While WTI Crude Oil next support is around the $98.50 mark, I’m watching and queuing off the Gasoil (diesel) price as a timing mechanism to see if Crude holds its interim level.

Today, Australian listed uranium mining explorer and producer, Paladin announced a $200 capital raise which is equivalent to 10% of its market cap.

In March 2021, the company raised $192 million.

Nothing like raising enough capital to equal something close to 25% of your market capitalisation within a 12 month period.

So I kept my analysis about the merit of the latest capital raising simple.

At a market capitalisation of A$2.15 billion and trading at 78 cents, Paladin is the same market cap as when the stock was $2.50 in 2011…..due to share issuance.

and then I look at their resources and reserves

and then I compared it to the national producer of Kazakhstan….who is considered an industry leader

Kazataprom (supplies 40% of the world’s uranium for contract nuclear power generation)

Market Cap A$10.2 billion equiv.

Revenue A$680 million equiv.

EBITDA $285 million equiv.

Measured Mineral Resources of 700.9Mt grading 0.058%U and containing 406.6ktU,

Indicated Mineral Resources of 710.2Mt grading 0.052%U and containing 369.1ktU,

Inferred Mineral Resources of 13.6Mt grading 0.063%U and containing 8.6ktU.

Aggregated Mineral Resources of 1,424.7Mt grading 0.055%U

In this week’s meetings, I’ve been telling investors that I think the Fed may raise rates 2 or 3 times this year…….

some of the family offices that I spoke with were surprised that my prediction wasn’t near the consensus of 6, 7 or 8 hikes.

I said that I needn’t not conform with the herd, for that would make for a boring meeting and hardly add any value or debate.

The bit that made them laugh, was that I also think the Fed will cut rates once around the turn of 2023.

I think that the Fed will have gone too far in their hikes and with a hard landing imminent (lower GDP growth due to higher prices resulting in a buyers strike and higher financing costs), they may need to back peddle with a supplementary cut, which funnily may coincide with a mid-term election.

After all, the Democrats recently returned Mr Powell for a new term lasting until January 2028.

Continuing a thread that a truce is coming in Ukraine, the price of oil isn’t surging anymore and

Russian oil is flowing and being sold in the market, albeit at a discount. This is understandable, anything tainted can’t command the going spot price.

Calculations and beliefs that all of Russian production has been lost and left the global market is foolhardy.

Long Oil is a very crowded trade.

Is a truce is reached, a $25 drop in the oil price is plausible.

The following assets (on a weekly timeframe) registered an Overbought reading or traded more than 2.5 standard deviations above its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

Australian 3, 5 & 10 year government bond yields

New Zealand, Swedish, Turkish & Canadian 10 year government bond yields

Gold (in USD and AUD)

AUD/USD

Oslo equity index

TBT & TBX (U.S. listed “Short” bond ETF’s), confirming the inverse reading of the overbought U.S. bond yields listed in the next category.

Overbought (RSI > 70)

Australian and U.S. 2 year government bond yields

German 5 & 10 year government bond yields

Greek, Spanish, French, Italian, Portuguese & Korean 10 year government bond yields

Australian Coal

CRB Index

Bloomberg Commodity Index

Nickel

WTI Crude Oil

Brent Crude

Gasoline

Cotton

Corn

Soybeans

Uranium

AUD/GBP

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

U.S. 5 and 10 year government bond yields

Gasoil

Heating Oil

AUD/EUR

AUD/JPY

Assets (securities) which touched the other side of the extreme, being Oversold (where the RSI is < 30) or were at least 2.5 standard deviations below its mean are;

Extremes “below” the Mean (at least 2.5 standard deviations)

SGD/AUD

INR/AUD

Oversold (RSI < 30)

U.S. 10 year minus 2 year government bond yield spread (lowest since March 2020)

U.S. 10 year minus 5 year government bond yield spread (which has now inverting and at lowest since January 2007.

