), Urea U.S. Gulf (3%), Gasoil (2.8%), Uranium (1.6%), Gold in EUR (2.5%), KBW Banking Index (8.8%), DJ Industrials (2.3%), DJ Transports (2.4%), S&P SmallCap 600 (3.6%), Russell 2000 (4.1%), TAIEX (2.1%), Nasdaq Composite (3.5%), KLSE (7.1%), KRE Regional Banks (7.1%), S&P MidCap 400 (3.5%), Nasdaq 100 (3.3%), Copenhagen (2.1%), SOX (2.9%), S&P 500 (3.1%), Nasdaq Transports (3.1%), TSX (2.5%), FTSE 100 (1.5%), ASX Financials (4.6%), ASX 200 (2.7%), ASX Industrials (1.8%) and the ASX Small Caps fell 2.6%.

March 9, 2025

By Rob Zdravevski

rob@karriasset.com.au

March 5, 2025 Leave a comment

Do you remember the deafening hubbub in November 2024 when “everyone” was scrambling to buy data centres stocks?

The study below highlights 4 empirically aligned moments when the stock price of Digital Realty (DLR US) was trading at extremes that deserved some attention and analysis.

You’ll find similar moments of extremes in many of the world’s other data centre ‘plays’ around that time.

In good news, DLR’s stock price is now trading at the price it was 5 years ago.

Sadly, this analysis would’ve been handy for those who were subscribing to #datacentre IPO’s which were being touted around the November and December 2024 period.

March 5, 2025

rob@karriasset.com.au

March 5, 2025 Leave a comment

The #Gold Bugs won’t like this view.

“When Gold registers a monthly overbought signal and is trading at > 40% above its 50 month moving average, the price consolidates and is followed by a concerted effort at mean convergence”

It’s a little different initiating a new ‘long’ at todays prices compared to being ‘long’, long ago.

Reports suggesting a ‘melt-up’ have validity because of momentum, but one should forfeit the right to complain if gravity takes hold.

