Watching Currencies – AUD/JPY

September 5, 2022 Leave a comment

Correlations – AUD/JPY and the ASX 200 Index

September 5, 2022

by Rob Zdravevski

rob@karriasset.com.au

Trying to hear what's not being said

September 5, 2022 Leave a comment

Correlations – AUD/JPY and the ASX 200 Index

September 5, 2022

by Rob Zdravevski

rob@karriasset.com.au

September 5, 2022 Leave a comment

Correlations – AUD/JPY and the Australian Inflation Rate

September 5, 2022

by Rob Zdravevski

rob@karriasset.com.au

September 5, 2022 Leave a comment

Correlations – AUD/JPY and Australian 2 year government bond yield

September 5, 2022

by Rob Zdravevski

rob@karriasset.com.au

September 5, 2022 Leave a comment

Correlations – AUD/JPY and Crude Oil

September 5, 2022

by Rob Zdravevski

rob@karriasset.com.au

September 4, 2022 Leave a comment

The following assets (on a weekly timeframe) registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

None

Overbought (RSI > 70)

U.S. 2 year government bond yield

U.S. Dollar Index

Istanbul Stock Exchange (BIST)

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

U.K. 10 year government bond yields

Extremes “below” the Mean (at least 2.5 standard deviations)

NZD/AUD

CAD/USD

TLT

Oversold (RSI < 30)

U.S. 5 year minus U.S.3 month government bond yield ‘spread’

Turkish 10 year government bond yields

Hot Rolled Coiled Steel

Tin

EUR/USD

GBP/USD

CNH/USD

DKK/USD

KRW/USD

SEK/USD

JPY/USD

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

None

Notes & Ideas:

The big news over the past week saw a continuation of the decline in U.S. equities with the Philadelphia Semiconductor Index (SOX) standing out with a 7% swoon.

Government bond yields are approaching their next round of being overbought, as are Cattle prices.

U.K. 10 year bond yields are at their highest since July 2011.

The U.S. Dollar Index (DXY) is at its highest since September 2022.

Gold, Silver and Platinum are nearing buys,

as is the Baltic Dry Index.

The Shanghai Composite equity index, Copper and the U.S. KBW Banking Index has mean reverted and dipped to its 200 week moving average for the second time in as many months.

Following last week’s comments about surging gas prices, Dutch TTF Gas and Japan Korean LNG Marker price no longer overbought having tanked 38% and 20% for the week, respectively.

U.S. RBOB Gasoline prices continue to retrace. This week’s 8% decline means it has halved over the past 3 months,

While, Australian Coking Coal has risen 33% over the past 5 weeks.

The larger advancers over the past week comprised of;

Australian Coking Coal 11.2%, Orange Juice 6% and Istanbul’s BIST equity index rose 2%.

The group of decliners included;

Aluminium (8.5%), Rotterdam Coal(2%), Bloomberg Commodity Index (4.4%), China Coal (2%), WTI Crude (6.7%), Gasoil (8.6%), Copper (7.7%), Heating Oil (10.7%), HRC (1.8%), JKM (19.7%), (19.7%), Coffee (3.9%), Lumber (3.8%), Tin (6.2%), Natural Gas (5.2%), Nickel (2.2%), Palladium (4.5%), Platinum (4.3%), Gasoline (8%), Rubber (2.4%), Sugarm(1.7%), Silver (4.6%), CRB Index (4.9%), Cotton (11.2%), Dutch TTF (38.1%), Brent Crude (7.3%), Silver in AUD (3.3%), Silver (4.5%), Oats (5.7%), Soybeans (2.8%), AEX (3.8%), KBW Banks (2.5%), Dow Jones Industrials (2.8%), DJ Transports (4.5%), HSCEI (3.6%), HSI (3.6%), IBEX (1.6%), KOSPI (2.9%), S&P MidCap 400 (4.2%), Nasdaq 100 (4%), Nikkei (3.5%), Oslo (3%), Copenhagen (3.8%), Russell 2000 (4.7%), SOX (7.1%), S&P 500 (3.3%), Taiex (4%), FTSE (2%), S&P SmallCap 600 (5.2%), Nasdaq Composite (4.2%), Canada’s TSX (3%) and Australia’s ASX 200 declined (3.9%).

