Macro Extremes (week ending May 21, 2021)

May 23, 2021 Leave a comment

The following assets (on a weekly timeframe) registered an Overbought reading or traded more than 2.5 standard deviations above its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

Italian Government 10 Year Bond Yields (4th consecutive week)

Zinc (although it closed 5% below its intra-week high)

GBP/USD (indicating a strong British Pound against the U.S. Dollar)

Overbought (RSI > 70)

French & Korean Government 10 year bond yields (3rd consecutive week)

German and Canadian 10 year bond yields (for the 2nd consecutive week)

The Commodities Indices (the CRB and Bloomberg’s)

Tin (for the 4th week)

Iron Ore (in its 7th overbought week)

Lean Hogs (for the 13th consecutive week and its highest price since July 2014)

U.S. KBW Banking Index (12th consecutive week)

Dow Jones Transport Index (11th consecutive week)

France’s CAC-40 Equity Index (for the 6th consecutive week) and

Spain’s IBEX (2nd week in)

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Canadian Dollar / USD (4th consecutive week of the quinella, where the CAD is exhibiting strength against the U.S. Dollar)

Assets (securities) within my immediate universe which touched the other side of the extreme, being Oversold (where the RSI is < 30) or were at least 2.5 standard deviations below its mean are;

Extremes “below” the Mean (at least 2.5 standard deviations)

Nil

Oversold (RSI < 30)

Nil

The Oversold Quinella – Both Oversold and Traded at < 2.5 standard deviations above the weekly mean)

Nil

Notes & Ideas:

The most notable price action over the past week saw more aggressive purchasing of government bonds (resulting in yields easing lower) and a decline in many commodity prices (such as Lumber, Sugar, Coffee and Corn) as they continue their reversion from their recent Overbought Extremes and in some cases, parabolic moves.

Specific moves include;

a 4.5% decline in Platinum and Wheat (adding to the latter’s 7% fall in the previous week),

while Brent Crude, Aluminium, Copper, Soybeans, Heating Oil and Gasoline all retreated 3.5% for the week,

It was a week where Copper & Aluminium ended 6 and 12 week respective overbought streaks while Gasoline is now 7% below its previous week’s high as bullish trades chasing high on news of the Colonial Pipeline cyber security attack proved to be a trap.

and the Nasdaq Transportation Index declined (after 9th consecutive weeks) while the Dow Jones Transports continues its Overbought streak.

While many western government bonds were being sold (resulting in rising yields), the Chinese Government 10 year bond yields are nearing an Oversold extreme, meaning the world’s 2nd largest bond market is attracting a bid. After all, only 3% of its is foreign-owned.

The major bond market yield I am watching continues to be U.S. 10 year yield and whether it breaks above 1.75%. It closed the week at 1.62%.

The Russell 2000 seems to be in the early stage of a new downtrend. Today’s price of 2,215 is 6% below its March 15, 2021 high of 2,360 and I continue to watch a similar setup for the MidCap 400.

We aren’t seeing the Dow Jones Industrials (DJI) and S&P 500 in the overbought realm, more so because the DJI’s prior week’s bearish outside reversal week is important to watch.

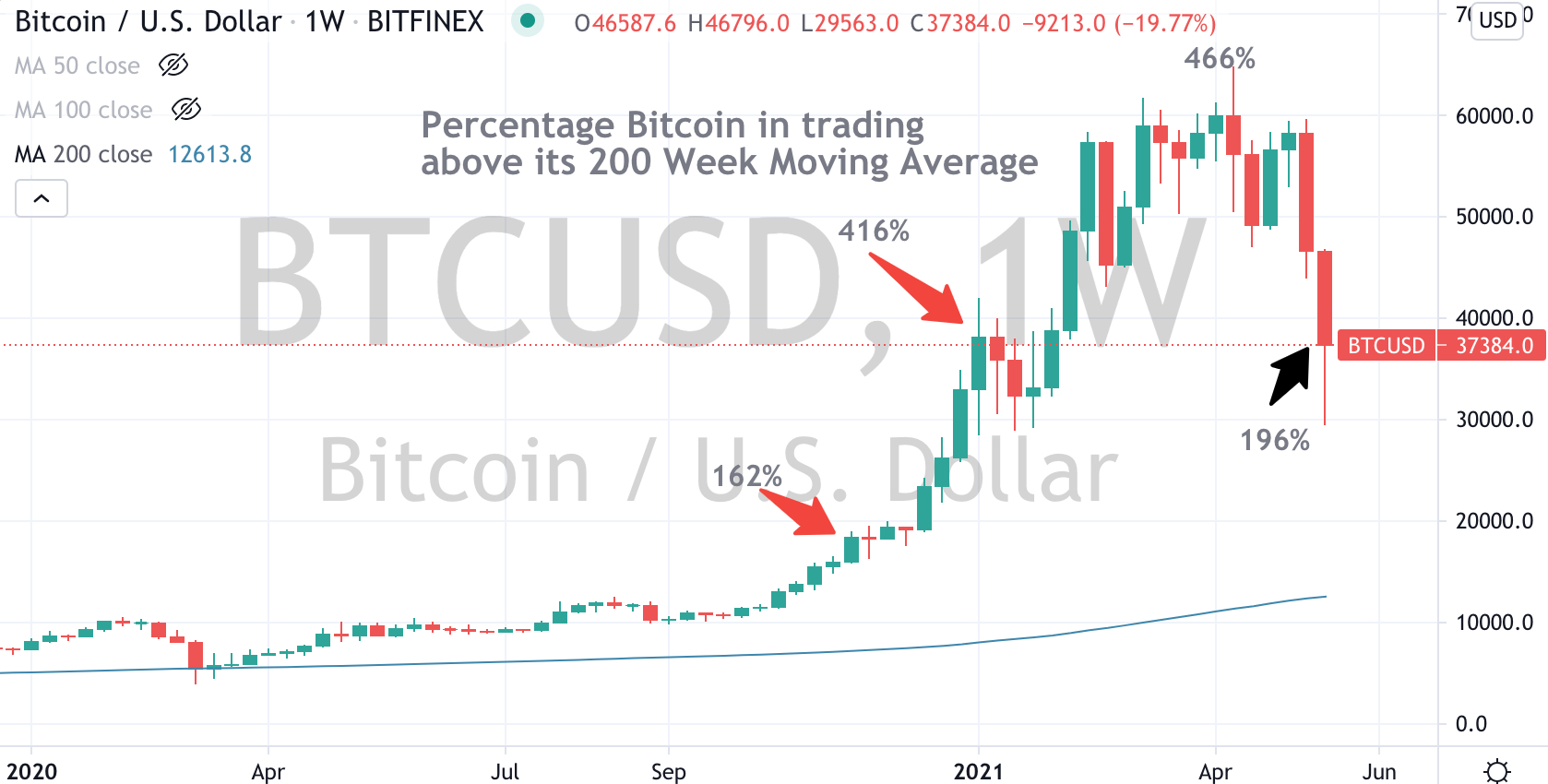

And lastly, it wouldn’t be a Macro Extreme post if I didn’t mention Ethereum’s 36% collapse during the week and Bitcoin’s 20% decline adding to the previous week’s 20% fall.

Bitcoin is now only trading 196% above its 200 week moving average compared to its 466% peak in mid-April 2021

p.s. no cryptocurrencies are Oversold yet.

May 23, 2021

by Rob Zdravevski

rob@karriasset.com.au