Macro Extremes (week ending April 28, 2023)

April 30, 2023 Leave a comment

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

EUR/USD

DKK/USD

AUD/IDR

Overbought (RSI > 70)

Silver (in AUD)

Gold (in AUD)

Russia’s MOEX Index

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Sugar

EUR/AUD

Extremes “below” the Mean (at least 2.5 standard deviations)

China 10 year government bond yields

U.S. 10 year bond yield minus German 10 year bond yield

Iron Ore

Corn

Oats

Soybeans

Oversold (RSI < 30)

U.S. 5 year bond yield minus U.S. 3 month bond yield

Australian Coking Coal

JKM LNG Gas

Lithium Hydroxide

AUD/GBP

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

None

Notes & Ideas:

Equities generally had quiet week, again, with a slight bias towards weaker prices.

For instance, the S&P 500 rose 0.9%, while Midcaps and Smallcaps fell 0.3% and 1% respectively.

The SOX, FTSE and ASX smallcaps fell between 0.3% and 0.9% for the week, while the ASX 200 rose 0.2%.

Trend less equity markets remains the trend, for now.

Government bond yields fell. While my trend analysis favours lower yields, pattern recognition work tells me it’s prudent to identify the sideways and ‘holding’ pattern seen of late and wait for new ‘higher high’ or ‘lower low’ to be recorded.

The Japanese 10 year bond yield recorded the most notable drop from 0.46% to 0.38%.

The most action was seen in Commodities as it had the active week in some time.

Coffee, Cocoa, Cattle, Middle East Urea and Hot Rolled Coil Steel are no longer sporting overbought tendencies.

Sugar’s 6 week rally has now amounted to a 27.5% return.

