Macro Extremes (week ending June 10, 2022)

June 12, 2022 Leave a comment

The following assets (on a weekly timeframe) registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

None

Overbought (RSI > 70)

Australian 2, 3, 5 & 10 year government bond yields

Canadian, Swiss, Spanish, French, Greek, Italian, South Korean, New Zealand, Swedish and Portuguese 10 year government bond yields

U.S. 2, 5 & 10 year government bond yields

German 2, 5 & 10 year government bond yields

TBT & TBX

U.S. Dollar (DXY) Index

CRB Index

Bloomberg Commodity Index

Natural Gas

Gasoline

WTI Crude Oil (September ’22 and December ’22 contracts)

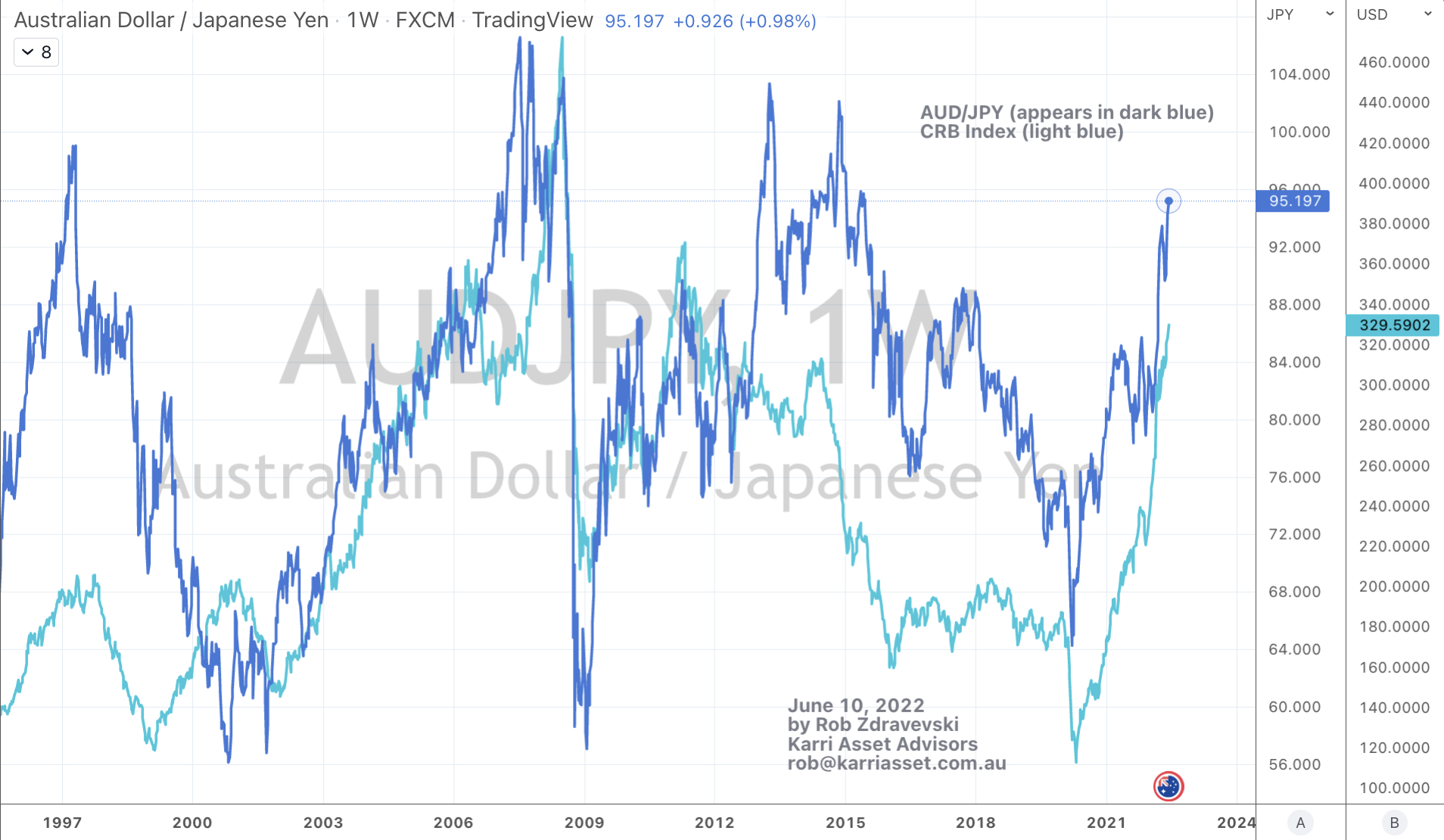

USD/JPY

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

British 10 year government bond year yields

Extremes “below” the Mean (at least 2.5 standard deviations)

None

Oversold (RSI < 30)