March 5, 2025

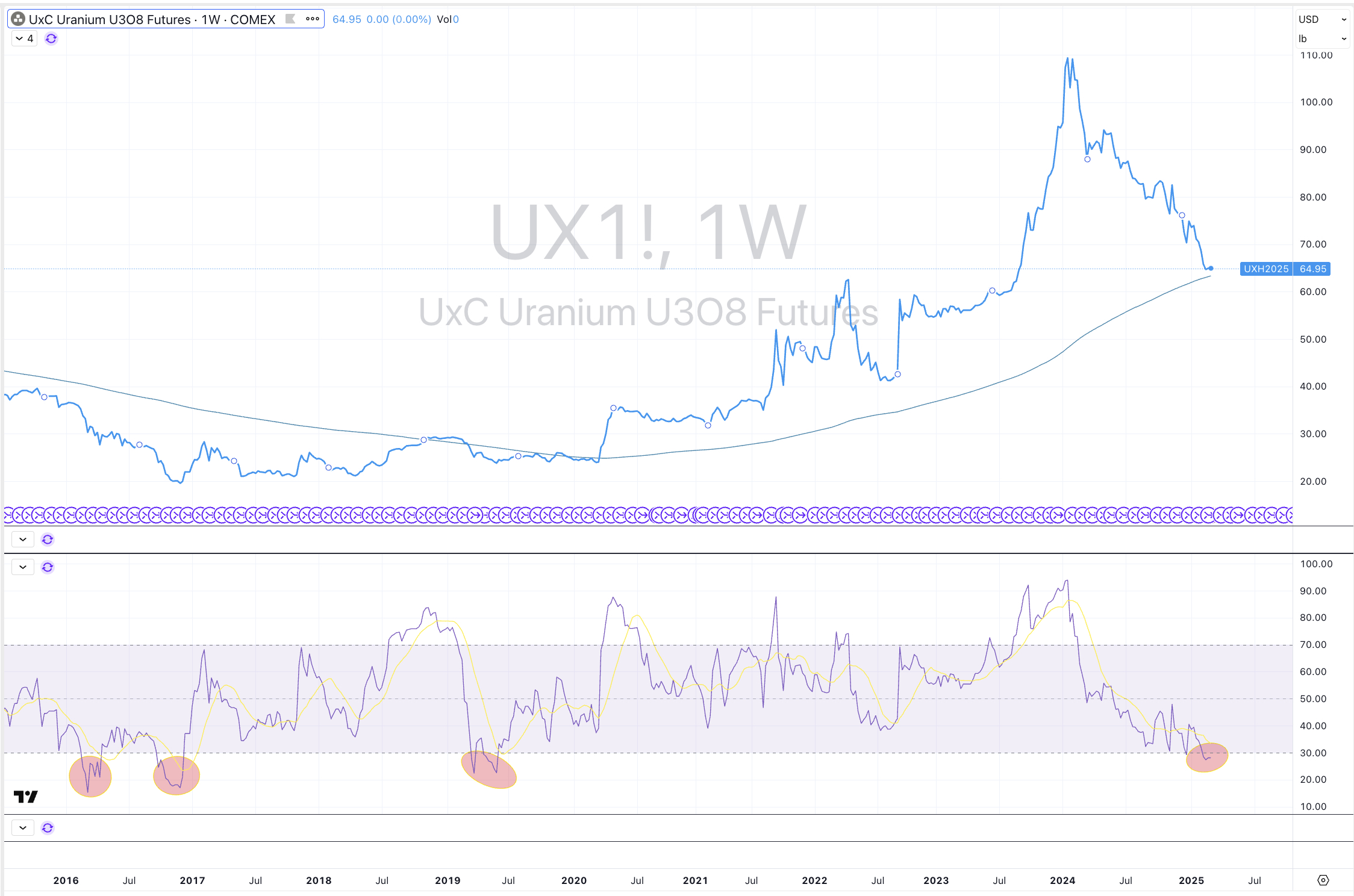

March 4, 2025 Leave a comment

The uranium futures price appeared in the oversold section in my weekend edition of Macro Extremes.

It’s the 4th such time that uranium is doing so over the past 10 years.

March 4, 2025

rob@karriasset.com.au

March 2, 2025 Leave a comment

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

n.b. pricing of (commodity) futures contracts is only considering the immediate front month.

* denotes multiple week inclusion

Extremes above the Mean (at least 2.5 standard deviations)

Swiss 10 year government bond yields *

JPY/AUD

JPY/CAD

HSCEI Index *

Hang Seng *

Tin

Overbought (RSI > 70)

Japanese 2, 5 & 10 year government bond yields *

Brazilian 10 year government bond yield *

Urea (U.S. Gulf price) *

Gold in AUD, CAD and ZAR *

Hungary’s BUX Index *

Germany’s DAX Index

Czech Republic’s PX Index *

Switzerland’s SMI Index

And Chile’s IPSA and IGPA Indices *

The Overbought Quinella (Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Austria’s ATX *

Spain’s IBEX Index *

Extremes below the Mean (at least 2.5 standard deviations)

TBX

U.S. 5 year government bond yield minus U.S. 5 year breakeven inflation rate

U.S. 5 year government bond yield minus U.S. inflation rate

U.S. 10 year government bond yield minus U.S. 10 year breakeven inflation rate

U.S. 5 year government bond yield minus U.S. 10 year inflation rate

Philadelphia SOX Index

Nikkei 225 Index

Oversold (RSI < 30)

U.S. 3 month government bill yield *

INR/USD

Australian Coking Coal *

Richards Bay Coal *

North European Hot Rolled Coil Steel *

Lithium Carbonate *

Lithium Hydroxide *

Newcastle Coal *

Uranium *

And Thailand’s SET Index *

The Oversold Quinella (Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

Orange Juice *

Jakarta Composite Index

Notes & Ideas:

Government bond yields fell….

except for Belgian, Finland and Brazil’s bond yields.

U.S. 7’s & 10’s have fallen for 7 weeks.

As a result, the IEF bond ETF has risen for 7 weeks.

The U.S. 10 year and 5 year real interest rate entered extreme territory this week.

We saw a large fall and reversal in Swiss yields.

While the Japanese 10 year bond yield has climbed for 8 weeks.

Equities were notably weaker.

Italy’s MIB have risen for 5 consecutive weeks.

Vietnam’s main index has risen for 6 weeks.

Spain’s IBEX have extended its advance to 10 weeks straight.

Inversely, the S&P SmallCap 600, MidCap 400 and Russell 2000 have declined for the 5 consecutive weeks.

The Hang Seng and the HSCEI were registering overbought quinella prices early in the week, before they fell and broke their 6 consecutive weeks of advance.

Singapore’s Strait Times, South Africa’s SA40 and Helsinki’s 25 Index snapped their respective 4, 5 and 6 week winning streaks.