CSI 300 equity index

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

JPY/USD

Notes & Ideas:

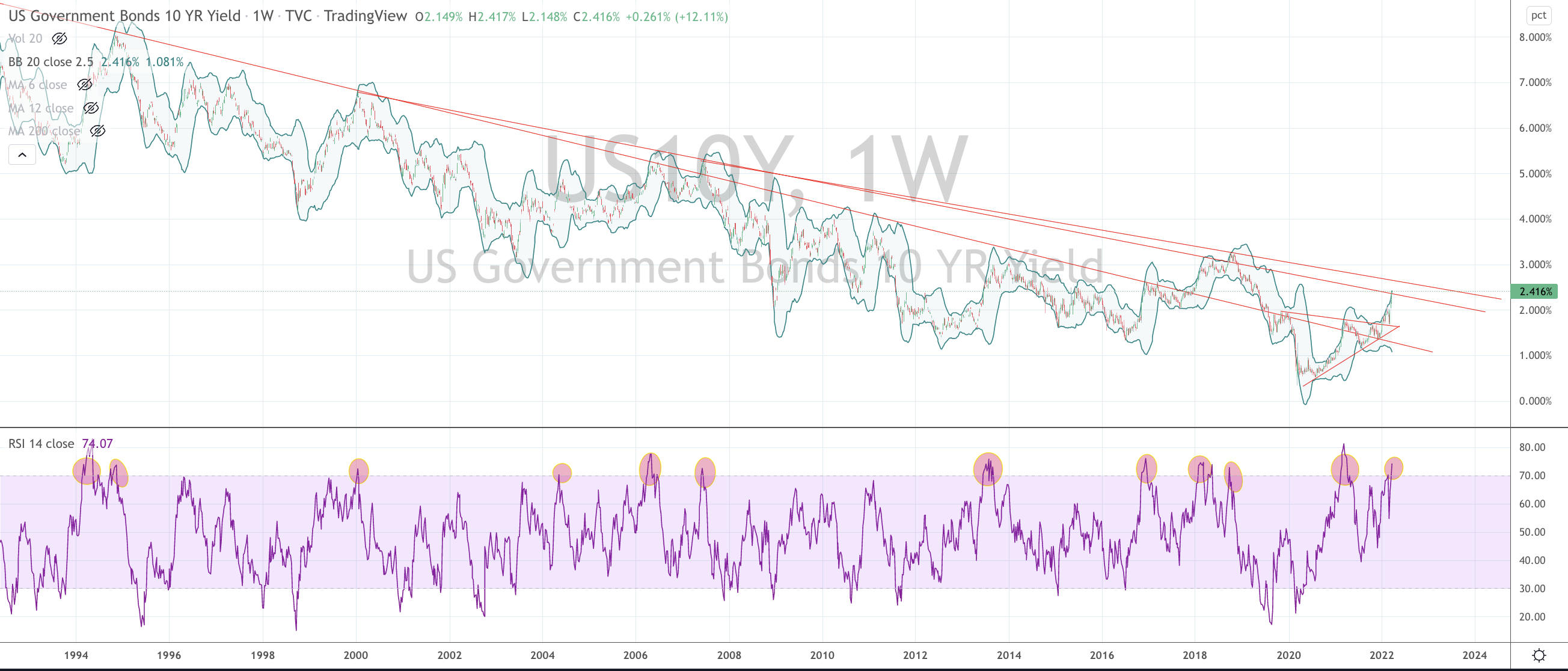

The big news in this week’s edition is the extreme high in the U.S. 10 year bond yield, which closed the week at 2.48%.

I’ll give it up to 2.66% but we’re at the upper end of the range for now.

The second largest piece of news, is that lack of news as we have seen the mildest and most benign moves in equity markets for many weeks. A host of indices barely changed week on week.

For example, the S&P 400 Midcap was up 0.3% on the week, while the Russell 2000 fell 0.4%.

