Selling Euro strength

April 24, 2025 Leave a comment

Enough for the Euro, for now.

Here are the 5 moments over the past 10 years when the Euro has traded at particular extremes against the U.S. Dollar.

April 24, 2025

rob@karriasset.com.au

Trying to hear what's not being said

April 24, 2025 Leave a comment

Enough for the Euro, for now.

Here are the 5 moments over the past 10 years when the Euro has traded at particular extremes against the U.S. Dollar.

April 24, 2025

rob@karriasset.com.au

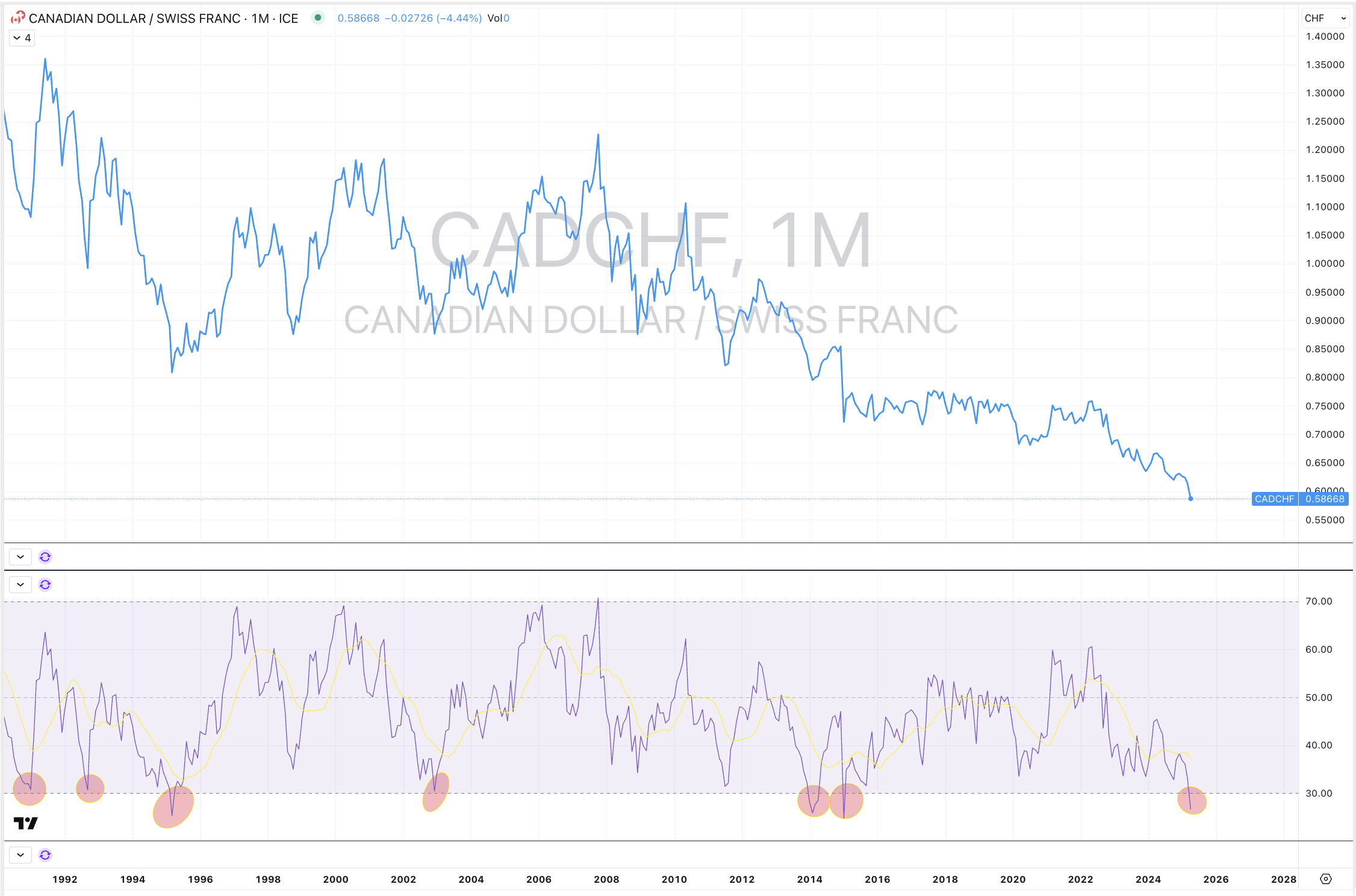

April 21, 2025 Leave a comment

Here are the 7 times over the past 35 years which the Canadian Dollar has been oversold against the Swiss Franc, on a Monthly basis.

