The following assets (on a weekly timeframe) registered an Overbought reading or traded more than 2.5 standard deviations above its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

Gasoil

Overbought (RSI > 70)

Aluminium

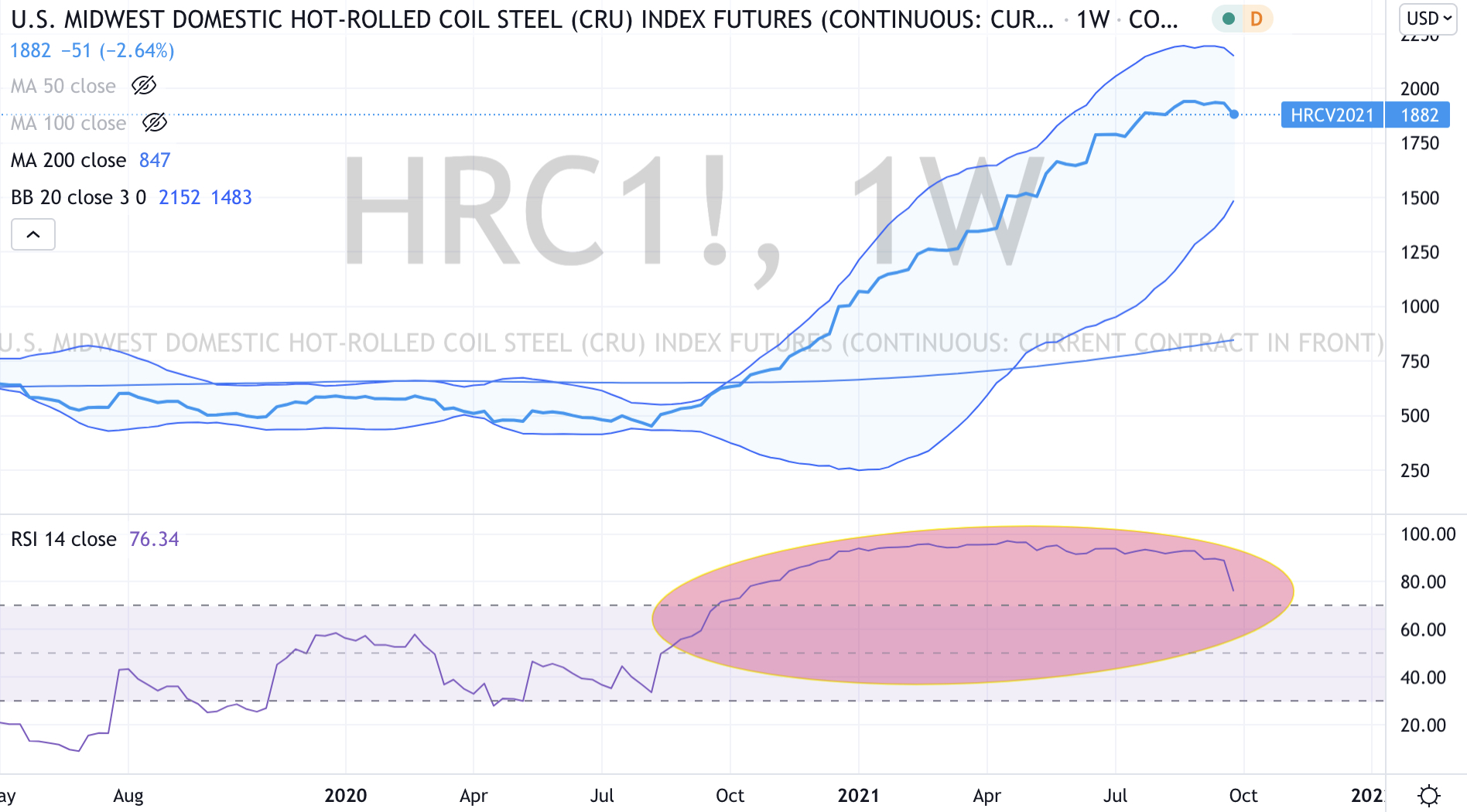

Hot Rolled Coil Steel (for the 52nd consecutive week)

The Baltic Dry Index,

Amsterdam’s AEX,

Tin

Natural Gas

and India’s Sensex & NIFTY 50 equity indices

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

None

Assets (securities) which touched the other side of the extreme, being Oversold (where the RSI is < 30) or were at least 2.5 standard deviations below its mean are;

Extremes “below” the Mean (at least 2.5 standard deviations)

Copper

Germany’s DAX

Brazil’s BOVESPA equity index

U.K.’s FTSE 100 equity index

The S&P MidCap 400 index

And as surprising as it seems, the Dow Jones Industrial Average (there is more work to be done on what it means in relation to recent and future action in the U.S. year government bond yields).

Oversold (RSI < 30)

Iron Ore

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean.

None

Notes & Ideas:

The big news the price action in the bond market and what may occur this coming week. Avid readers will know that I always advocate the importance of watching the credit markets in order to help you understand the equity markets.

Bond yields are rising. It’s a topic I have been presenting to various investment groups lately, albeit my view of notably higher interest rates is a multi-year view.

Over the past 2 weeks, we’ve seen the Aussie 10 (10’s) year government bond yield rise from 1.27% to 1.40%. The Canadian’s have followed rising 1.29% to 1.38%, Spain’s 10’s have risen by a third (0.35% to 0.43%) and the U.K’s 10’s have soared from 0.58% to 0.92% over the past 4 weeks.

These are notable moves not necessarily signalled in the financial media and they are more evident considering these yields bounced off their Oversold extremes several weeks ago.

I am also watching the Copper/Gold Ratio to also assist with a directional call on interest rates.

The larger advancers over the past week comprised of Brent crude 3.7%, WTI crude 3%, Aluminium 2%, Coffee 4.3%, Heating Oil 2.6%, Tin 5%, Baltic Dry Index (shipping) 8.6%, Platinum 5.3%, Wheat 2% & the U.S. KBW Banking Index 3%.

The group of decliners included Cocoa (2.8%), Bitcoin (11%), Ethereum (15%), the Hang Seng Index (2.9%) and HSCEI (3.8%) (note: interested buyer at 7,800).

Chinese equity indices are nearing oversold with the CSI 300 still heading lower. France’s CAC-40 has entered a new weekly downtrend.

In FX, the AUD and EUR are trending lower against the USD. The Swedish Kroner also looks set to move lower.

A suggested rise in the U.S. Dollar portends weaker commodity prices including Gold whose downtrend is picking up steam. In fact, Gold in AUD needs to hold hold a A$2,312 support level.

But I think that higher interest rates, lower commodity prices and a weaker AUD is short lived, in the short-term the recent higher moves in rates could be a head-fake.

September 26, 2021

by Rob Zdravevski

rob@karriasset.com.au