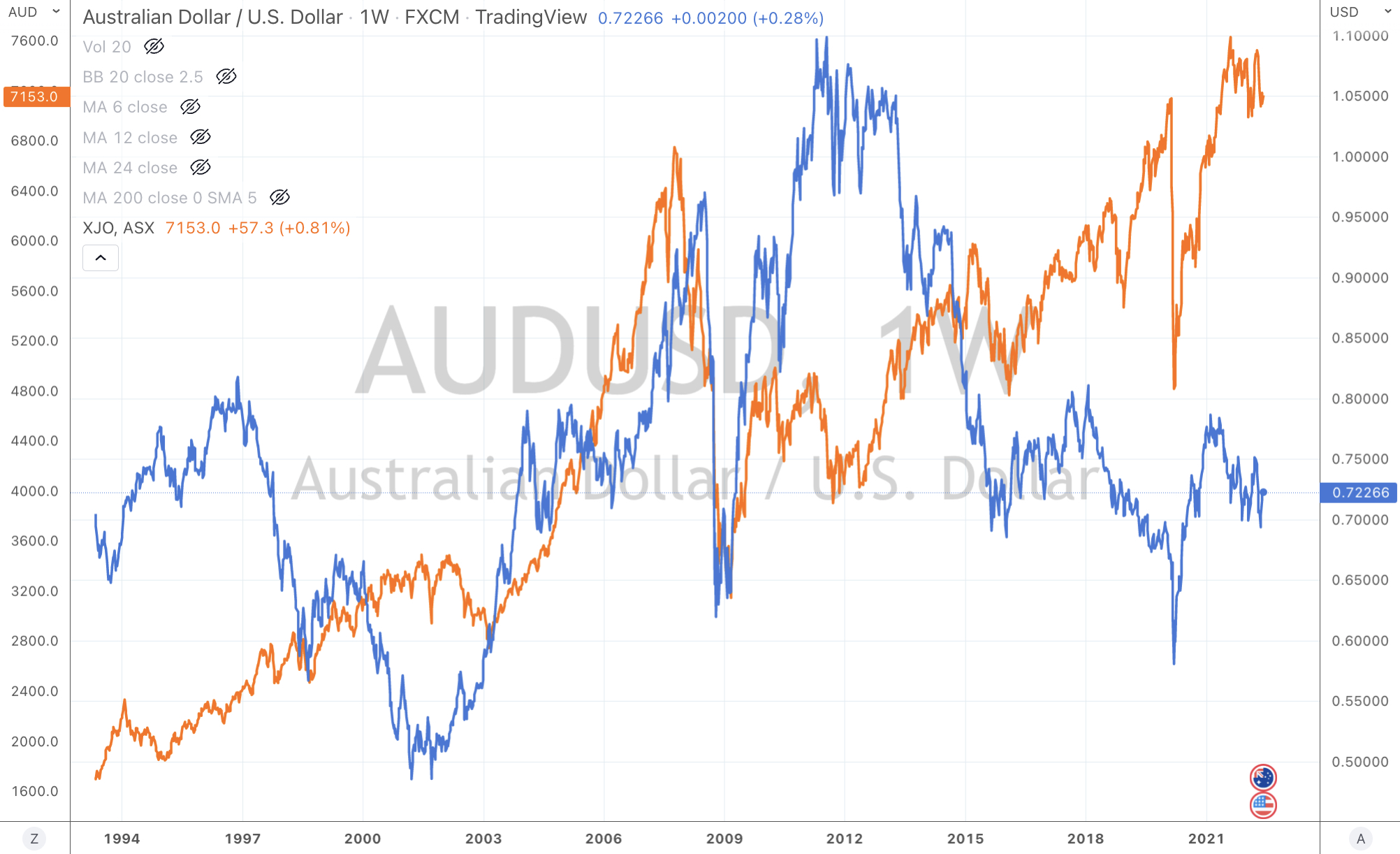

NZD/AUD

JPY/USD

TLT & IEF

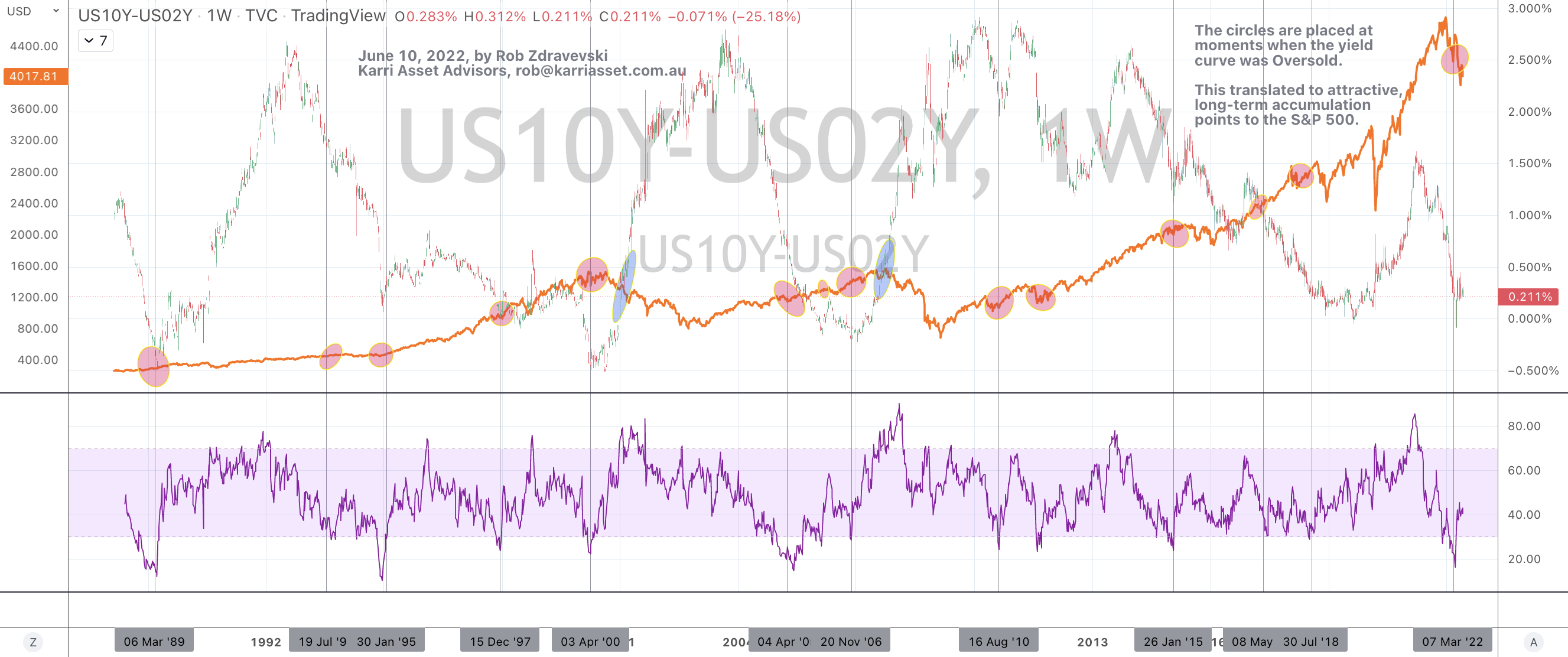

US 10 year minus Australia 10 year government bond yields

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

None

Notes & Ideas:

The big news for the week was that global government bond yields made new, recent highs, everywhere, except for the U.S. 10’s.