April 21, 2025

rob@karriasset.com.au

April 21, 2025 Leave a comment

A year ago, I wrote about my interest in re-entering the uranium trade.

“I’ll look to add to uranium price “trackers” such as the #Sprott Physical Uranium Trust at C$20.50 and Yellow Cake plc at 450p”

The circle in the attached chart shows the price of date of the Sprott Physical Uranium Trust on that April 10, 2024 call.

Both securities have now reached those levels but I am yet to pull the trigger on any buying.

April 21, 2025

rob@karriasset.com.au

April 20, 2025 Leave a comment

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

n.b. pricing of (commodity) futures contracts is only considering the immediate front month.

* denotes multiple week inclusion

Extremes above the Mean (at least 2.5 standard deviations)

AUD/IDR

AUD/ZAR *

CAD/USD *

EUR/GBP

NZD.AUD

NZD/USD

PHP/USD

THB/USD

Overbought (RSI > 70)

Australian government 10 year bond yield minus the Aust. 5 year bond yield spread *

U.S. 10 year minus U.S. 2 year bond yield spread *

BofA BB High Yield Option Adjusted Spread *

Urea (U.S. Gulf) *

Gold in AUD, CAD, EUR, GBP, USD and ZAR *

Chile’s IGPA and IPSA equity indices

The Overbought Quinella (Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Australian government 10 year bond yield minus the Aust. 2 year bond yield spread

U.S. 30 year minus U.S. 10 year bond yield spread *

EUR/USD *

Extremes below the Mean (at least 2.5 standard deviations)

Australian 2, 3, 5 & 10 year bond yields *

German and Italian 2 year bond yields *

Australian 3 and 5 year bond yields

Polish 10 year bond yields *

Copper/Gold Ratio *

USD/CAD

USD/MXN

Oversold (RSI < 30)

Richards Bay Coal *

U.S. (DXY) Dollar Index

North European Hot Rolled Coil Steel

Lithium Carbonate *

Lithium Hydroxide *

Newcastle Coal *

Shanghai Rebar

Rubber

AUD/EUR

RMB

USD/DKK

USD/SEK

Dow Jones Transports

S&P SmallCap 600

Taiwan’s TAIEX

Nasdaq Transports

IBB Biotech ETF

And Thailand’s SET Index *

The Oversold Quinella (Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

Australian 2 year government bond yield

Indian 10 year government bond yield *

CAD/CHF

AUD/CHF

USD/CHF

Notes & Ideas:

Government bond yields fell except for those in Japan.

The non-investment grade bond yields aren’t overbought anymore.

Norwegian 10 year yields are in a 5 week declining streak.

Notably, Australian 2, 3 and 5 year yields are oversold.

European 10’s have fallen for 5 straight weeks while Euro 2’s have done so for 6 weeks.

Equities rose, again.

Equities had a good week, except for the American indices.

All of the equity indices which were in last weeks oversold list, are not there anymore.

For now, it looks like April 4th/7th may signal the lows for global equities.

The DAX, Hang Seng, Stockholm and Helsinki broke their 5 weeks falling streak

Copenhagen broke its 6 week losing streak.

The IBB Biotech ETF broke its 7 weeks of decline.

Commodities were mainly higher.

The Bloomberg Commodity Index has risen 3% over the past fortnight.

Many commodities which were oversold last week are no longer so, including uranium.

Cocoa, Coal, Natural Gas, Palm Oil & Tin were counted amongst the few losers.