Perhaps this is symbiotic of the VIX index which has fallen to 20 (see the chart below)

We also continued to see many ‘heady’ commodities ease from their recent overbought readings they work on testing support lines and ponder whether they change trend direction.

Keep in mind that creating a meaningful new trend takes more than a sudden jolt, instead it often requires prices to go through a consolidating and digestion process of the previous trend.

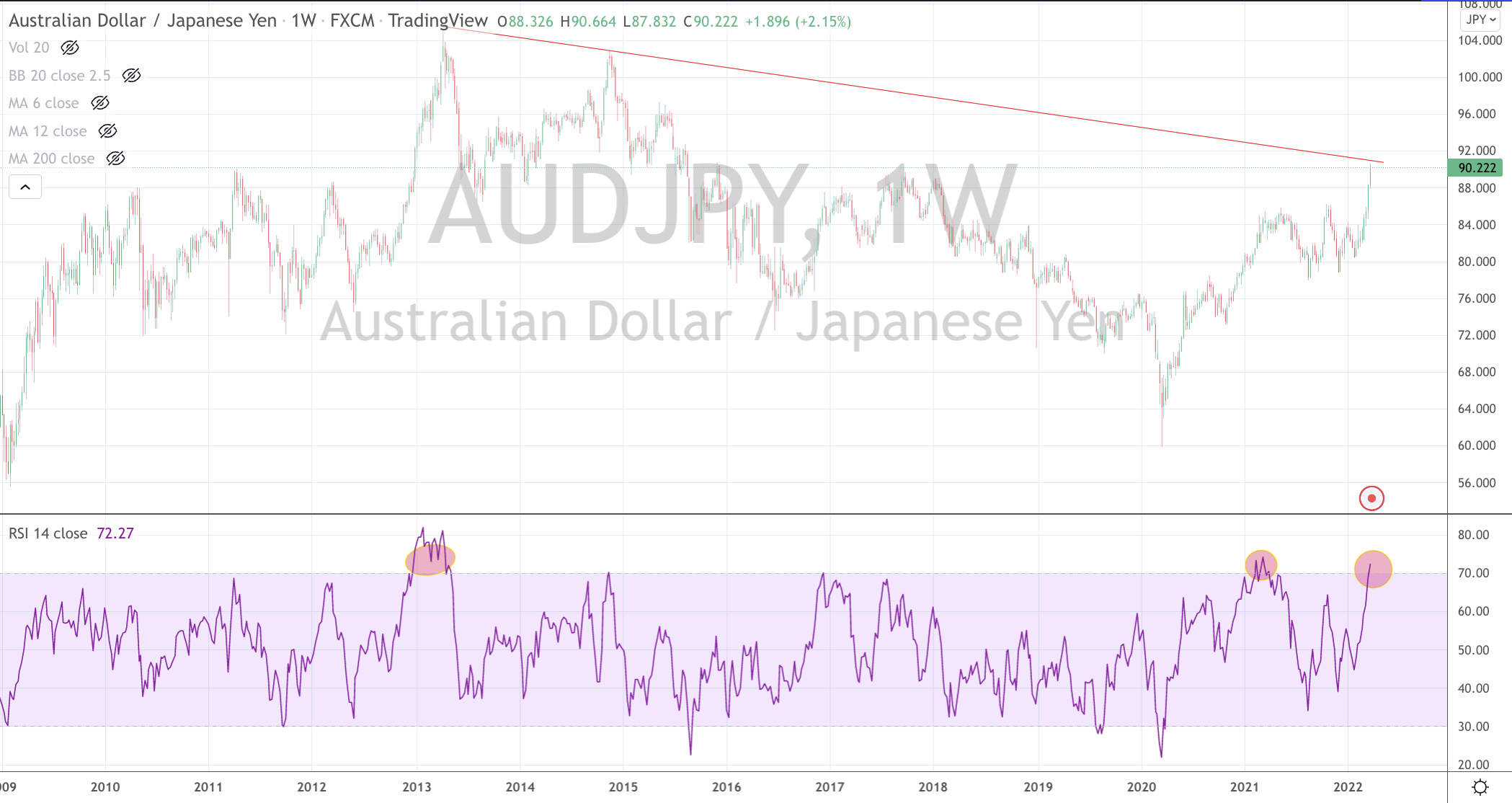

I’m seeing the AUD and USD at 6 year highs against the Japanese Yen;