September 4, 2022

by Rob Zdravevski

rob@karriasset.com.au

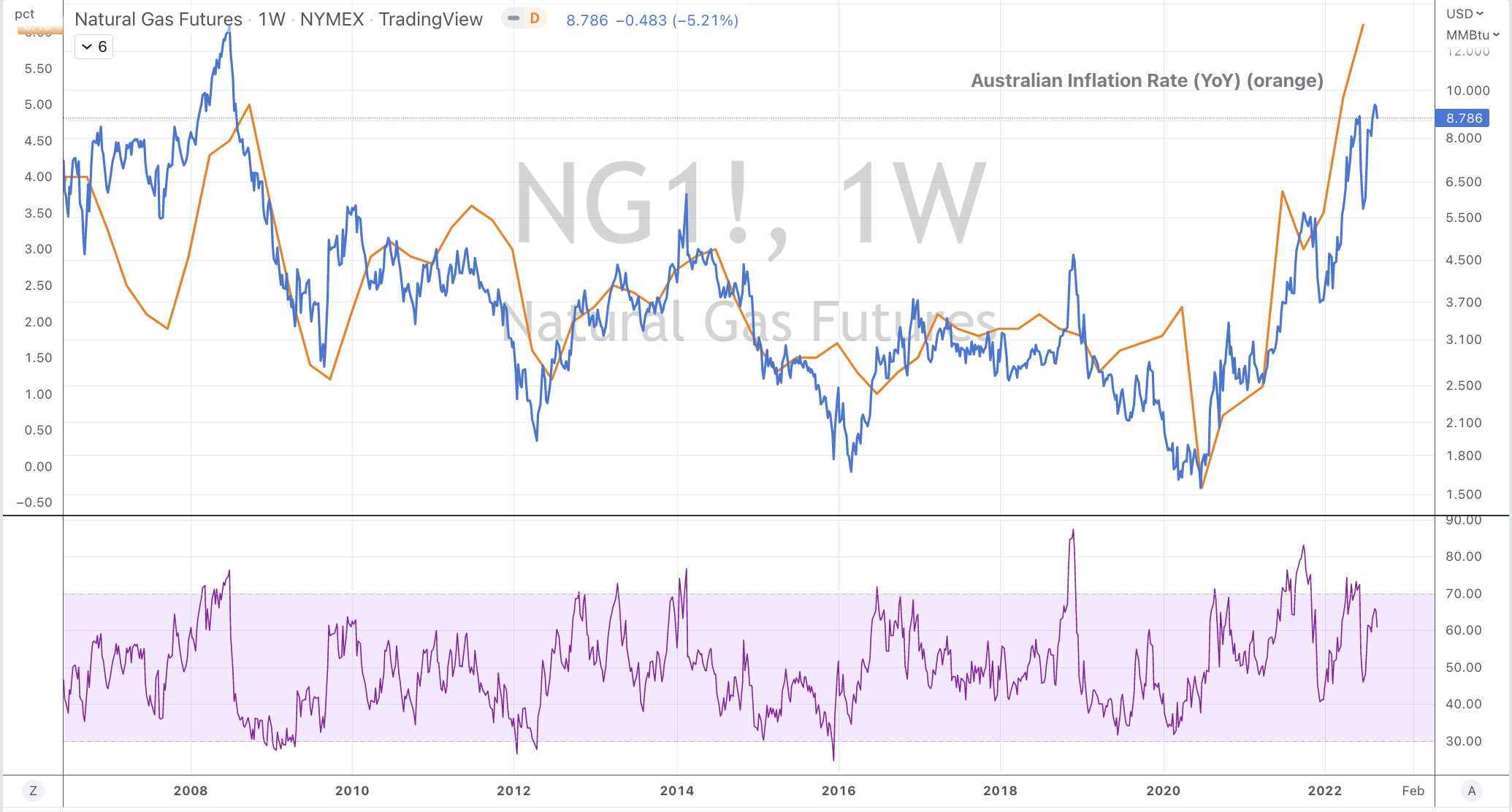

September 3, 2022 Leave a comment

As an addendum to last week’s note about elevated Natural Gas (US$ Henry Hub) prices,

here is a chart pitching those American gas prices against the Australian inflation rate, aiding my call for moderation.