The Baltic Dry Index has fallen for 5 straight weeks.

Sugar has declined for 4 weeks straight.

Gold as priced in ZAR has risen for 6 weeks.

Gold in AUD is in a 7 week winning streak.

while Lithium Hydroxide has been oversold territory for 98 consecutive weeks.

Currencies were very active, again.

The Aussie rose.

The Loonie was weaker against all except the USD.

The British Pound was stronger as was the Kiwi.

The Yen was mixed as the USD/JPY is approaching oversold levels.

The U.S. Dollar (DXY) Index has fallen for 5 consecutive weeks.

Notably, the Swissie is at oversold extremes against some risk currencies.

The larger advancers over the past week comprised of;

Bloomberg Commodity Index 1.4%, Brent Crude 4.6%, WTI Crude 5.2%, Lean Hogs 5%, Copper 4.8%, Heating Oil 4.1%, JKM LNG 4.9%, Arabica Coffee 5.4%, Cattle 3.7%, JKM LNG in Yen 7.3%, Nickel 3.6%, Orange Juice 8.9%, Palladium 6%, Platinum 3.4%, Gasoline 4.9%, S&P GSCI 2.6%, CRB Index 2.1%, Dutch TTF Gas 6.6%, Gasoil 6.2%, Gold in CAD 2.7%, Gold in CHF 3.3%, Gold in EUR 2.7%, Gold in USD 2.8%, Oats 3.1%, All World Developed ex USA 4.1%, AEX 4%, ATX 5.4%, KBW Bank Index 1.9%, BUX 2.5%, CAC 2.6%, DAX 4.1%, FTSE 100 5.7%, Hang Seng 2.3%, IBEX 5.1%, Bovespa 1.5%, IDX 2.9%, KLSE 3.1%, KRE Regional Banks 4.4%, KSE 2.1%, KOSPI 2.1%, FTSE 250 4%, Mexico 3%, Nasdaq Biotechs 1.5%, Nikkei 225 3.4%, NIFTY 4.5%, Oslo 2.8%, Copenhagen 4%, Helsinki 3.7%, PX 3.2%, Russell 2000 1.6%, South Africa40 4%, SENSEX 4.5%, SET 2%, SMI 3.8%, IGPA 4.8%, IPSA 5.2%, STI 5.9%, TA35 3%, TSX 2.6%, FTSE 100 3.9%, WIG 4.4%, ASX Financials 3.2%, ASX 200 2.3%, ASX Materials 3.2%, ASX SmallCaps 2.3% and the XBI Biotech ETF rose 2.2%.

The group of largest decliners from the week included;

Cocoa (1.7%), Newcastle Coal (2%), Natural Gas (8%), Palm Oil (4.2%), Tin (2.1%), Corn (1.6%), Wheat (1.3%), Dow Jones Industrials (2.6%), Nasdaq Composite (2.6%), Nasdaq 100 (2.3%), SOX (4%) and the S&P 500 fell 1.5%.

April 20, 2025

By Rob Zdravevski

rob@karriasset.com.au

April 17, 2025 Leave a comment

I’ve been telling clients that I still expect lower prices in the S&P 500, Nasdaq Composite and Nasdaq 100…..

because the Mega-8 should test some longer term mean reversion…

and those stocks still are making up 29% of the S&P 500’s total market capitalisation……

and so, a decline in the ‘headline’ indices will make many gasp but there is a nuance behind.

See Figure 13 in the link below;

April 17, 2025

rob@karriasset.com.au

April 15, 2025 Leave a comment

One year ago today, I disagreed when the former CEO of #Shell suggested the #SHEL stock price was undervalued.

My timing seems to be off by 6 months, but I still think that the price of Shell will trade down to GBP 21.70 area ‘soon’.

It could coincide with #Brent Crude trading down to $58.

April 15, 2025

rob@karriasset.com.au

April 13, 2025 Leave a comment

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

n.b. pricing of (commodity) futures contracts is only considering the immediate front month.

