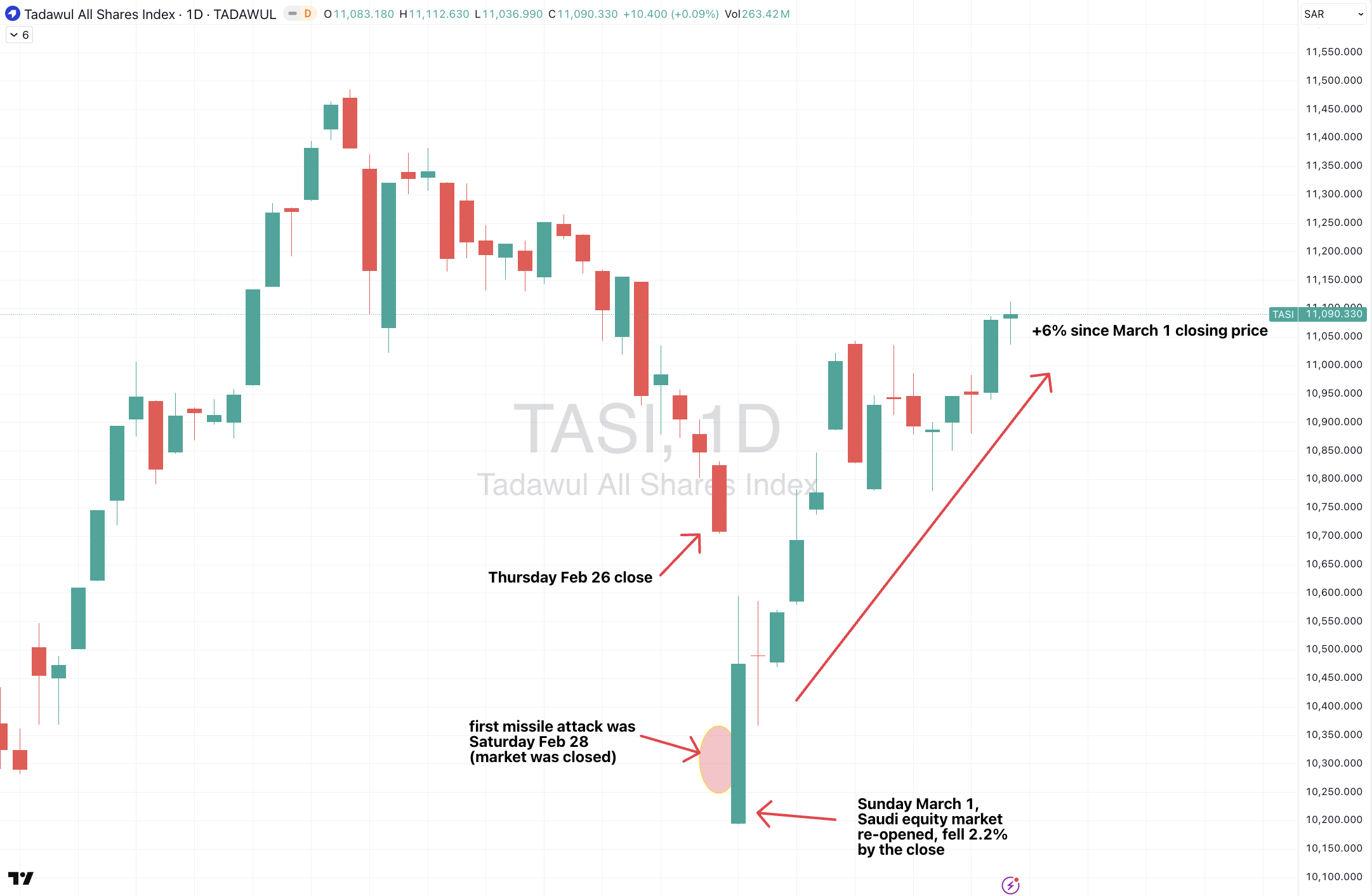

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

n.b. pricing of (commodity) futures contracts is only considering the immediate front month.

* denotes multiple week inclusion

Extremes above the Mean (at least 2.5 standard deviations)

10-year Austria, Belgian, Chilean, German, Danish, Spanish, Finnish, French, British, Norwegian, Kiwi and U.S. government bond yields.

2, 3, 5, 7 and 20-year U.S. government bond yields.

British 30-year bond yields

U.S. 5–7-year Investment Grade and High Yield yields

U.S. 10-year bond yield minus U.S. 10 year inflation breakeven rate

Cotton *

Sugar *

Oats *

Overbought (RSI > 70)

2-year British and Japanese government bond yields.

