More on British inflation

April 17, 2024 Leave a comment

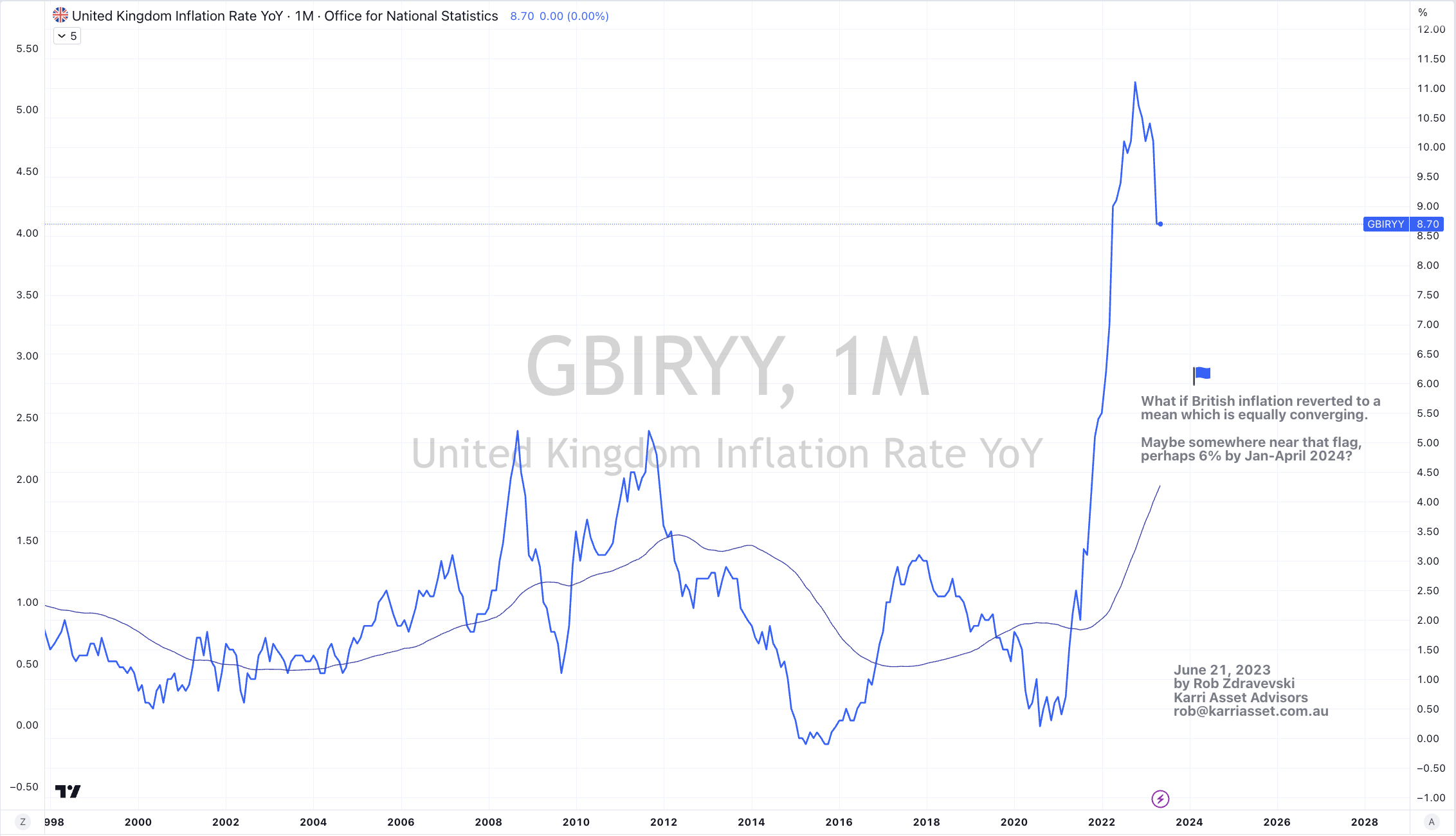

I am posturing for higher #inflation rates, again.

My expectations (found in my historical posts) for ‘lower’ inflation has occurred and is as good as being completed.

Following up my note dated April 11, 2024, suggesting the irrelevance of the U.K. March inflation report,

While inflation has abated, now it doesn’t matter so much whether this month’s #UnitedKingdom inflation rate of 3.2% is lower than last months (year on year) figure of 3.4%.

Keep in mind, that prices are still rising and I think that is mostly a cause of capacity and supply constraints rather than notable demand.

My thinking is that #UK inflation will move to 5% rather than 2%.

Slowing demand means companies will increases prices for goods and services, in order to maintain their shrinking margins.

April 17, 2024

by Rob Zdravevski

rob@karriasset.com.au