The Shanghai equity index is nearing an oversold reading,

I think the S&P 500 may touch an interim top of 4,549.80

And last week, I mentioned Nasdaq’s bullish outside reversal week as it rose 2.3% this week.

The larger advancers over the past week comprised of;

Aluminium 6.9%, China Coal 11.4%, WTI Crude 10.5%, Gasoil 12.3%, Gold 1.9%, GVZ 12.2%, Hogs 8.1%, Heating Oil 14.4%, Natural Gas 14.6%, Nickel 9.2%, Orange Juice 2.2%, Gasoline 7.1%, Sugar 3.6%, Silver 2.1%, CRB 5.2%, Cotton 7.1%, Brent Crude 10.6%, Uranium 3.7%, Oats 6.2%, Rice 4%, Soybeans 2.5%, Wheat 3.6%, AUDJPY 3.9%, Bovespa 3.7%, Nasdaq 2.3%, Nikkei 4.9%, Oslo 2.7%, SOX 2.7%, S&P 500 1.8%, STI 2.5%, Istanbul 2% and the ASX 200 rose 1.5%.

The group of decliners included;

Baltic Dry Index (2.3%), Australian Coal (5.6%), Rotterdam Coal (-16% adding to last week’s 11% fall), JKM (3%), Lumber (15%), Palladium (4%), Platinum (2.7%), Dutch TTF Gas (3.6%), Copenhagen (4.5%), Helsinki (2.7%) and Stockholm (3.3%).

One of the more decisive currency moves over the past 2 years has been the 50% rise in the AUD versus the JPY.

Today, it’s recording its highest level since November 2015.

This often watched indicator of risk-on/risk-off sentiment has reached an overbought level seldom seen and when coupled with its butting up against a resistance line, makes me think the ‘fat part of the trade’ has been had.