The Canadian 10’s moved from 3.07% to 3.38% and Australian 10’s rose from 3.50% to 3.76%, hitting its highest level not seen since June 2014.

All the G-10 nations (except the U.S.) saw their government bond yield rise to mimic June 2014 prices.

While the yield in the U.S. 10 year yield peaked in the past week at 3.18%, it didn’t trade above its week ending May 9th, 2022 high of 3.20%, let alone its 3.25% high seen in October 2018.

Although the U.S. 10’s high in June 2014 was 3.05%.

In other news, the U.S. Dollar Index also failed to trade above its May 9th weekly high and WTI Crude Oil didn’t make news highs either.

Most global equities took a drubbing and the sentiment seems awfully bearish but note that these indices didn’t make ‘lower lows’.

The only equity markets to register gains this week were those tracking Chinese and Hong Kong stocks. The Shanghai Composite Index has risen 9% in 5 weeks and 14% since its April 25 low.

It’s worthy to note that we saw outside bearish reversal week’s in the DAX, CAC, Dow Jones Transports, S&P Mid Cap and Small Cap indices.

However, my work suggests that major western equity indices are not about to embark on a major, new or extended downward leg.

Many indices are already showing weekly RSI readings in their 30’s, they are closing in on their longer term mean reversions, nearing their lower band of normal standard deviations and when coupled with my other trend and momentum indicators, my work suggests that the ‘set-up’ isn’t in place for such a move.

Cryptocurrencies saw more weakness. Ethereum fell 20%. With little fanfare and news, it seems like apathy may mark an upcoming low. I’ve marked $22,500 as a target for Bitcoin. That’s 18% lower than its current price of $27,500 as I write this.

Silver also had a outside bearish reversal week as it works its way down to it 200 week moving average of $20.36, which is a further 7% below todays price.

The CRB (commodities) Index remains overbought, for the 21st consecutive week.

Last week, I wrote that while “Copper rose for the week as did the Copper/Gold ratio. The latter hit and didn’t break resistance.”

This week, Copper fell which aided how the Copper/Gold ratio behaved, for it did not break above that resistance line.