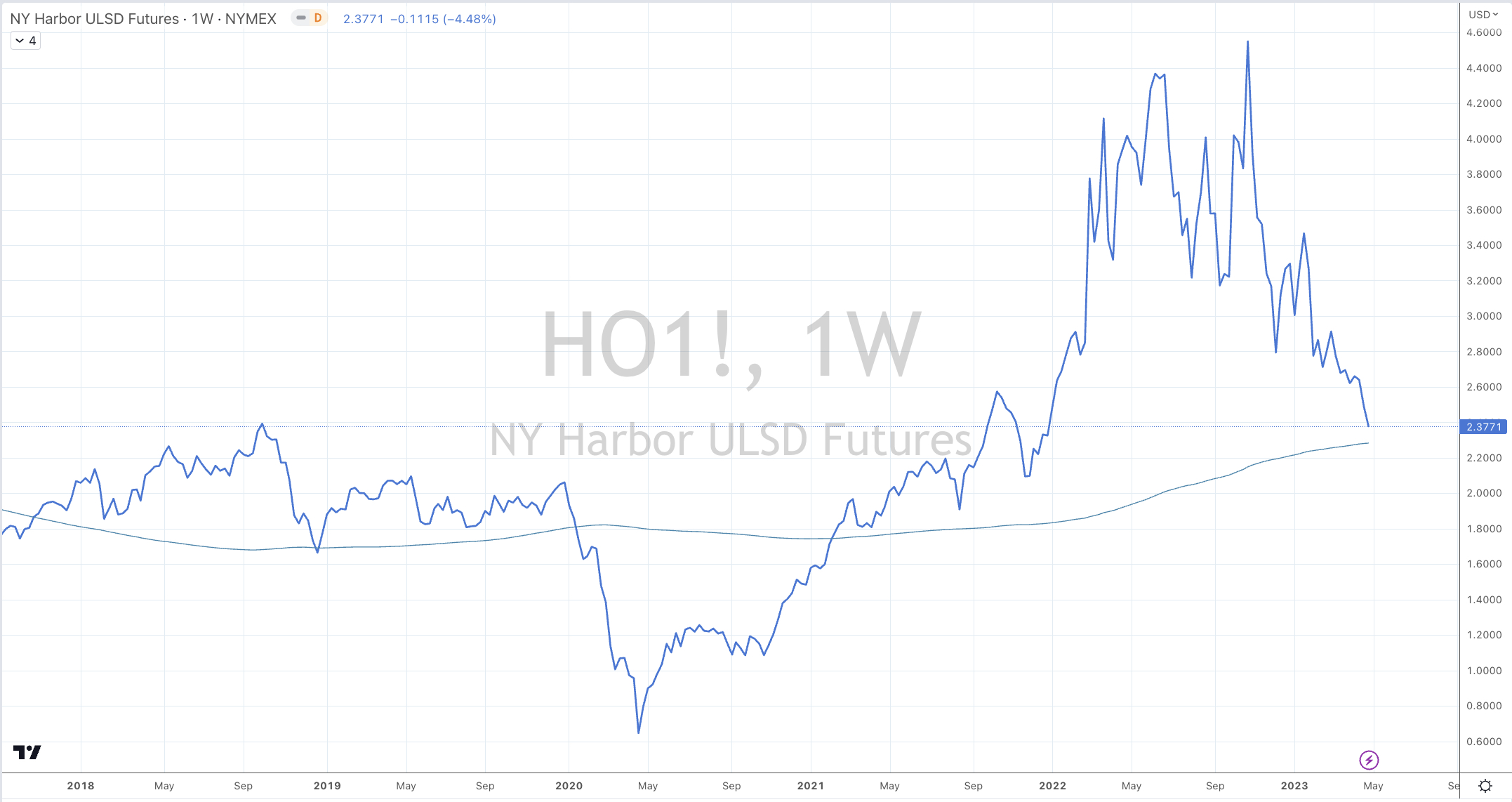

In fact, the streaks amongst commodity prices have returned. Heating Oil has declined for 5 consecutive 5 weeks, Lithium has sunken for 9 weeks, Australian Coking Coal is in a 5 week downward streak (9 of its past 10 have been negative) while the EUR/USD is in its 9th rising week.

We saw a continuation of last week’s weakness in energy, copper and soybeans with more agricultural (corn and wheat) joining the declines.

Other observations include, Gasoil (diesel) and Heating Oil are 3% from reaching a long awaited men reversion to its 200 week moving average and Copper broke below a support line.

The run in the PGM’s (platinum and palladium) took a breath this past week with the former breaking its 6 week rising streak.

Australian Coking Coal joined the oversold ranks having now seen a 39% decline over the past 5 weeks whilst also mean reverting back to its 200 week moving average.

Corn’s nearest contract fell 12% this past week while the next contract month fell 14%. The pertinent reason for mentioning the subsequent month’s contract this week, is that it registered quinella of oversold readings and it also mean reverted to its 200 week moving average.

And Lumber has closed at its lowest level since mid-May 2020.

Remember all those stories about rising timber prices affecting homebuilding costs?

Euro strength dominated action amongst currencies.

The AUD was weak against most and many currencies which prompts me to say Australian assets are on sale against the GBP and EUR.

While the BRL/USD takes break from trading at an extreme, it continued to strengthen and we also saw the Danish Krone trade into overbought territory against the USD.

The larger advancers over the past week comprised of;

Baltic Dry Index 4.8%, Lean Hogs 3.4%, Natural Gas 7.9%, Sugar 6.1%, Urea (U.S. Gulf) 3.2%, Urea (Middle East) 9%, Gold in AUD 1.5%, Nasdaq 100 1.9%, Sensex 2.4%, Mexico 1.8%, Chile’s Santiago equity index rose 3.6%.

The group of decliners included;

Australian Coking Coal (13.7%), Rotterdam Coal (2.1%), Brent Crude (1.4%), Copper (2.3%), Heating Oil (4.5%), Hot Rolled Coil Steel (9.3%), JKM LNG Gas (2.8%), Coffee (2.9%), Lumber (11.6%), Cattle (4.9%), Lithium (6.6%), Tin (5.7%), Nikkei (5%), Palladium (6.1%), Platinum (4.3%), Gasoline (2.8%), S&P GSCI (1.6%), Dutch TTF Gas (4.1%), Corn (11.8%), Oats (6.5%), Soybeans (2.1%), Wheat (5.8%), KBW Bank Index (2%), DJ Transports (2.7%), MIB (2.4%), IBEX (1.9%), KOSPI (1.7%), Nasdaq Biotech Index (2%) and Thailand’s SET Index fell 1.9%.

April 30, 2023

by Rob Zdravevski

rob@karriasset.com.au