Aussie and British 3-year government bond yields.

Australian and Japanese 5-year bond yields.

5 & 10-year Japanese bond yields.

Richards Bay Coal *

Rotterdam Coal *

Bloomberg Commodity Index *

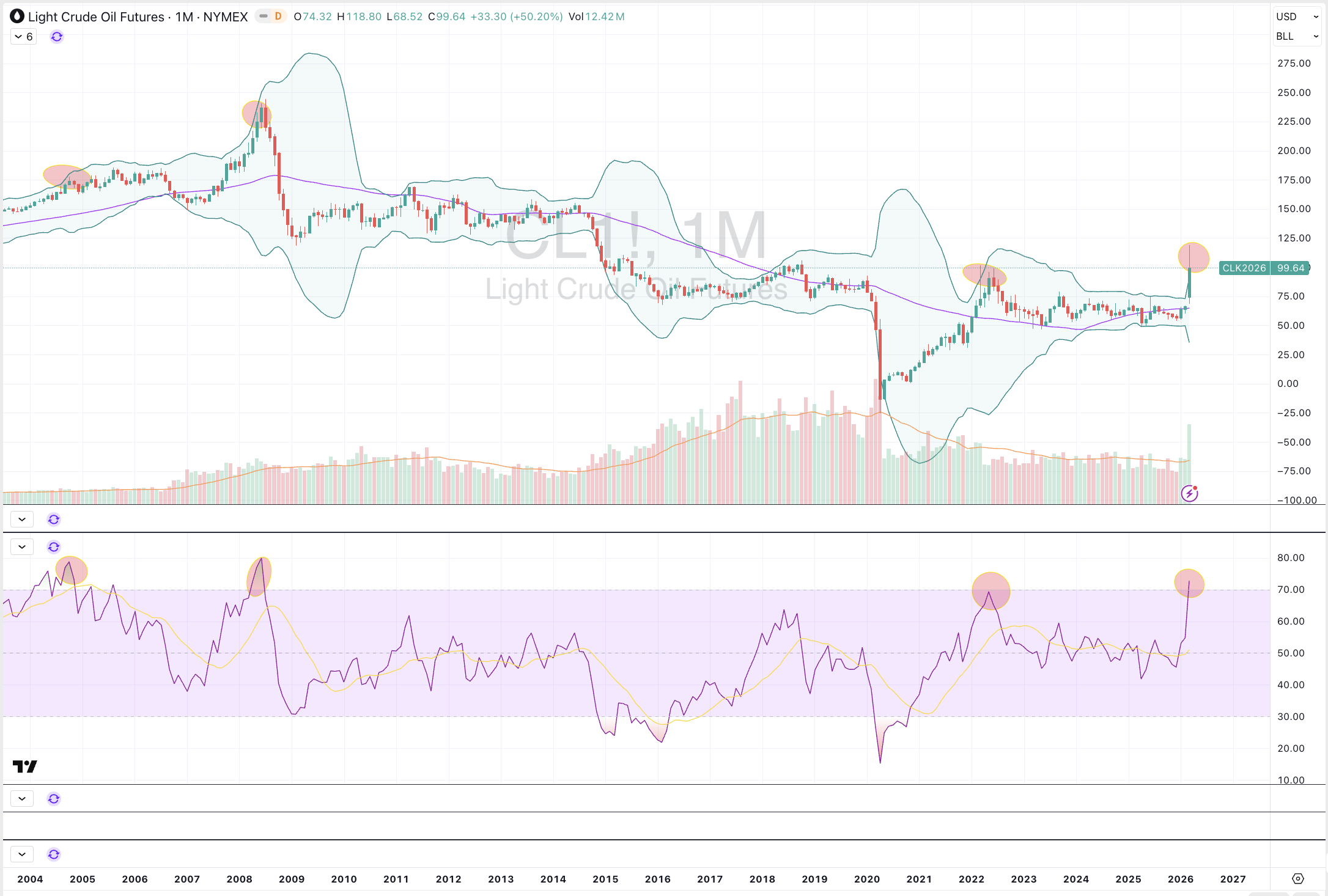

Brent Crude Oil *

WTI Crude Oil *

JKM LNG in USD

Newcastle Coal *

S&P GSCI Index *

CRB Index *

Urea (U.S, Gulf and Middle East) *

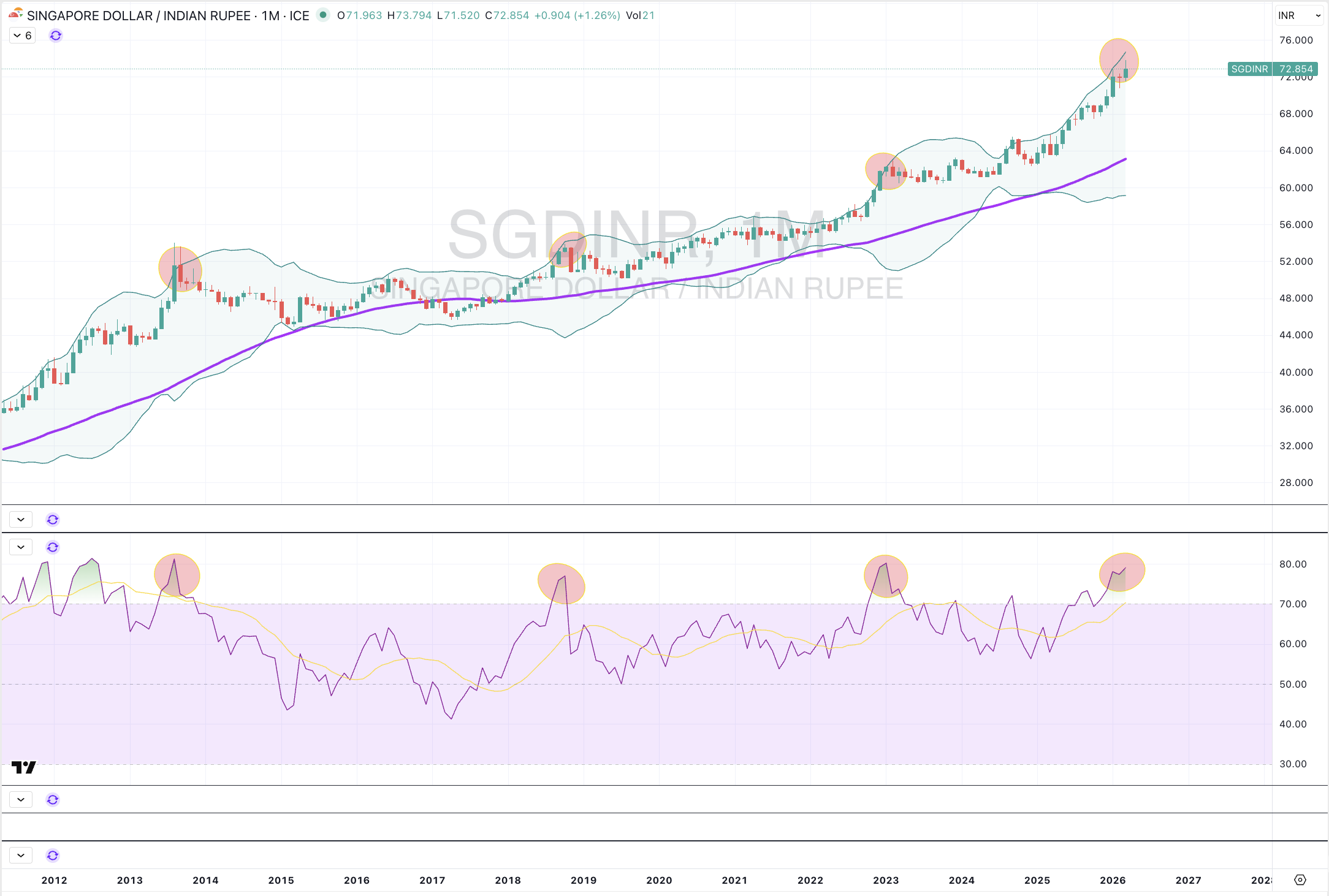

AUD/INR *

OBX *

The Overbought Quinella (Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Australian, Chilean, German and Italian 2-year government bond yields.

5 year Australian and German bond yields

10-year Greek, Indonesian, Italian, Korean, Polish, Portuguese & Turkish government bond yields.

Heating Oil *

JKM LNG in Yen *

Gasoline *

Gasoil *

Extremes below the Mean (at least 2.5 standard deviations)

IEF

IEI *

SHY *

U.S. 10-year minus U.S. 2-year bond yield spread *

U.S. 10-year minus 5-year bond yield spread

U.S. 30-year minus U.S. 10-year bond yield spread *

Lumber

PHP/USD

CSI 300

CAC Index *

DAX Index *

MIB

HSCEI

Hang Seng

Nasdaq Composite *

Nasdaq 100

SMI

S&P 500

ASX Industrials *

ASX Small Caps

Oversold (RSI < 30)

Australian 10-year minus Aussie 2-year bond yield spread

Cocoa

NZD/AUD *

HKD/USD *

KRW/USD *

IDX Composite *

The Oversold Quinella (Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

INR/USD *

NIFTY *

SENSEX *

Notes & Ideas:

Government bond yields rose, again.