September 3, 2022

by Rob Zdravevski

rob@karriasset.com.au

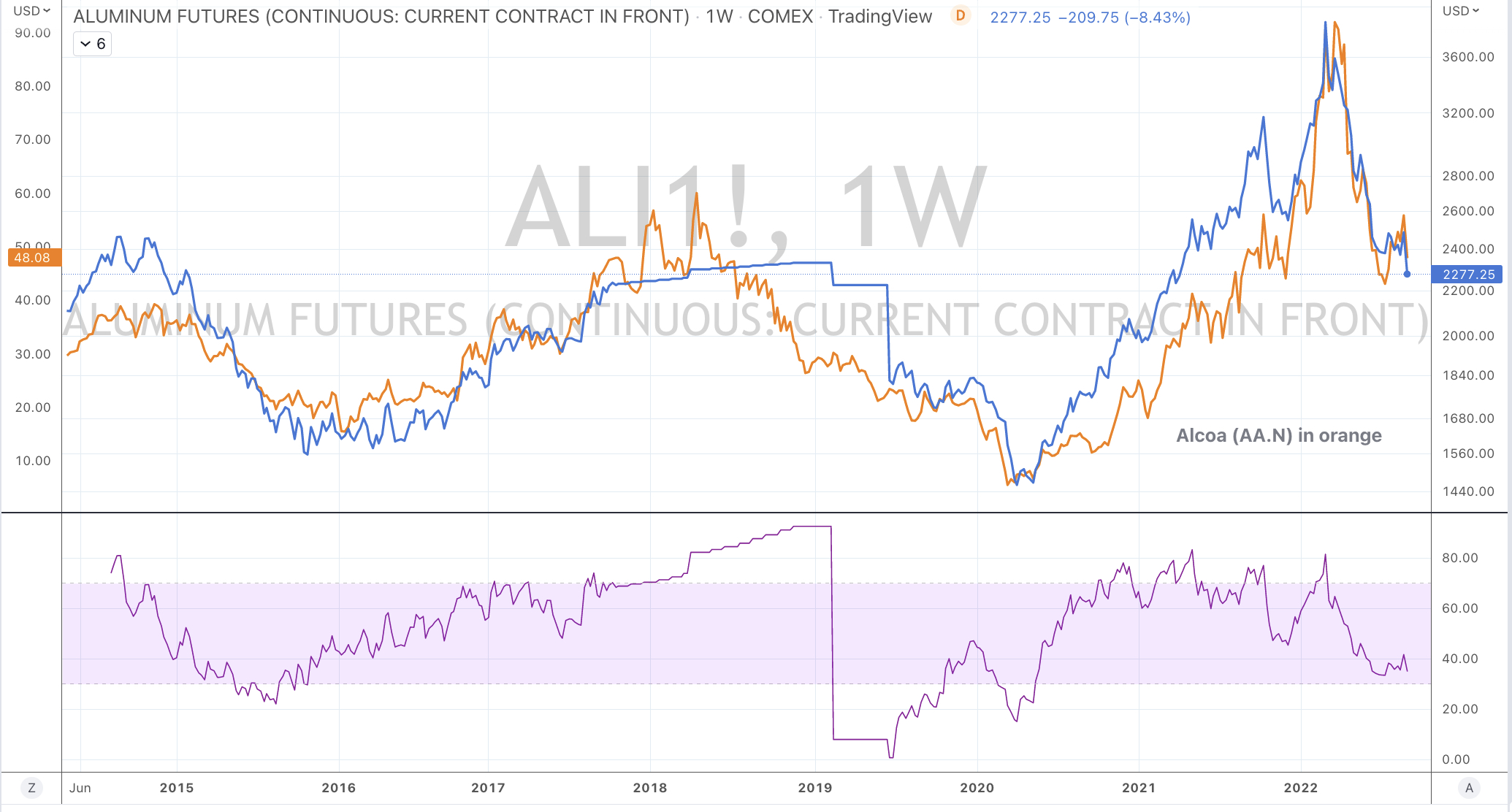

September 2, 2022 Leave a comment

Here is the price of Aluminium and Alcoa’s (AA.N) stock price waltzing around.

Observe the operational leverage the equity can provide if the company is executing well, when the underlying commodity is in an upward trend.

September 2, 2022

by Rob Zdravevski

rob@karriasset.com.au

September 2, 2022 Leave a comment

The Iron Ore futures (Singapore traded, 62%) price dances nicely along with the stock price of Rio Tinto (RIO.ASX)

September 2, 2022

by Rob Zdravevski

rob@karriasset.com.au

September 2, 2022 Leave a comment

I’m sharing a presentation which I spoke to this week.

The topic is contrarianism where I show long-term charts (on a weekly basis) and quantified extreme moments using three measures, being:

– the 200 week moving average

– the Relative Strength Indicator (signalling Overbought and Oversold readings) and

– Bollinger Bands showing when prices traded to 2.5 standard deviations (either above or below its rolling weekly mean)

I attempted to highlight the case for lower interest rates and inflation (as they are themselves trading at ‘extreme’ levels) by showing a host of correlations and I believe moderation is aided with further mean reversions amongst various prices, while many other commodities have already done so. As reported inflation figures lag, lower readings are expected to appear in the coming 4-10 months.

There is also a series of charts showing recent buying ‘windows’ and where I’m waiting for some others to enter my buying territory.