While Hungary’s BUX, Poland’s WIG broke their 9 week wining streaks.

The SENSEX and NIFTY are nearing extremes.

And Switzerland’s SMI has climbed for 9 of the past 10 weeks.

Commodity prices had a terrible week, across the board.

Tin, Corn, Wheat, Coffee, Sugar and Palladium were amongst the heaviest decliners.

Shipping Rates, Lumber, Oasis were the few to rise for the week.

In fact, the Baltic Dry Index has soared 57% over the past 4 weeks, after registering an oversold reading.

Orange Juice tanks further, extends its losing streak to 10 weeks

U.S. Hot Rolled Coil Steel has climbed for 5 weeks.

Sugar broke its 5 week winning streak, erasing the past 3 weeks of gains.

Platinum has fallen for 4 straight weeks.

Silver in USD broke its 5 straight weeks of advance.

Gold in USD snapped its 8 week winning streak.

Australian Coking Coal prices rose slightly, snapping its 7 straight weeks of losses.

Cattle is in a 5 week losing streak, while Uranium snapped its 4 weeks of decline.

Brent Crude and WTI Crude have fallen for 6 straight weeks.

Lean Hogs broke their 4 consecutive weeks of advance,

Wheat slumped and broke its 6 week winning streak.

Tin prices have soared 12% over the past weeks.

while Lithium Hydroxide has now lingered in weekly oversold territory for 91 consecutive weeks.

Currencies also saw much action.

The Yen and Swiss rose, confirming the ‘risk-off’ type of week.

The Aussie fell and did the Loonie.

In turn, we see the Yen in overbought territory this week against these ‘risk’ currencies.

The British Pound rose

And the U.S. Dollar rose against everyone.

The larger advancers over the past week comprised of;

Baltic Dry Index 25.3%, Lumber 2%, JKM LNG in Yen 2.9%, Urea, U.S. Gulf price 1.7%, Oats 1.5%, ATX 2.5% and IBEX rose 3.1%.

The group of largest decliners from the week included;

Aluminium (3.4%), Bloomberg Commodity Index (3.8%), Cotton (3.1%), Lean Hogs (4.6%), Heating Oil (2.7%), JKM LNG (2.3%), Arabica Coffee 4.2%, Lithium Hydroxide (1.9%), Tin (7.3%), Newcastle Coal (4.1%), Natural Gas (8.5%), Orange Juice (2.7%), Palladium (9.2%), Platinum (5%), Robusta Coffee (6.6%), Sugar (9.7%), Sugar #16 (4.5%), S&P GSCI (2.8%), CRB Index (3%), Dutch TTF Gas (6.5%), Brent Crude (1.6%), Gasoil (3.7%), Urea Middle East (4.2%), Silver in AUD (1.8%), Silver in USD (4%), Gold in USD (2.7%), Gold in GBP (2.2%), Gold in EUR (1.9%), Gold in CHF (2.1%), Corn (7.5%), Rice (1.6%), Soybeans (3%), Wheat (8%), Shanghai Composite (1.7%), AEX (1.7%), China A50 (1.6%), SOX (7.2%), HSECI (2.9%), Hang Seng (2.3%), BOVESPA (3.4%), Jakarta Composite (7.8%), Russell 2000 (1.5%0, TAIEX (2.9%), Nasdaq Composite (3.5%), KOSPI (4.6%), Mexico (2.6%), Nasdaq Biotech (1.6%), Nasdaq 100 (3.4%), Nikkei 225 (4.2%), NIFTY (2.9%), SA40 (3.5%), SENSEX (2.8%), SET (3.4%), TA35 (1.8%), FTSE 100 (1.7%), ASX 200 (1.5%), ASX Materials (5.3%) and the ASX SmallCaps fell 2.5%.

March 2, 2025

By Rob Zdravevski

rob@karriasset.com.au

February 28, 2025 Leave a comment

The circled area is when my analysis suggested extremes in Alphabet’s price and valuations.

This was when I was advising clients to sell their positions.

“We” have not held the stock for nearly a year.

The ‘fat part of the trade’ was had.

Even though today’s price is the same as that of April 2024……

I am not buying it back, yet.

February 28, 2025

rob@karriasset.com.au

February 27, 2025 Leave a comment

WTI Crude Oil is in a 6 week losing streak and it’s just commencing a medium term down trend.

It needs to hold $64.75, otherwise I’ll look for a visit to $62.

February 27, 2025

rob@karriasset.com.au