* denotes multiple week inclusion

Extremes above the Mean (at least 2.5 standard deviations)

British 30 year government bond yield

Turkish 10 year government bond yield

U.S. 3 month bill yield

U.S. 10 year bond yield minus the U.S. inflation rate

SHY

AUD/ZAR

CAD/USD

JPY/USD

SEK/USD

USD/ZAR

Overbought (RSI > 70)

U.S. 30 year minus U.S. 10 year bond yield spread *

BofA BB High Yield Option Adjusted Spread

Urea (U.S. Gulf)

Gold in AUD, CAD, GBP and USD

The Overbought Quinella (Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Australian government 10 year bond yield minus the Aust. 2 year bond yield spread

Australian government 10 year bond yield minus the Aust. 5 year bond yield spread

BofA High Yield Index Effective Yield

U.S. 10 year minus U.S. 2 year bond yield spread

U.S. 10 year minus U.S. 5 year bond yield spread

Gold in ZAR *

CHF/AUD

CHF/USD

EUR/GBP

EUR/USD

USD/IDR

Extremes below the Mean (at least 2.5 standard deviations)

Australian 2, 3, 5 & 10 year bond yields *

German and Italian 2 year bond yields *

British 2’s, 3’s & 5’s

Polish 10 year bond yields

Copper/Gold Ratio

Aluminium *

Brent and WTI Crude Oil *

Cotton *

JKM LNG in Yen

Nickel

Platinum

Gasoline

Shanghai Rebar

S&P GSCI

TSI China Iron Ore price

Gasoil

AUD/CAD

AUD/JPY

AUD/SGD

AUD/THB

CAD/CHF

GBP/JPY

Shanghai Composite

CSI 300

All World Developed – ex USA

Amsterdam’s AEX

KBW Bank Index

CAC

Indonesia’s IDX

KRE Regional Banks Index

KOSPI

Nikkei 225

Oslo

Helsinki

SENSEX

SMI

S&P 500

Strait Times

TSX

FTSE 100

ASX 200

ASX Materials

And ASX Small Caps

Oversold (RSI < 30)

Richards Bay Coal *

Lithium Carbonate *

Lithium Hydroxide *

Newcastle Coal *

Uranium *

Dow Jones Transports

And Thailand’s SET Index *

The Oversold Quinella (Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

Indian 10 year government bond yield *

U.S. (DXY) Dollar Index

North European Hot Rolled Coil Steel

Rubber

AUD/EUR

CAD/CHF

USD/DKK

Nasdaq Transports

Biotech ETF’s

S&P Small Cap 600

Russell 2000

Malaysia’s KLSE

FTSE 250

Copenhagen

Stockholm

Notes & Ideas:

Government bond yields mostly rose.

Intra-week we saw many extremes visited, not many closed near.

Thus, various yield spreads left the list.

European 10’s have fallen for 4 straight weeks while Euro 2’s have done so for 5 weeks.

U.S. 3 month bill yields moved out of oversold territory for the first time in 9 months.

Austrian and Spanish 10’s broke their 4 week losing streak,

And the U.S. 30 year minus U.S. 10 year yield spread broke it 8 consecutive weeks of gains.

Equities broadly rebounded.

It was a tricky week to report on extremes based on figures at the close of the week, for many extremes were seen intra-week before reversing.

The S&P 500 and the Nasdaq Composite rose and departed oversold land.

Chinese and Hong Kong stocks wore the losses this week as did some Western European indices.

The TAIEX and Singapore’s Strait Times Index both fell 8%, which is quite a comparison to the Nasdaq Composite’s 7% gain.

The DAX, Hang Seng, Stockholm and Helsinki have fallen for 5 weeks straight.

Copenhagen is in a 6 week losing streak.

The IBB Biotech ETF have fallen for 7 weeks.

DJ Transports, the FTSE 250 and the SOX broke their 7 consecutive weeks of decline.

The KRE Regionals Banks Index is nearly oversold.

Commodities were mixed.

Coal, Aluminium, Copper, Nickel, Orange Juice, Precious Metals and Grains rose.

Shipping Rates, Oil, Gases, Distillates, Tin and Sugar were amongst the largest losers.