A few more 10-year government bond yields joined the overbought list.

4 weeks of higher yields are seen in Australian, Belgian, Canadian, German, Danish, Spanish, Finnish, French, Greek, Japanese, Dutch, Kiwi, Polish, Portuguese, Swedish and American 10 year bonds.

Chilean 10-year yields have climbed for 5 weeks.

The following also have 4 week streaks of higher yields; Aussie, German, Italian and U.S. 2’s, the U.S. 3 year, German and American 5 years along with U.S & British 30 years.

U.S. 5 and 10 years minus inflation spread yields have also increased for 4 weeks.

Meanwhile, British 3 and 5 year bond yields fell and snapped their 4 week rise.

And Chilean 2-year yields have risen for 8 consecutive weeks.

Equities were mainly lower, in a tale of some streaks being extended while others were broken.

Taiwan’s TAEIX, South Korea’s KOSPI and Israel’s TA 35 Index were the last to leave overbought land.

The Shanghai Composite, All World Developed ex USA, DAX, Hang Seng, IBB, Indonesia’s IDX, FTSE 250, NBI, Stockholm, PSE and XBI are in 4 week losing streaks.

The DJ Industrials, Nasdaq Composite, Nasdaq 100, NIFTY, SENSEX, S&P 500 and ASX Financials have fallen for 5 weeks.

China’s FCTAC has declined for 6 weeks.

Austria’s ATX, Russell 2000, S&P Small Cap 600, KRE Regional Banks, S&P MidCap 400, Copenhagen, S&P 600 and Nasdaq Transports rose to snap their 4 straight weeks of decline.

China’s FCATC has fallen for 5 weeks.

Pakistan’s KSE has declined for 9 weeks.

Inversely, Norway’s OBX has risen for 9 weeks.

And India’s NIFTY is at its lowest close since early April 2025.

Commodities were mixed.

Intra-week saw large swings but the changes in week to week close where muted and subdued.

Oils, Distillates, Aluminium, Cotton, Silver & Tin were the notable gainers.

Gases, Coffee, Cocoa, Palladium, Platinum & Oats were amongst the decliners.

Oats, Palm Oil and Dutch TTF Gas left overbought territory.

WTI Crude, CRB Index, Gasoil and Middle Eastern Urea have closed higher for 6 weeks straight.

Gasoline, Brent Crude, Heating Oil, JKM LNG snapped their 5-week streak of higher prices.

Sugar #16 is in a 7-week winning streak.

Palladium and Platinum have declined for 4 weeks, falling 27% and 23% respectively, over that time.

And U.S. Gulf Urea prices have risen for 16 consecutive weeks.

Currencies were quieter.

The Aussie fell.

All of the Aussie pairs except against the Kiwi and Rupee exited

AUD/THB fell and snapped a 5-week rising streak.

CAD was lower.

Euro rose.

The USD was mainly higher,

CLP/USD rose slightly to snap its 5-week losing streak.

And the USD/ZAR is in a 4-week winning streak.

The larger advancers over the past week comprised of;

Aluminium 2%, WTI Crude Oil 1.4%, Cotton 3.2%, Heating Oil 10.7%, Cattle 2.3%, Tin 5.9%, LME Aluminium 3.3%, Orange Juice 9.3%, Urea U.S. Gulf 1.9%, Gasoil 1.9%, Silver in AUD 4.9%, Silver in USD 2.7%, Gold in AUD 2.1%, Wheat 1.6%, DJ Transports 1.8%, BOVESPA 3%, Mexico 4%, SA40 1.8%, SMI 2%, S&P 600 1.1%, Nasdaq Transports 1.8%, TSX 2.1%, Vietnam 1.5% and ASX Materials rose 4.6%.

The group of largest decliners from the week included;

Cocoa (2.8%), JKM LNG (6%), Arabica Coffee (2.6%), Lumber (2.1%), Palladium (2.7%), Platinum (5.1%), Gasoline (1.3%), Robusta Coffee (1.9%), Dutch TTF Gas (8.4%), Oats (4.6%), CSI 300 (1.4%), FCATC (2.9%), Nasdaq Composite (3.2%), KOSPI (5.9%), FTSE 250 (1.8%), Nasdaq 100 (3.2%), SOX (2.8%), S&P 500 (2.1%), TA35 (5%) and BIST fell 2.7%.

March 29, 2026

By Rob Zdravevski

rob@karriasset.com.au