The following assets (on a weekly timeframe) registered an Overbought reading or traded more than 2.5 standard deviations above its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

Shanghai Composite equity index

Russia’s MOEX equity index

Bloomberg Commodity Index

Overbought (RSI > 70)

Hot Rolled Coil Steel (for the 51st consecutive week)

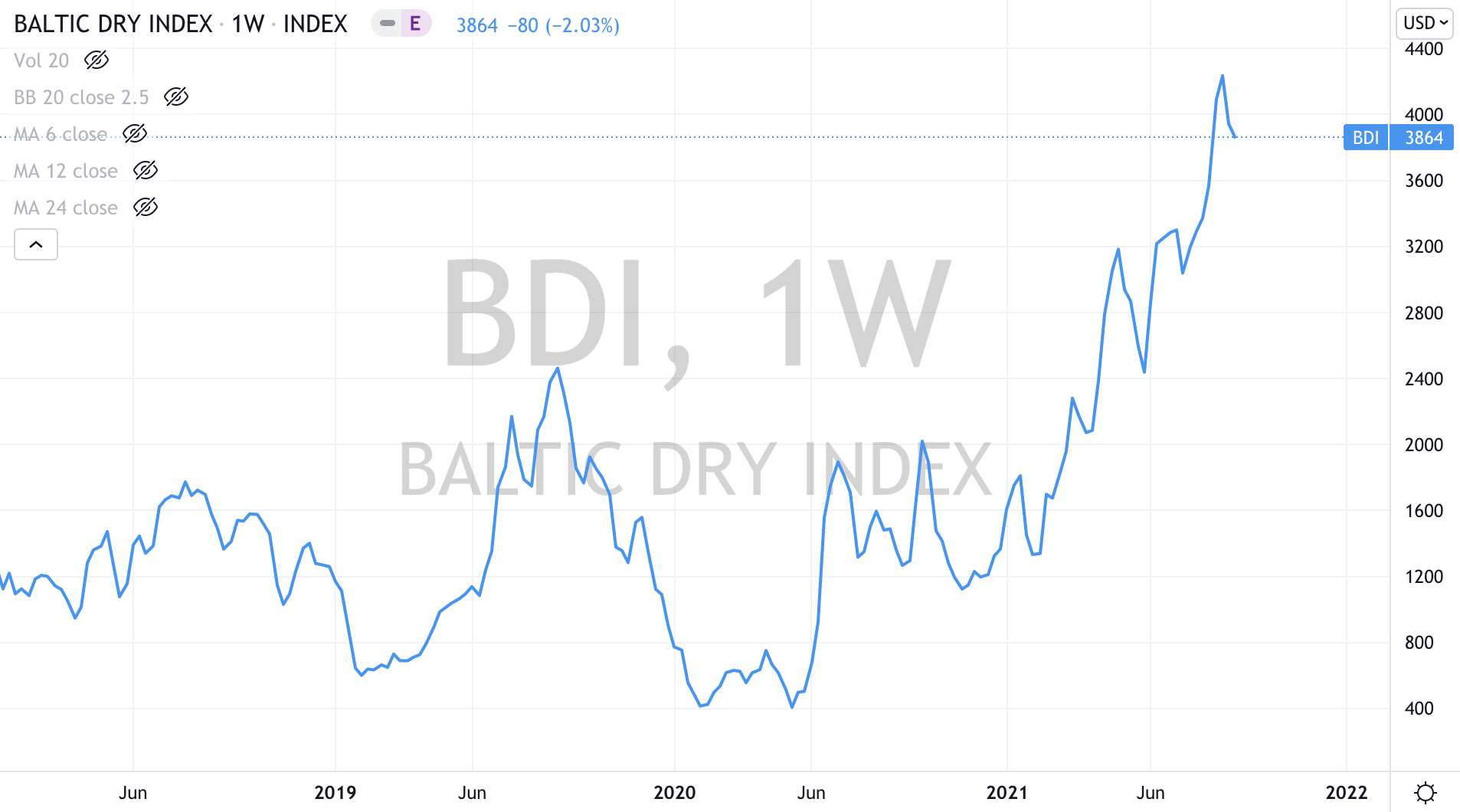

The Baltic Dry Index,

Amsterdam’s AEX,

and India’s NIFTY 50 equity index

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Aluminium

Natural Gas

Assets (securities) which touched the other side of the extreme, being Oversold (where the RSI is < 30) or were at least 2.5 standard deviations below its mean are;

Extremes “below” the Mean (at least 2.5 standard deviations)

Brazil’s BOVESPA equity index

U.K.’s FTSE 100 equity index

Oversold (RSI < 30)

None

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean.

