What a contrast.

Generally, retail investors didn’t seem too interested buying equities in September or October 2012. After all, with all of the world’s looming problems….

Today, anecdotally, investors are chasing stocks at higher prices even after seeing an advance of approximiate 13% in many indices and individual stocks.

Why do investors feel more comfortable buying when prices are much higher?

Is is because there is less risk in equity markets today?

Are they “technical” traders and feel better buying on the “break-out”?

They feel more “comfortable” if the herd is doing the same?

Or perhaps they have a Fear Of Missing Out (FOMO)?

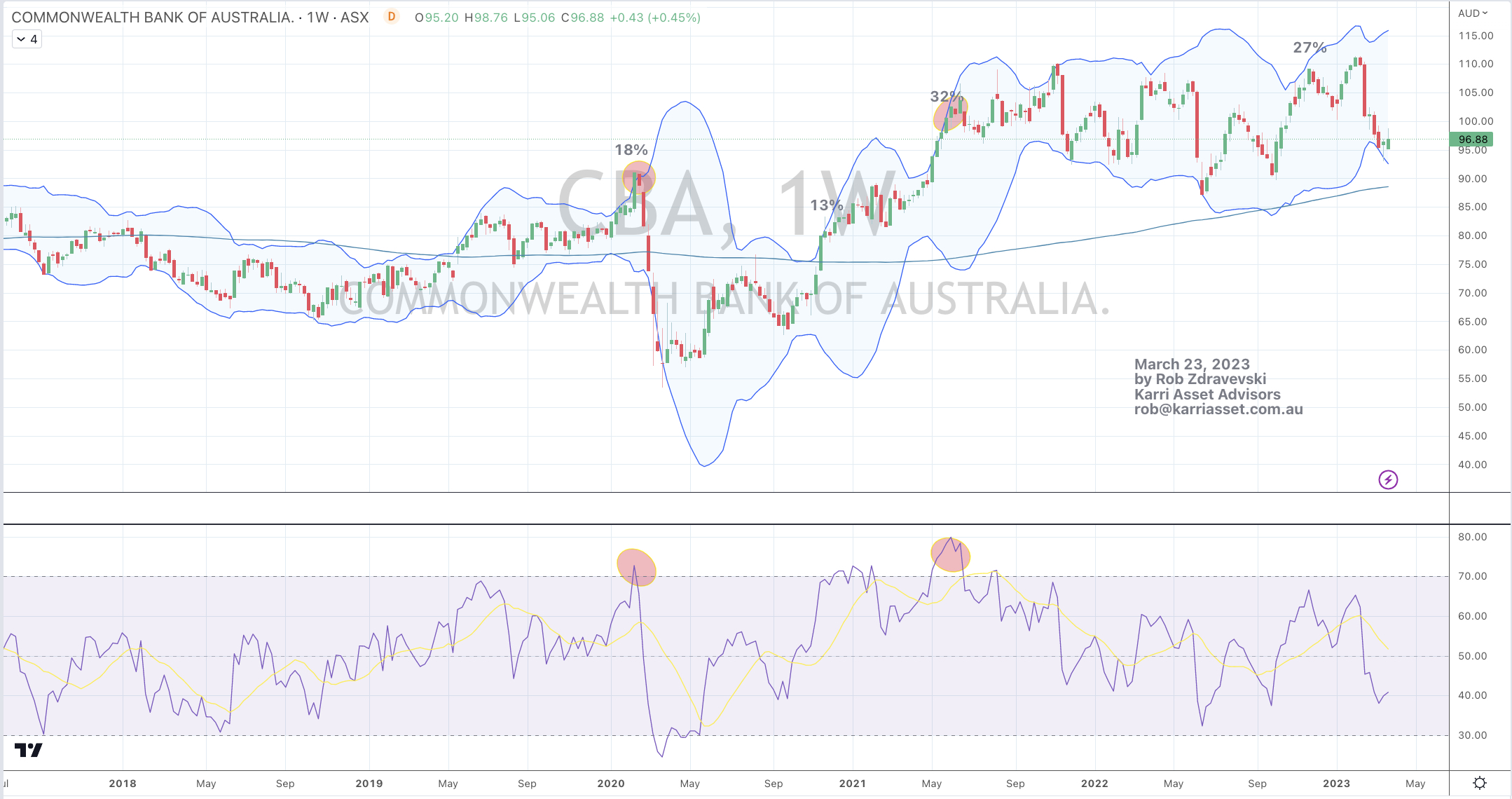

At the beginning of February 2013, the market capitalisation for Commonwealth Bank of Australia (CBA) nears that of Bank of America.

CBA has one-quarter of the revenues while domiciled in a country with one-fifth’s of Bank of America’s home turf. Hmm, not sure if this is deserved.

I think investors in Australia are not only worrying about the FOMO but also upset that they are “only” earning 3.5% on their cash savings.

They are starting to exhibit “needs-based investing”.

Ever heard of anyone being a “forced buyer”?

This is where an investor “needs” to invest because they feel aggrieved by their paltry bank interest returns.

Recently, I have had conversations with investors who wish to buy CBA’s stock (even though it has risen 14% in the past 3 months and 165% in past 4 years) because it’s paying a 7% dividend. They are happy to buy assets that present a headline dividend yield for the sake of yield alone, without any regard for any capital risk that they may be taking.

The sadness for Australians who only invest in Aussie shares, is that they have a lack of quality companies from which to populate their portfolios with.

This is not a post about CBA’s valuation but rather behaviour. I am encouraging retail investors to observe the biases that they may have when making decisions.

It seems every investor is armed with the same defence.

Many say, “I’ll only own blue-chips”. And they do, often without any regard for valuation, because if you call a stock “blue-chip”, then you are apparently safe and immune from losing any money.

If you’re an Australian whose equity portfolio only consists of domestic shares, ask your friends to describe their portfolio to you.

You should find that they will start by bragging about their “blue chips” and amazingly, you’ll probably own the same 12 stocks.

3 out of the 4 banks, BHP, Rio Tinto, Telstra, Wesfarmers, Woolworths (they’ll usually say something like “’cause everybody has to eat” after mentioning this one), Westfield, maybe an insurance company, some other sort of mining company that they think is blue-chip ’cause of the mining boom and CSL. Some investors still hold a pearler such as Qantas or Toll Holdings for they are confident that they will “come good” sooner or later.

Investing behaviour never ceases to amaze me.