The following assets (on a weekly timeframe) registered an Overbought reading or traded more than 2.5 standard deviations above its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

Cocoa

Shanghai Composite equity index

Russia’s MOEX equity index

Japan’s Nikkei 225 index

Overbought (RSI > 70)

Hot Rolled Coil Steel (for the 50th consecutive week)

Natural Gas

the Nasdaq 100 index

Amsterdam’s AEX,

and India’s NIFTY 50 equity index

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Aluminium

Assets (securities) within my immediate universe which touched the other side of the extreme, being Oversold (where the RSI is < 30) or were at least 2.5 standard deviations below its mean are;

Extremes “below” the Mean (at least 2.5 standard deviations)

None

Oversold (RSI < 30)

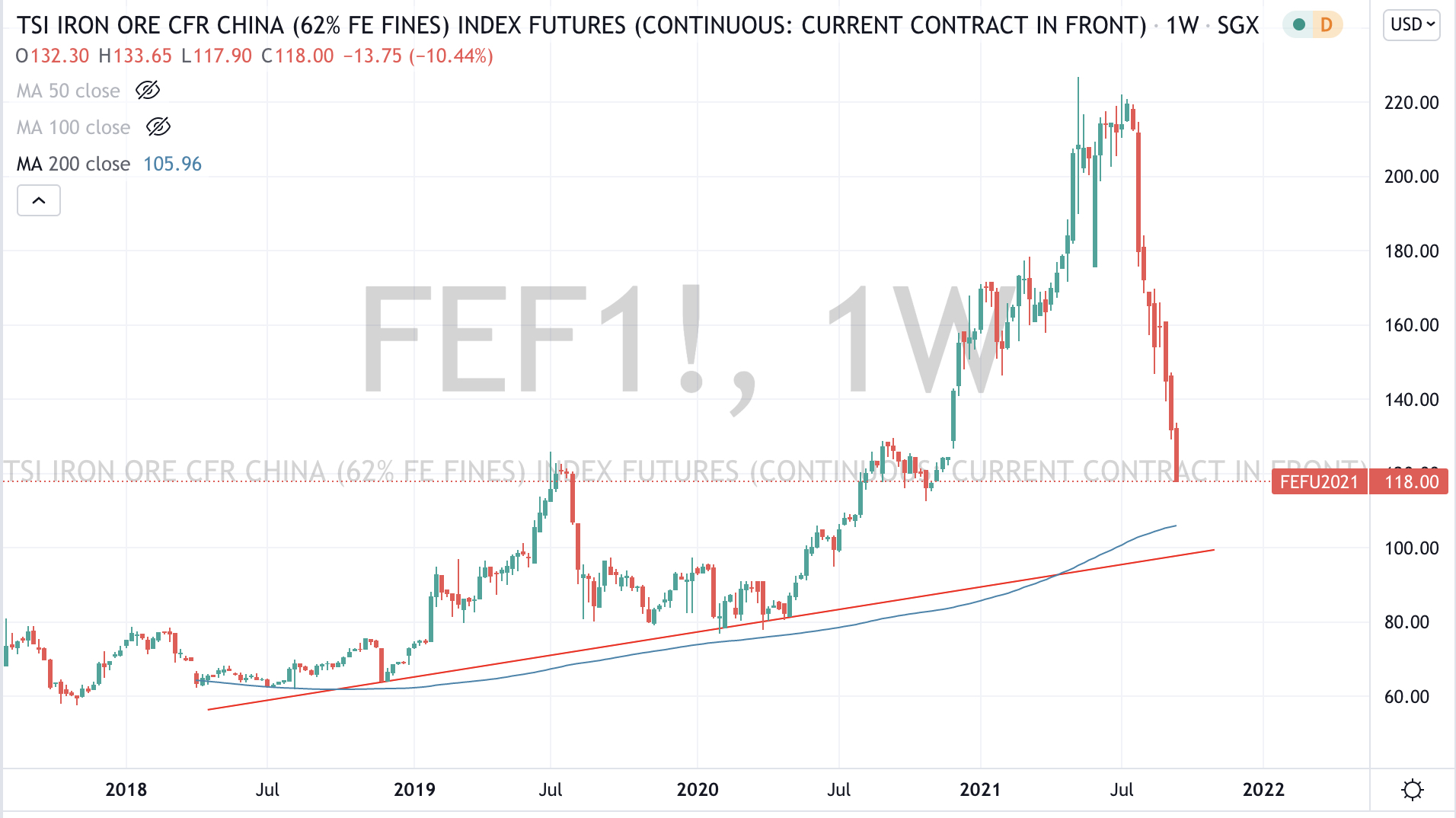

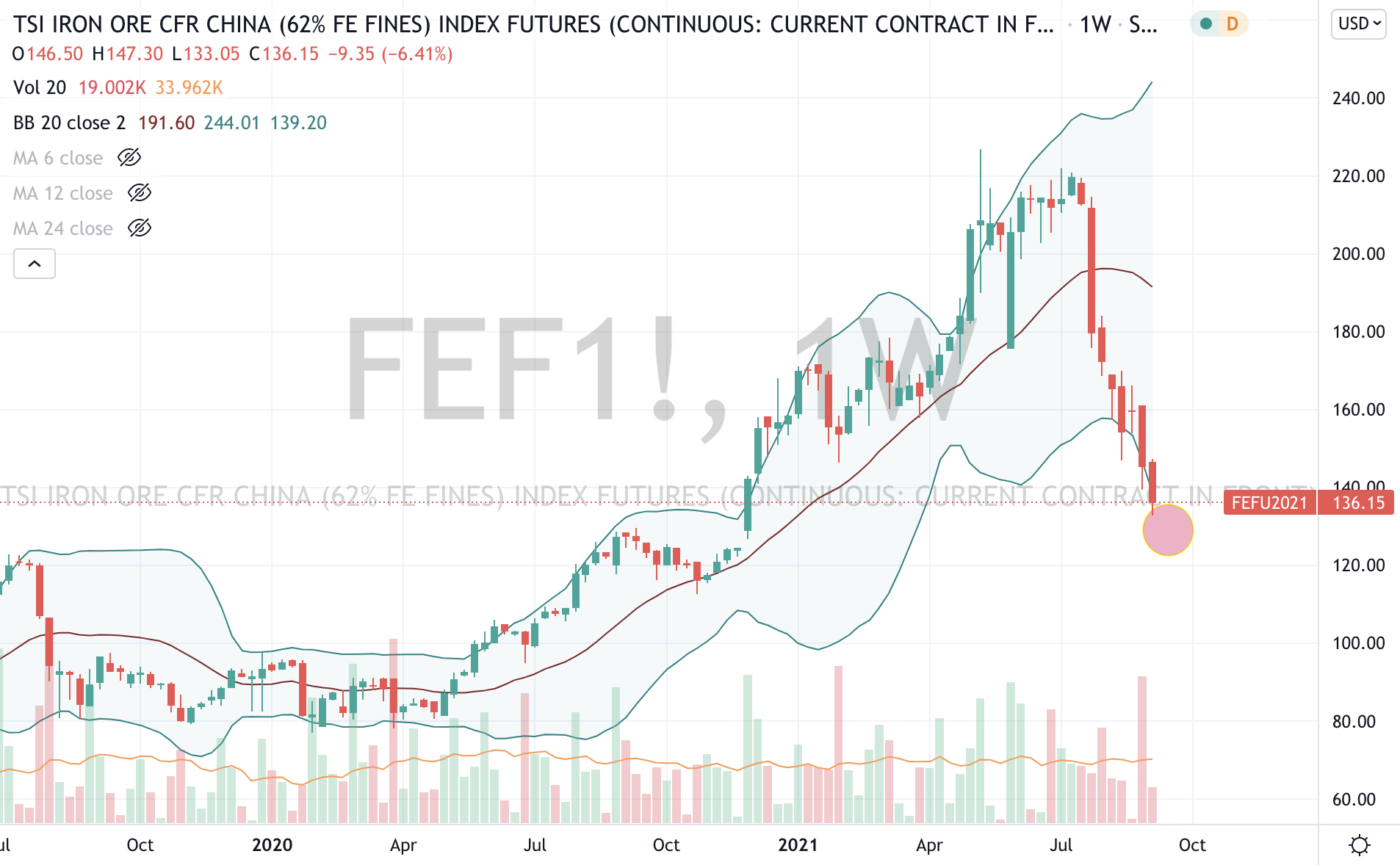

Iron Ore

Brazil’s BOVESPA equity index

Notes & Ideas:

This past week continued last week’s general muted state of activity especially amongst currencies and equities.

Notable departures from the list included the previously overbought Cattle, the S&P 500 and the Nordic stock exchanges.

This list is the smallest over the past 6 months.

The larger advancers over the past week comprised of Aluminium +7%, Natural Gas +5%, Nickel +4%, Copper +2.7% and China’s Shanghai and CSI 300 indices both rose 3.4%.

The Shanghai Composite has risen 8% in the past 3 weeks….

The group of decliners included Platinum (6.3%), Wheat (5%), Sugar (4%), Silver (3.6%), Tin (3.3%), Coffee (2.5%), Cocoa (2%), Gold (2%), Nikkei 22 (2.8%), S&P Midcap 400 (2.7%), both Dow Jones and Nasdaq Transportation indices fell 2.7%, the Bovespa, SMI and Kospi declined (2.3%), Spain’s IBEX (2%), the Dow Jones Industrial Average (2%), the S&P 500 (1.7%) and Australia’a ASX 200 fell 1.6% for the week.

September 11, 2021

by Rob Zdravevski

rob@karriasset.com.au