Australian Coking Coal moved out of oversold territory as did Orange Juice.

The former has risen 5% over the past fortnight.

The Baltic Dry Index has fallen or 4 straight weeks while Aluminium broke its 4 week losing streak.

Coffee looks like turning lower.

Gold as priced in ZAR has risen for 5 weeks.

Gold in AUD is in a 6 week winning streak.

Tin tanked 13%, nearly erasing the past 5 weeks of gains.

while Lithium Hydroxide has been oversold territory for 97 consecutive weeks.

Currencies were very active, again.

The star of the show was the U.S. Dollar falling 3%.

Similar to equities, the end of week entrants in this list are only a fraction of the extremes seen intra-week.

The Aussie however rose towards the end of the week yet remains in the doldrums.

The Loonie was mixed and it has risen for 6 straight weeks against the USD.

The CHF/CAD is 16% below its 200 WMA.

The Swiss is strong.

The Kiwi is the highest against the AUD since March 2024.

And the Danish Krone is at a 3 year high vs the USD.

The larger advancers over the past week comprised of;

Australian Coking Coal 2.8%, Aluminium 4.1%, Rotterdam Coal 2.6%, Bloomberg Commodity Index 1.8%, Cotton 4%, Copper 2.8%, Nickel 2.2%, Orange Juice 23.1%, Platinum 3.3%, Silver in AUD 4.8%, Silver in USD 9.2%, Gold in AUD 2.3%, Gold in CAD 3.9%, Gold in GBP 5%, Gold in USD 6.6%, Gold in ZAR 6.8%, Corn 6.5%, Rice 3.2%, Soybean 6.7%, Wheat 5.1%, KBW Bank Index 4.1%, BUX 2.3%, China A50 2.2%, DJ Industrials 4.9%, DJ Transports 1.9%, Russell 2000 1.8%, Nasdaq Composite 7.3%, S&P MidCap 400 2.8%, Nasdaq 100 7.4%, SA40 6.1%, SOX 10.9%, S&P 500 5.7%, Nasdaq Transportations 2.8%, TSX 1.7%, WIG 2.3% and the ASX Small Caps rose 1.8%.

The group of largest decliners from the week included;

Baltic Dry Index (14.4%), Brent Crude (2.2%), DXY Index (3%), JKM LNG (2.9%), Arabica (2.9%), Lumber (3.1%), JKM LNG in Yen (14.8%), Lithium Carbonate (1.8%), Tin (19.8%), Natural Gas (8.1%), Gasoline (2.7%), Sugar (4.5%), Sugar #16 (7.1%), TSI Iron Ore (2.6%), Dutch TTF Gas (8.1%), Gasoil (2.9%), Shanghai Composite (3.1%), CSI 300 (2.9%), AEX (2.6%), CAC (2.3%), Egypt (2.8%), MIB (1.8%), HSCEI (7.4%), Hang Seng (8.5%), IDX (3.9%), TAEIX (8.3%), KLSE (3.3%), SMI (3.5%) and the Strait Times fell 8.2%.

April 13, 2025

By Rob Zdravevski

rob@karriasset.com.au

April 10, 2025 Leave a comment

A failed bond auction is the thing that undoes the prosperity in U.S. capital markets.

Earlier in the week, demand in the 3 year bond auction was weak or ‘tailed’.

It was thought that we’d see weak demand in todays 10 year auction, but an hour before the auction “old mate” makes an announcement which improves the chances of the auction’s success.

A failed bond auction is a proxy for no one wanting to buy America.

That would be embarrassing because that’s the exact product that Trump is trying to sell….

Later this week, it’s the 30 year bond auction.