Towards the end of the presentation I touch on how a scramble to secure supply led to price spikes and parabolic price moves in commodities such as Lumber and Steel, where such parabolas were (and often) followed by sharp declines.

I think there is much finished product still held as inventory, thus tying up working capital and should lead to discounting wars. This will be deflationary and assist in abating inflation and interest rates.

To be clear, I’m calling for interest rates and inflation to abate, not collapse.

September 2, 2022

by Rob Zdravevski

rob@karriasset.com.au

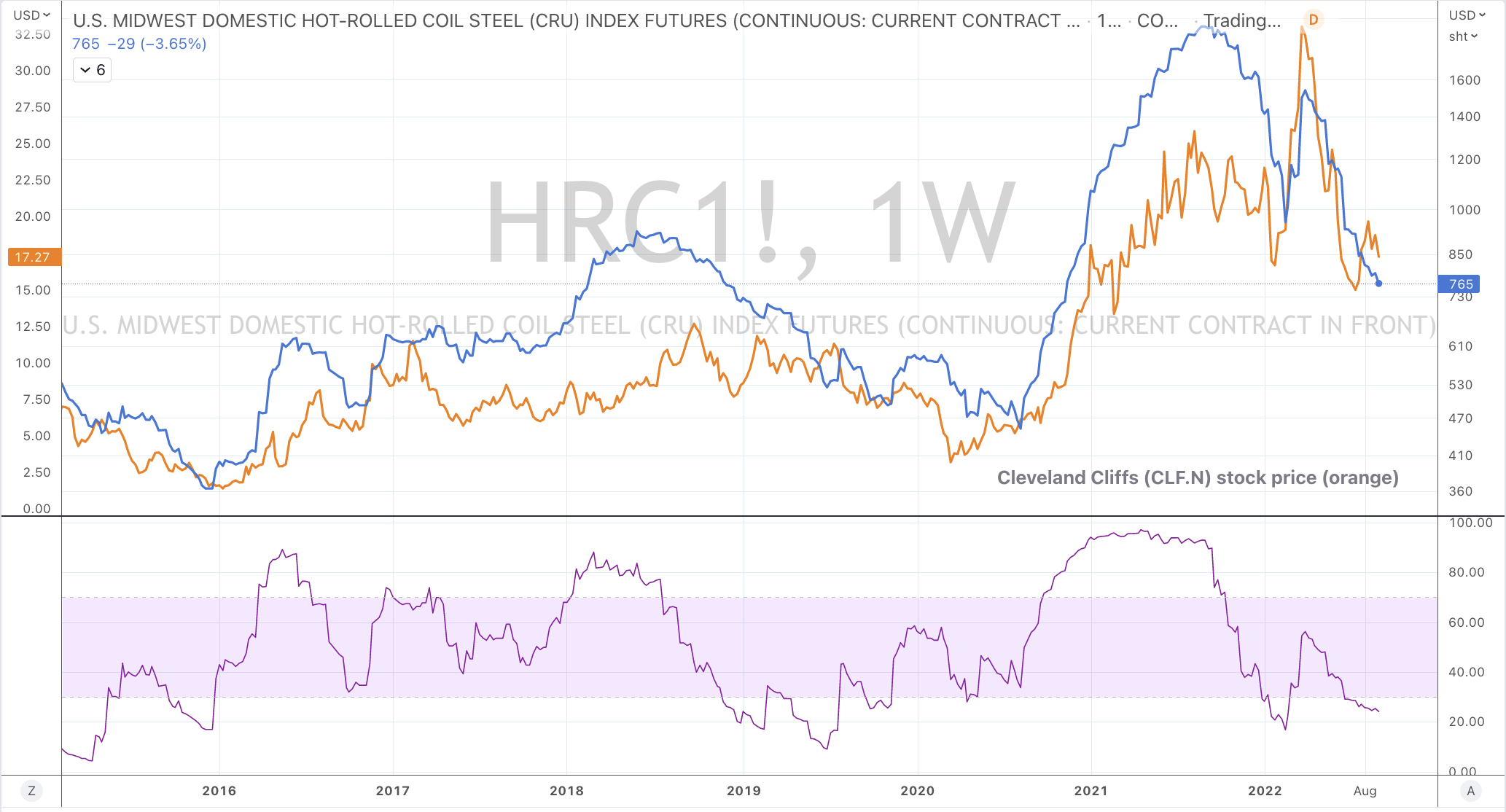

September 1, 2022 Leave a comment

Lows in U.S. Hot Rolled Coiled Steel prices are correlating with the stock prices of selected steel companies.

Cleveland Cliffs (CLF.N) is the featured comparison in the chart below.

September 1, 2022

by Rob Zdravevski

rob@karriasset.com.au