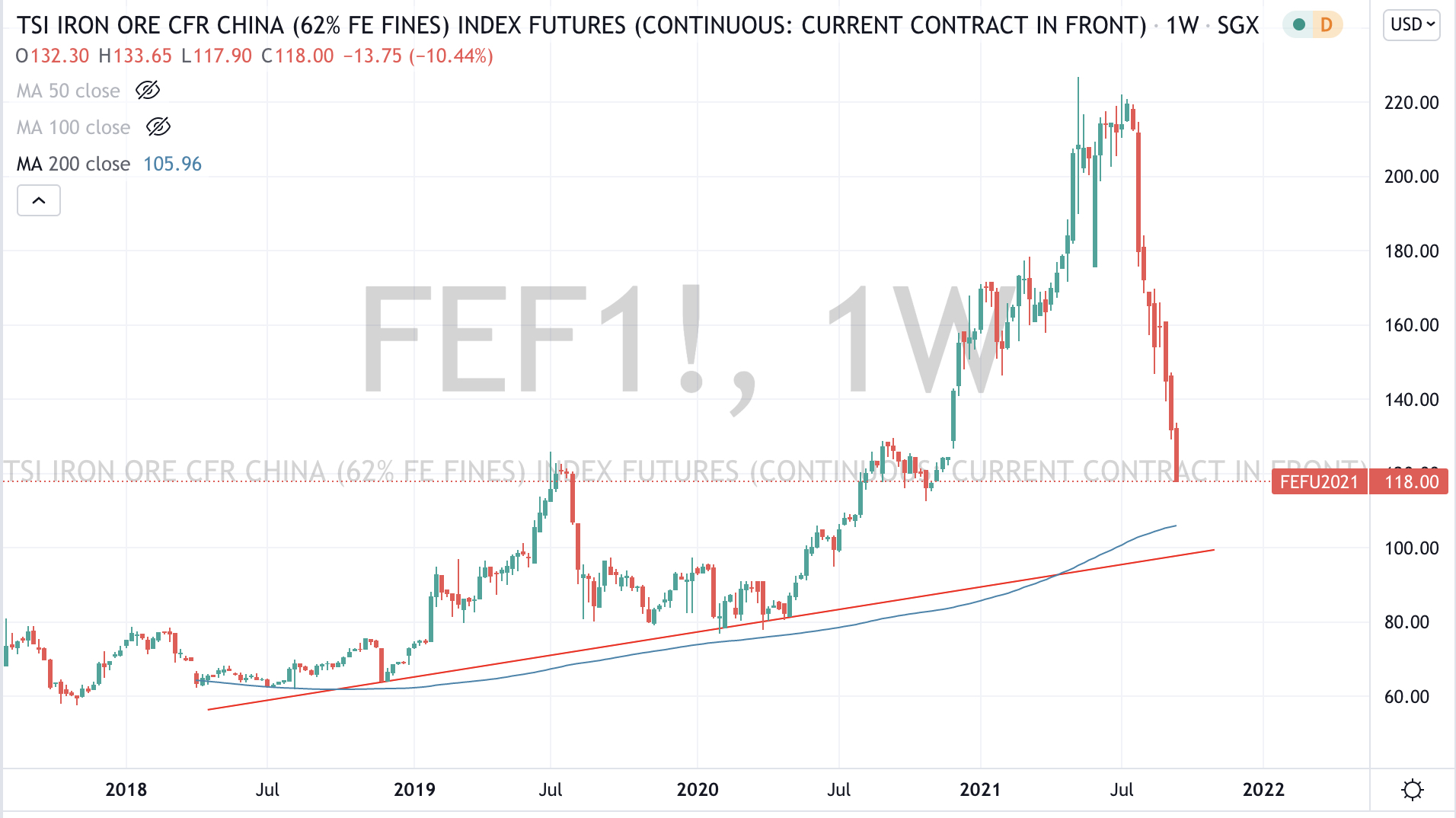

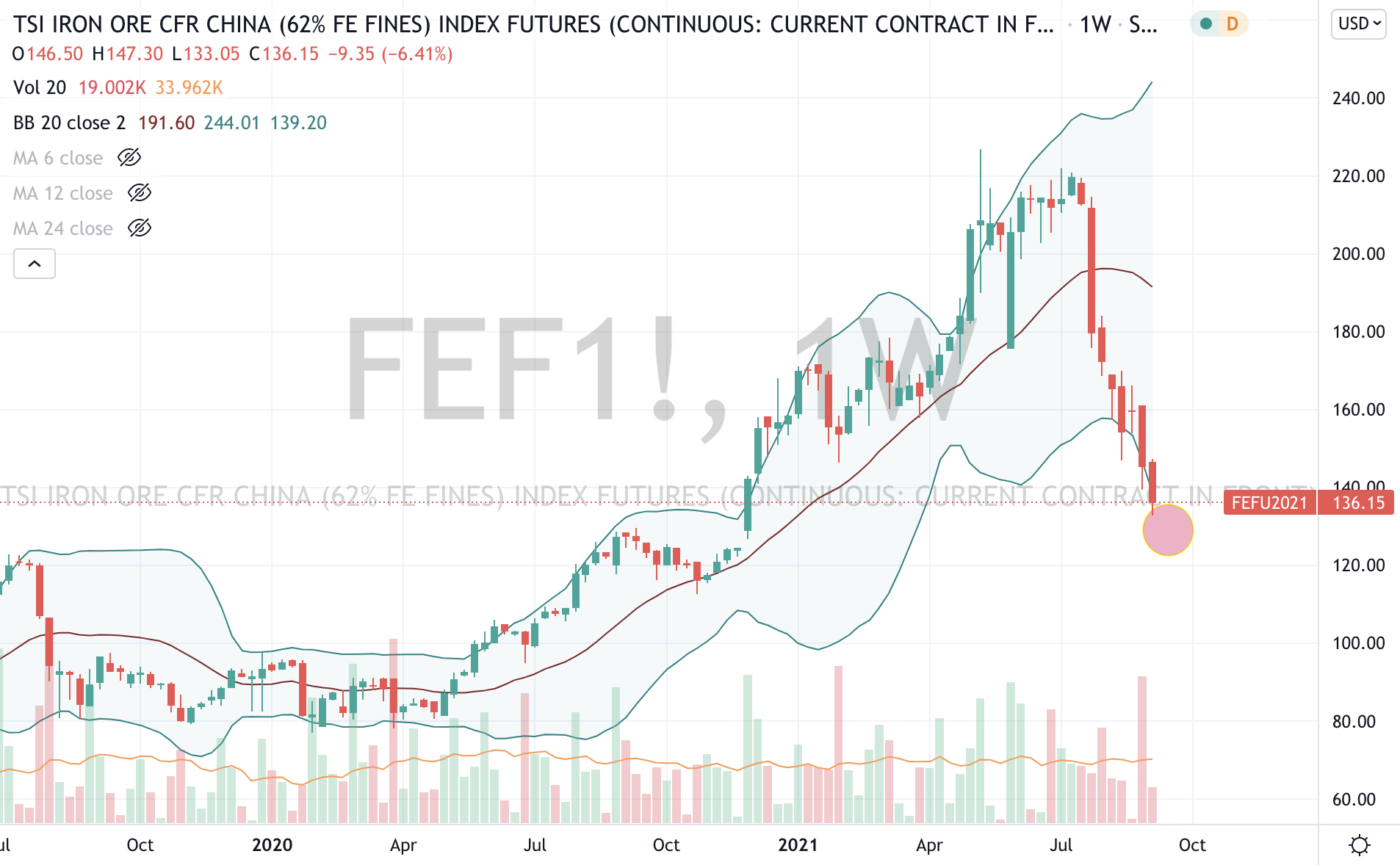

Iron Ore

Notes & Ideas:

And this week’s list is smaller again as many asset as finding their new trends on their way to an ‘extreme’.

The larger advancers over the past week comprised of Natural Gas +3.4%, Baltic Dry Index +11%, WTI Crude +3%, Brent Crude +3.3%, Tin +2%, Wheat +3%, Cocoa +2.3%, Rice +2%, Heating Oil +3%, Gasoil +3.5% and Lumber and lean Hogs both rose 4%.

