The following assets (on a weekly timeframe) registered an Overbought reading or traded more than 2.5 standard deviations above its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

Russia’s MOEX10 Index

Overbought (RSI > 70)

Canadian 10 year bond yields (for 9th consecutive weeks)

The Commodities Indices (the CRB and Bloomberg’s)

Iron Ore

Aluminium (for 8th consecutive weeks)

Copper (for 18th consecutive weeks)

Lean Hogs (for the 9th consecutive week and its highest price since September 2014)

Corn (for the 19th consecutive week & trading 52% above its 200 Week Moving Average)

Soybeans (for the 6th consecutive week)

S&P 500 Index (for the 2nd consecutive week)

Dow Jones Industrial Average (for the 2nd consecutive week)

S&P Mid Cap 400 (6th consecutive week)

U.S. KBW Banking Index (7th consecutive week)

Nasdaq Transportation Index (7th consecutive week)

Dow Jones Transport Index (6th consecutive week)

Sweden’s OMX 30 Index (6th consecutive week)

Germany’s DAX Index (2nd consecutive week)

France’s CAC-40

South Korea’s KOSPI Index

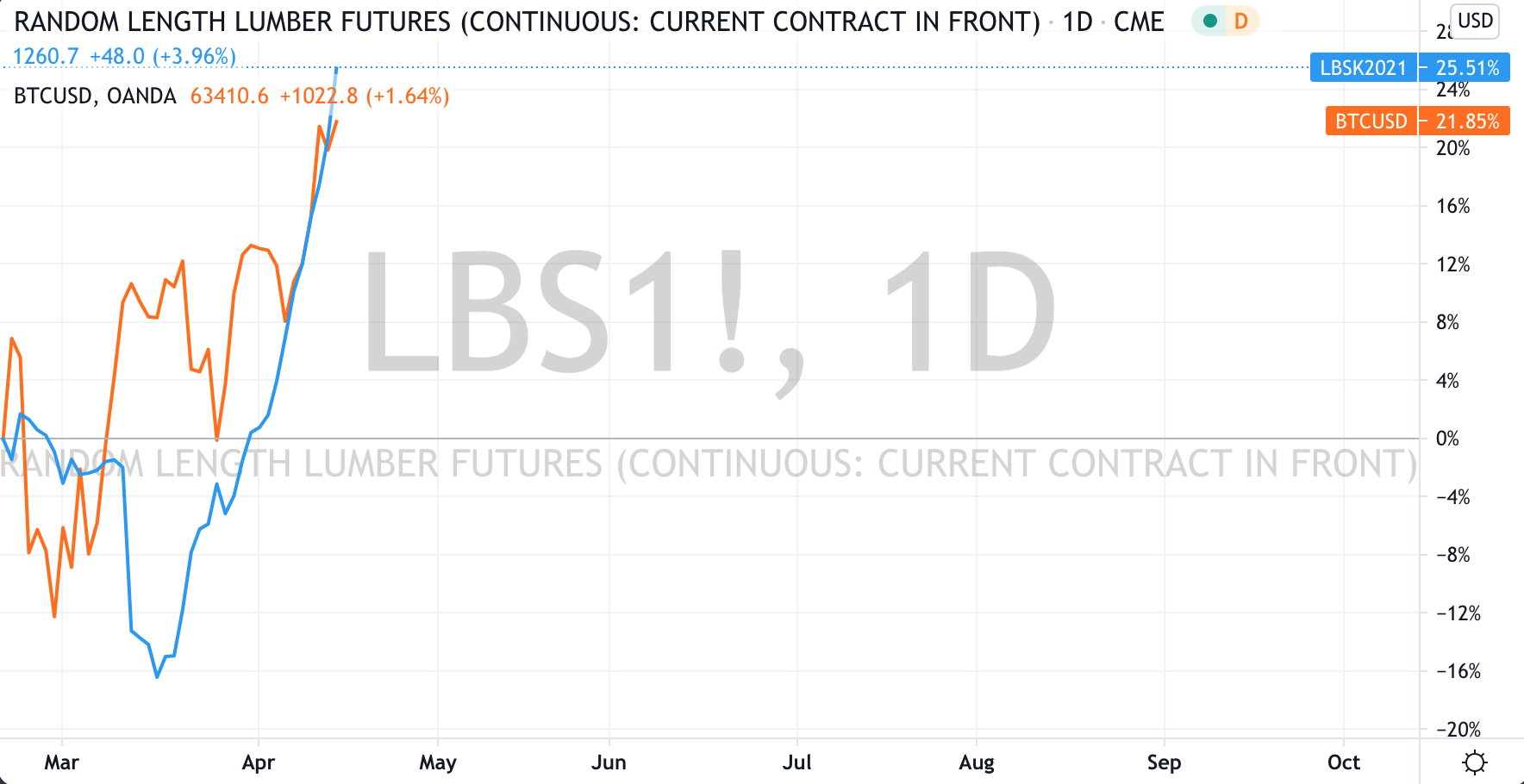

Bitcoin & Ethereum

The Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Australia’s ASX 200 Index

Lumber (having risen 26% in past 2 weeks)

Cryptocurrencies – Litecoin, Dogecoin, EOS and Ripple

Assets (securities) within my immediate universe which touched the other side of the extreme, being Oversold (where the RSI is < 30) or were at least 2.5 standard deviations below its mean are;

Extremes “below” the Mean (at least 2.5 standard deviations)

Nil

Oversold (RSI < 30)

Nil

Notes & Ideas:

Notably, no currencies are Overbought this week. Many of them have corrected from those high extremes from recent weeks and have since traded 2-3% lower.

The same can be said for the ‘highs’ seen in a host of global bond yields. Following from last week, bond buyers have been the more aggressive participants of the trade, sending most yields lower this past week.

My memory can’t help recite past moments where FX and Debt have pre-empted the next move for Equities.

The emerging group of assets visiting Overbought territory are the Equity Indices.

The most famous visitor is the S&P 500, while Australia’s ASX 200, Germany’s DAX and France’s CAC-40 are worth noting as well.

Overbought weekly streaks in U.S. Transports, U.S. Banking, U.S. MidCaps, along with Corn, Soybeans, Aluminium, Copper & Lean Hogs continue…….

Be cognisant that streaks do come to an end, let alone does mean reversion beckon.

Some commodities in the energy complex are nearing Overbought readings, although not yet…those being Gas Oil, Brent Crude, Heating Oil.

And, Bitcoin has rise 3.4% higher for the week and is trading at 442% above its 200 Weekly Moving Average.

April 17, 2021

by Rob Zdravevski

rob@karriasset.com.au