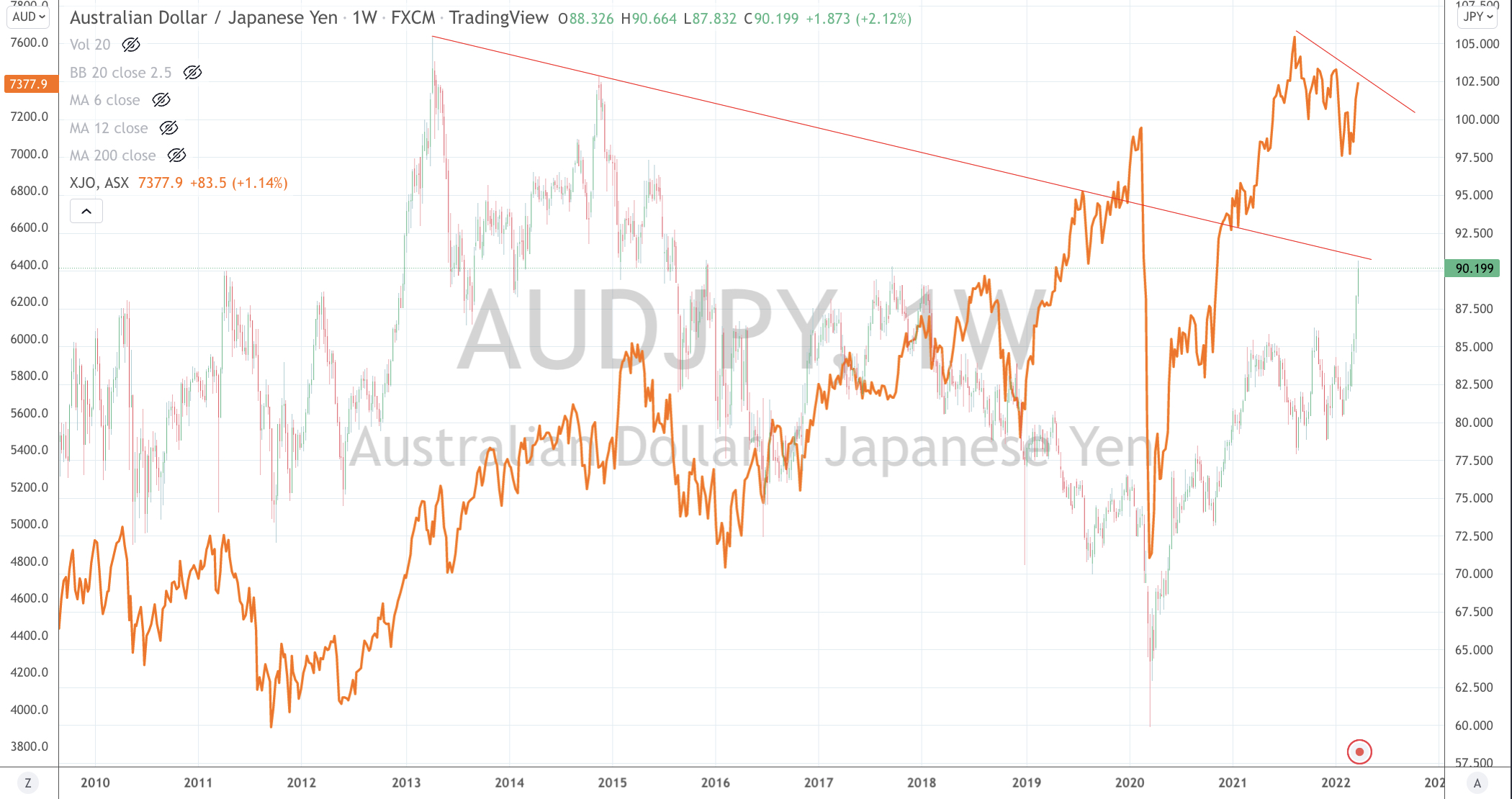

In the other chart below, I’ve overlaid the ASX 200 index and coincidentally it too is tickling a resistance line.

You see a nice companionship between the two.

So now, I’ll sell some AUD and buy JPY.

What to do then?

There are plenty of good Japanese businesses, not expensively valued and are conservatively operated which are carrying 20% of their market capitalisation in cash.

U.S. 10 year bond yield are at ‘overbought extremes’.

At 2.41%, it’s kinda done or at the least, at the upper end of being so.

I’ll give a move to 2.6% (that downward sloping resistance line in the chart below) but I’ll say that you don’t want to be shorting bonds at these levels.

Beyond the subjective notion that short bonds is a crowded trade and the chart below showing a unison registration of a 70 RSI reading (it’s 12th visit in 30 years) with a 2.5 weekly standard deviation above the mean, my other work tells me that the 10’s are the most stretched since October 2018.

In fact, other than 2018 and now, we haven’t seen the 10’s this ‘stretched’ at any other time in 40 years of data.

Additionally, the U.S. 10 year bond yields have doubled in 8 months and quadrupled in 18 months.

If you think 2.4% is low compared to where we once came from, the quantum of this ‘recent’ move should count for something.

p.s. once again, tune in to the noise amongst the market pundits, chat rooms and the media again. ‘Today’s’ hyper-ventilation is now about falling bond market yields.

Similar to recent moments seen in Nickel, Oil, Crypto, Wheat, Chinese equities etc etc, consider the opposite side of what the crowd is crowing about.

It’s funny, I just can’t seem to remember ‘them’ saying anything when interest rates were 1%……