Sowing too many Oats

July 13, 2022 Leave a comment

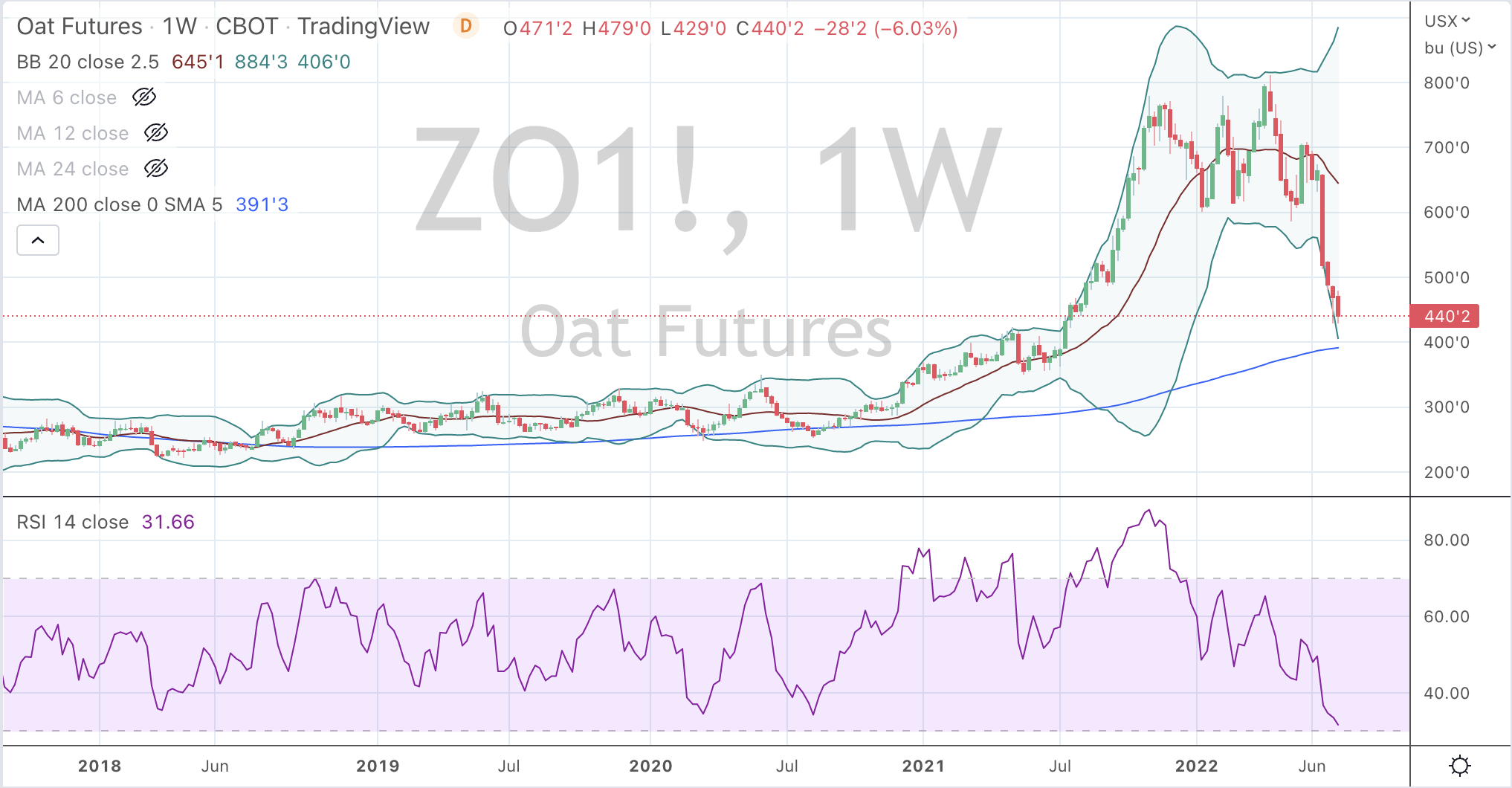

This weekly price chart of Oats tells me its set up is looking good for a low around the $3.94 mark in the coming 2-3 weeks.

A further decline of 10% is sympathetic to the trajectory of other ‘softs’ such as Rice, Wheat, Corn and Soybeans.

I think Cotton and Coffee have substantially more to downside than others. More on that in a future note.

The price of Oats nearly trebled through 2020- 2021 and then stayed elevated for 6 months.

However, this is a story about;

- not chasing prices which are at extreme percentages above whatever mean you choose to obey;

- observing euphoria and not running with the herd;

- if you did, take the ‘fat part of the trade’ and;

- allow for the probability of mean reversion.

Furthermore, farmers would have been well advised that an extreme run in price is often short-lived before considering crop rotation,

as would have buyers of agricultural land.

It was a sellers market.

When we combine an increase in inventories and higher fertiliser prices amidst a mid-cycle slowdown, prices are now declining towards the other end of the pendulum.

Canada is the world’s largest exporter of Oats, Russia is the largest grower whilst the U.S. and Germany account for 50% of the global Oats import market. Oats yield 50% more per acre than Wheat.

Lower Oats prices will benefit the likes of Kelloggs, Hain Celestial & Nestle.

Those ‘middle-men’ who have built up inventories will soon (next 6 months) be seen selling at a discount or loss.

It will soon be a buyers market.

July 13, 2022

by Rob Zdravevski

rob@karriasset.com.au