The group of decliners included Iron Ore (13%), Copper (4.6%), Platinum (2.7%), Gold (2.2%), Nickel (4%), Shanghai Composite (2.4%), China’s CSI 300 (3.1%), the HSCEI (4.8%), Brazil’s Bovespa (2.5%) and the Helsinki 25 (2.5%)

Notable deletes include;

Cocoa, Japan’s Nikkei 225 index, the Swiss SMI and the Nasdaq 100 index fell from its overbought levels, following the S&P 500’s departure from the list last week.

Incidentally, it staggers me how much energy is spent by market pundits ‘calling a correction’. Beyond the perspective that 10% decline in the S&P 500 would merely see it trading at levels seen this past May but it may surprise some readers that it has already cleaned 2.5% from its recent September 2nd intra-day high of 4,545.

Amongt the list of the week’s advancers and decliners, Silver’s decline of 6.5% caught my eye, adding to the previous week’s fall of 3.6%. Although it’s not trading at my ‘extremes’, it is already 2 standard deviations below its weekly mean.

In other news, Brazil’s Bovespa has now fallen 8% over the past 3 weeks and Iron Ore has halved since July 19th.

Media mentioned Aluminium’s climb to $3,000 but didn’t give a glance when it was $1,500 only a year ago.

Natural Gas continues to soar and has, ever since it broke above a resistance trend line which I wrote about in this post, The Mother of All Breakouts

Iron Ore has now fallen to the $124 target (currently trading at $119) which I have been writing about, however I am now revising my downside target to the $99 level.

The chart below shows the price of Iron Ore converging to its 200 week moving average.

Mean reversion is another topic I have been harping on about lately too, especially amongst commodities and selected stocks which have soared to extremes and more so those price charts resembling parabolas.

This means I now look for Fortescue Metals (FMG.AX) to trade down to the $15.50 mark and BHP (BHP.AX) to visit $38.50 with $34.50 presenting a compelling entry point.

While all of that is going on, cheaper iron ore means better profits for steel makers.

“Container shipping remains the star. It now costs $14,287 to haul a 40-foot steel box from China to Europe. That’s up more than 500% on a year earlier and is pushing up the cost of transport everything from toys to bicycles to coffee.”

In the next post, I’ll send a chart of what the Baltic Dry Index has done over the past 16 months.

The following assets (on a weekly timeframe) registered an Overbought reading or traded more than 2.5 standard deviations above its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

Cocoa

Shanghai Composite equity index

Russia’s MOEX equity index

Japan’s Nikkei 225 index

Overbought (RSI > 70)

Hot Rolled Coil Steel (for the 50th consecutive week)

Natural Gas

the Nasdaq 100 index

Amsterdam’s AEX,

and India’s NIFTY 50 equity index

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Aluminium

Assets (securities) within my immediate universe which touched the other side of the extreme, being Oversold (where the RSI is < 30) or were at least 2.5 standard deviations below its mean are;

Extremes “below” the Mean (at least 2.5 standard deviations)

None

Oversold (RSI < 30)

Iron Ore

Brazil’s BOVESPA equity index

Notes & Ideas:

This past week continued last week’s general muted state of activity especially amongst currencies and equities.

Notable departures from the list included the previously overbought Cattle, the S&P 500 and the Nordic stock exchanges.

This list is the smallest over the past 6 months.

The larger advancers over the past week comprised of Aluminium +7%, Natural Gas +5%, Nickel +4%, Copper +2.7% and China’s Shanghai and CSI 300 indices both rose 3.4%.

The Shanghai Composite has risen 8% in the past 3 weeks….

The group of decliners included Platinum (6.3%), Wheat (5%), Sugar (4%), Silver (3.6%), Tin (3.3%), Coffee (2.5%), Cocoa (2%), Gold (2%), Nikkei 22 (2.8%), S&P Midcap 400 (2.7%), both Dow Jones and Nasdaq Transportation indices fell 2.7%, the Bovespa, SMI and Kospi declined (2.3%), Spain’s IBEX (2%), the Dow Jones Industrial Average (2%), the S&P 500 (1.7%) and Australia’a ASX 200 fell 1.6% for the week.

It’s close to the $132 mark which is the upper end of the circled range in my article link below.

$132 is also its 100 week moving average.

Albeit there is a gap in the chart at $124.50 and I think it could be ‘backed and filled’, notwithstanding an additional 4%-7% decline, Iron Ore is nearing the region of a ‘trading buy’, which may give buyers a 35% bounce up to the $180 mark.