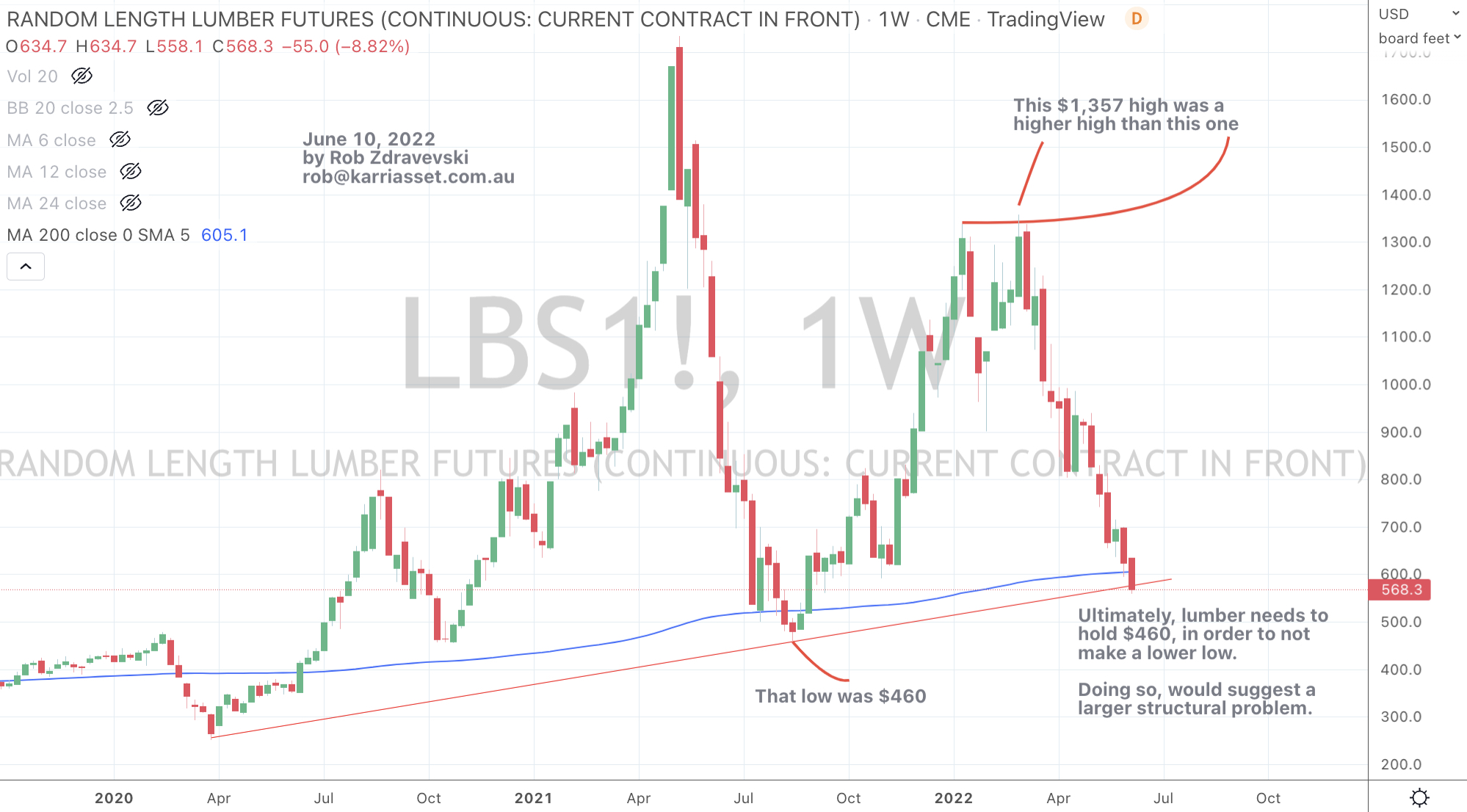

Lumber fell 10% for its 2nd week in a row and a blog post from earlier in the week revises a buying entry point as $460 per tonne.

