Venezuela is the largest holder (18%) of the world’s proven oil reserves. If we discount any government inflated figures and the difficulty and costliness of extracting from the Orinoco Belt, let’s agree that they may come in slightly lower than Saudi Arabia.

Although, this comparison is between one country to another. It is worthy to note that Middle Eastern countries collectively hold 48% of these reserves.

Recently, it has been reported that Venezuela may default on its debt sometime in 2013. I don’t believe they will, but they will create tensions and ransoms surrounding such a possibility.

They will simply produce more oil receipts to service or extinguish their debt. The IEA, OPEC and Saudi’s have also said that they would like to see oil prices lower than their present levels.

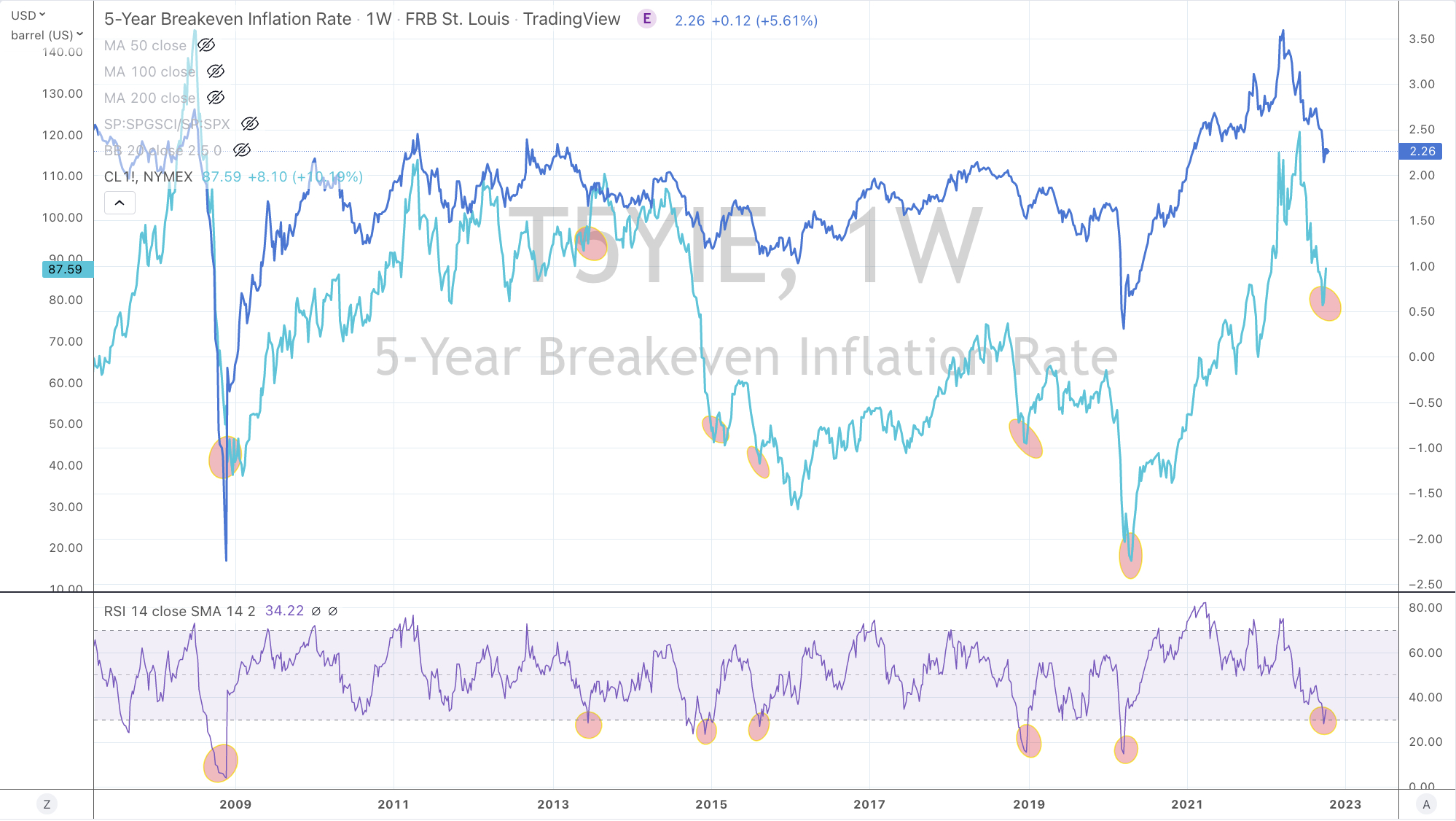

Recently, it seems that the oil price has been supported by speculation or anticipation surrounding geopolitical tensions and probabilities.

Israel’s equally hostile reaction to Iran’s previous threats has bid up the oil price of late along with populous Arab uprisings, although geopolitically, it would be wise for Israel to seek counsel from the United States before any pre-emptive missile attacks.

Although Iran would prefer a better scenario, but covertly they would welcome higher oil prices as it would ease the fiscal pain associated with new rounds of sanctions while Venezuela needs higher prices to make their tar, economically viable.

Much of America’s foreign policy is oil based and higher oil prices wouldn’t help America’s economic plight. Look for more diplomatic focus towards South America and the former Soviet Republics.

The fundamental case for lower oil prices includes a subdued global economy, cheap coal and abundant gas (shale or otherwise) and record levels of oil production capacity will help keep the price of oil low.

Furthermore, there is so much oil in the world, we are not close to a “peak oil” scenario. In fact, the value of the world’s proven reserves amounts to at least $150 trillion, which is more than the combined value of all of the worlds gold, bank deposits, government debt and the market capitalisation of the worlds listed companies.

Yossie Hollander’s TED Talk summarised it well. There is not enough money in the world to buy all of the world’s oil, thus oil is too expensive.

When investing, you should avoid owning an asset where there is excess supply for I would prefer owning an asset that is in demand but in short supply.