April 10, 2025

rob@karriasset.com.au

April 9, 2025 Leave a comment

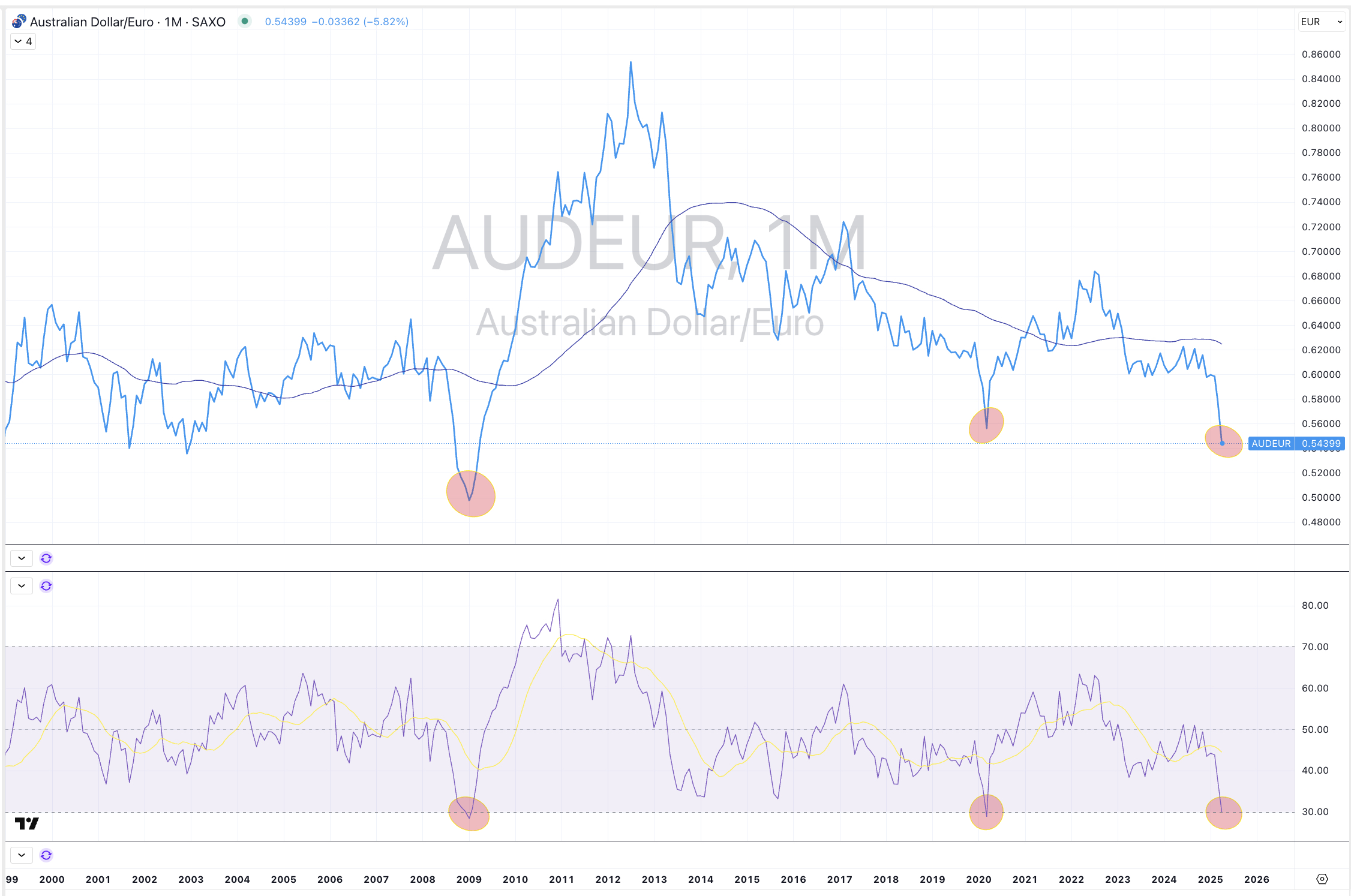

The Aussie Dollar is seeing it 3rd monumental low against the #Euro in the past 25 years.

Australia may see more European private equity firms buying up assets Down Under, especially when the #AUD is this cheap.

April 9, 2025

rob@karriasset.com.au

April 9, 2025 Leave a comment

Non-investment grade (BB rated) bond yields are stretched.

I think some moderation will occur and that tells me what to do with equities.

April 9, 2025

rob@karriasset.com.au