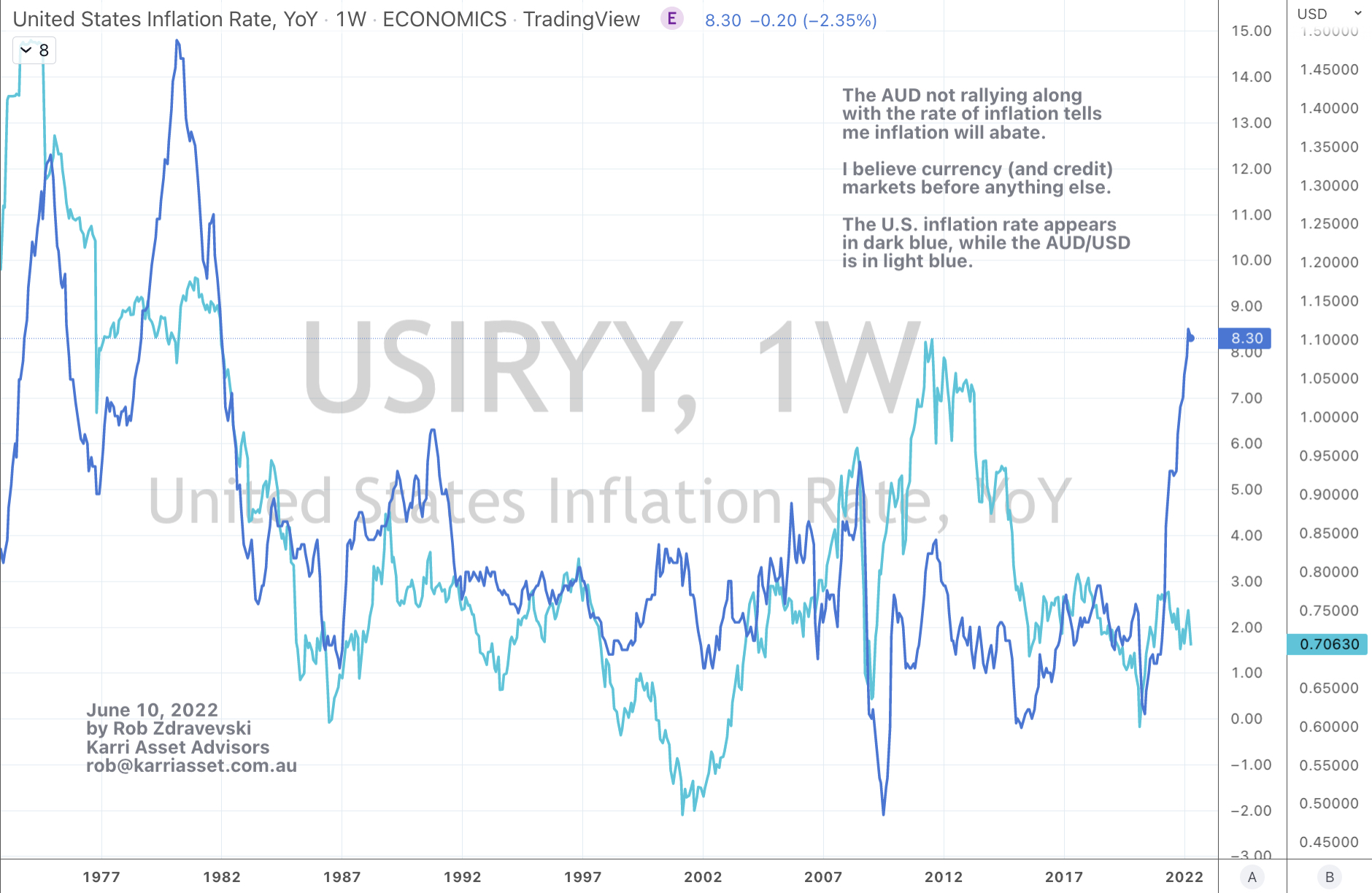

Last week, I wrote a reminder to watch if Gold (in AUD) holds the A$2,500 level.

It did and has, the low for the week was A$2,544

And the Japanese 10’s tell us that things aren’t that bad as they idle around the 26 basis points mark.

The larger advancers over the past week comprised of;

China Coal 7.3%, WTI Crude Oil 1.5%, DXY 2%, Heating Oil 2%, Cattle 2%, Tin 7.3%, Natural Gas 3.8%, Orange Juice 2.4%, Cotton 5%, Uranium 2.5%, Silver in AUD 2.2%, Gold in AUD 3.5%, Corn 6.4%, Soybeans 2.8%, Wheat 3%, Shanghai Composite 2.8%, CSI-300 3.7%, HSCEI 4.7%, HSI 3.4%.

The group of decliners included;

Australian Coal (8.2%), Aluminium (2%), Rotterdam Coal (3%), Baltic Dry Index (11.9%), Gasoil (2.8%), Hogs (2.2%), Copper (4%), JKM (3.5%), Lumber (10.8%), Palladium (4%), Platinum (4%), Gasoline (1.9%), Sugar (2.2%), Urea (9%), Oats (5.7%), Rice (3.3%), Bitcoin (8.5%), Cardano (10.8%), GBTC (3%), Ethereum (20.2%), AEX 2.7%, KBW Bank Index (7.8%), CAC (4.6%), DAX (4.8%), Dow Jones Industrials (4.6%), DJ Transports (7.5%), MIB (6.7%), IBEX (3.8%), Bovespa (5.1%), KOSPI (2.8%), Midcap 400 (4.6%), Nasdaq 100 (3.6%), Sensex (2.3%), Oslo (2.7%), Copenhagen (3.4%), Helsinki (2.7%), Stockholm (3.8%), Russell (4.4%), SMI (3.9%), SOX (7.5%), S&P 500 (5.1%), FTSE-100 (2.9%), Canada’s TSX (2.5%), S&P SmallCap 600 (4.3%), Biotech Index (5.2%) and Australia’s ASX 200 fell 4.2%.

June 12, 2022

by Rob Zdravevski

rob@karriasset.com.au