A story about the AUD and the ASX 200

June 9, 2022 Leave a comment

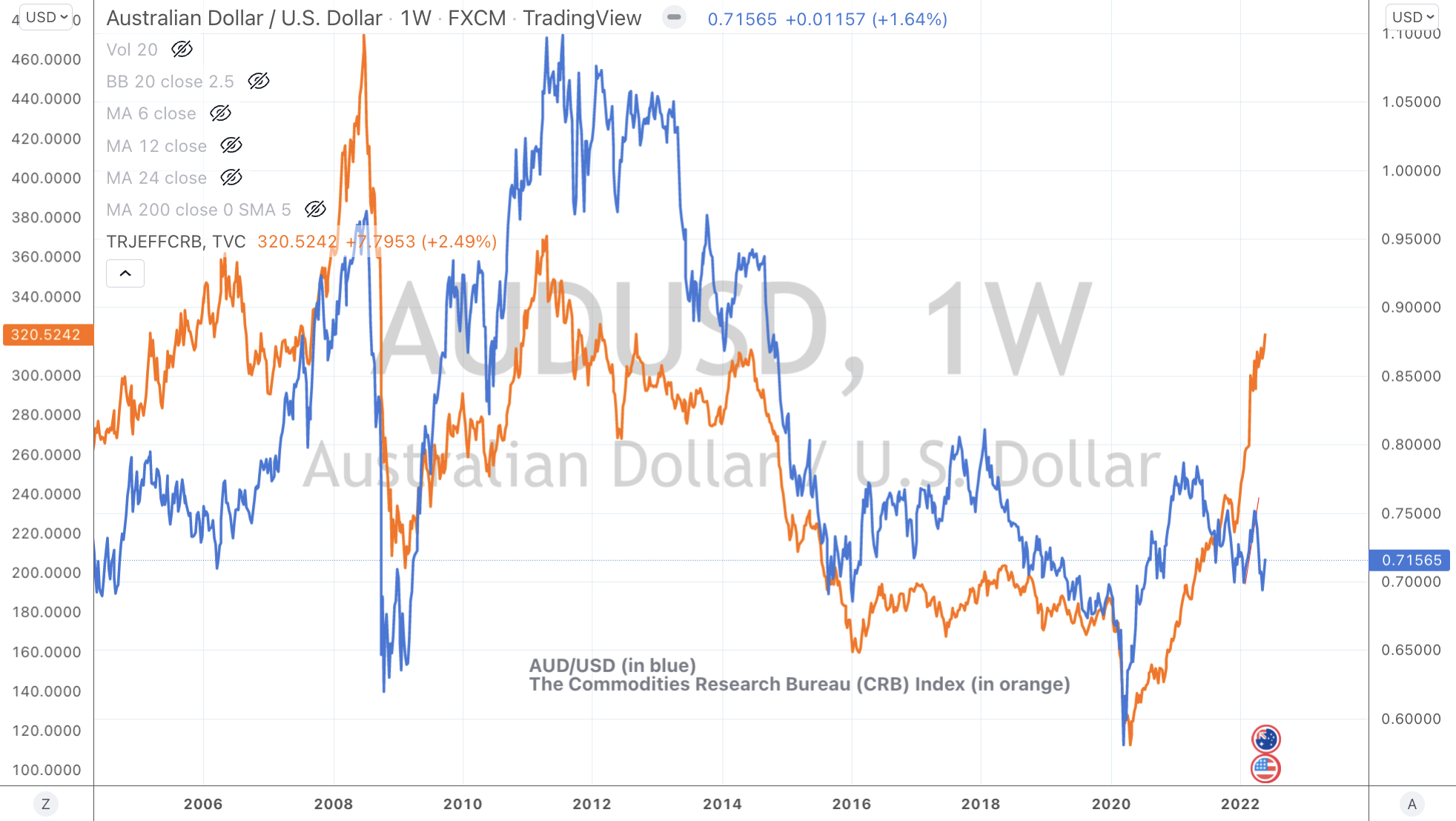

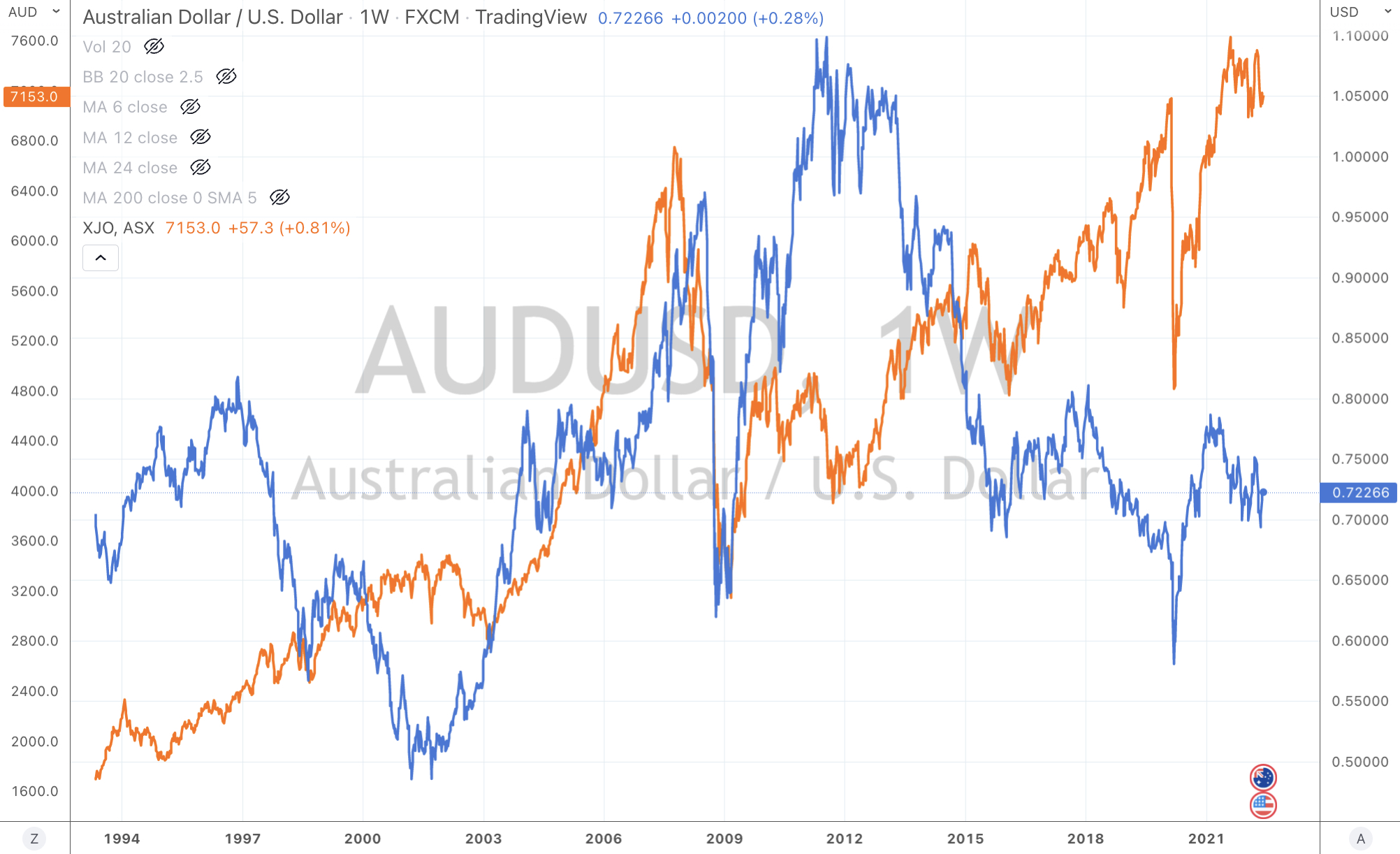

Check out the chart below.

It is the Australian Dollar (vs USD) laid over the ASX 200.

(AUD in blue and the ASX 200 is in orange)

Other than a couple divergences (in 2001 and 2013), this 30 year chart shows that these two prices generally move in lockstep.

Some people also call this an analog or correlation.

However, the content in this note carries a correlation to a note written earlier this week, where I state that the AUD may rise a little to close that divergence to commodity prices……

but the larger move should be seen with a decline in commodity prices.

If we see this evolve, the ASX 200 is vulnerable due to its large weighting to commodity and mining related companies.

This earlier note (below) about the Australian Dollar versus the Japanese Yen is also related.

https://robzdravevski.com/2022/06/01/aussie-yen-leads-the-spx-in-risk/

In the AUD/JPY case, we already have a very strong Aussie. The Yen is at a 20 year low and trading at extremes Oversold levels against many crosses.

The USD is inversely at Overbought levels.

So, the if the USD takes a break and declines a little, then the Yen rises against it.

In turn, the AUD stays supported by weaker USD, but stifled from any meaningful advance by a stronger Yen.

I see a ‘lid’ holding the AUD from rising significantly.

A rising Yen signifies a little equity risk is in the air and specifically, the sector which is the ‘frothiest’ are commodities.

Should we see commodities decline, inflation will take a breather and those companies producing ‘end-product’ will see cheaper ‘input’ prices.

So, not all is lost.

I’ll leave you with a chart showing the AUD/USD (the blue line) versus West Texas Intermediate (WTI) Crude Oil (in orange).

The AUD/USD would need to trade above 0.7670 before I entertain the possibility of a rally into the 80’s.

Otherwise, I’ll look for lower prices and mean reversion in a host of commodity prices before they decide their next move.

June 9, 2022

by Rob Zdravevski

rob@karriasset.com.au