Macro Extremes (week ending September 29, 2023)

October 1, 2023 Leave a comment

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

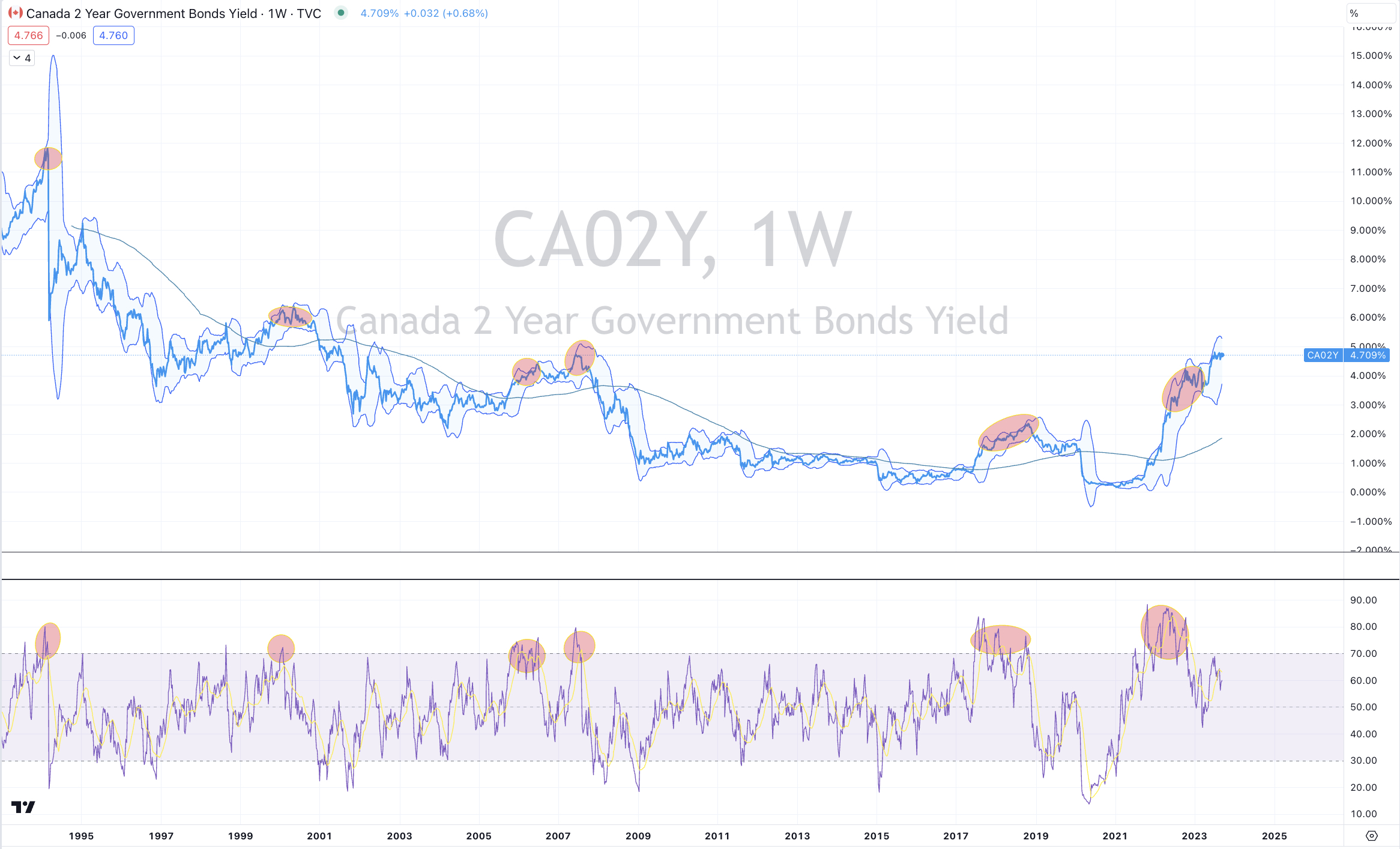

Australian, Brazilian, Italian, Canadian, Swiss, German, Spanish, Greek, French, Portuguese, Swedish and Turkish 10 year government bond yields

U.S. 5-7 year corporate bond yields

German 5 year government bond yields

Baltic Dry Index

CAD/EUR

CAD/GBP

CAD/EUR

Australian Coking Coal

CAD/GBP

Oslo’s equity index

Overbought (RSI > 70)

Japanese, Russian and New Zealand 10 year government bond yields

U.S. 3 month bill yields

U.S. 5 year bond yield minus 5 year inflation break-even rate

U.S. 10 year bond yield minus 10 year inflation break-even rate

Gasoil

USD/JPY

And Turkiye’s BIST 100

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Chilean 10 year government bond yield

U.S. 7, 10, 20 and 30 year government bond yields

TBT & TBX

Australian Coking Coal

China Coking Coal

Uranium

Extremes “below” the Mean (at least 2.5 standard deviations)

IEF & IEI

Nickel

Gold (in USD)

THB/USD

DAX Index

Nasdaq Biotechnology Index

Thailand’s SET Index

ASX Small Cap Index

And ASX Industrials Index

Oversold (RSI < 30)

U.S. Mid West Hot Rolled Coil Steel

Lithium Hydroxide

Orange Juice

JPY/USD

The Oversold Quinella – Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

TLT

Notes & Ideas:

Government bond yields rose again with my most notable news being the return of bond yields towards the upper end of their ‘extremes’.

However, while highs over recent times are now being made, the past several weeks sees many global government bond yields yet to break the previous major cycle highs of 2007 and 2011.

Note those U.S. yields which appear in the ‘quinella’ section of this week’s list.

Equity indices continued their general weakness with most of them ending the week either up or down 0.6% from last week’s close.

The Philadelphia Semiconductor Index bounced 2% following a 9% decline over the previous 3 weeks.

Most U.S. bourses held up, for example the S&P 500 rose 0.7% while most Asian bourses fell, reversing last week’s action.

Furthermore, the KOSPI has fallen 5.2% in the past 2 weeks.

Commodities were mixed with the list of winners and losers showing those who closed 1.8% in either direction from last week’s week ending prices.

Gold and Silver had a terrible week.

Gas prices has a good week. In fact, Dutch TTF Gas has now doubled since its oversold moment in late May 2023.

The Baltic Dry Index has soared 51% in the past 4 weeks and is now overbought while Gasoil is the first of the energy contracts to return to the territory.

Whilst Cattle isn’t overbought anymore.

Nickel has mean reverted having nearly halved from its December 2022 overbought reading and closing in on oversold territory.

Uranium is overbought for its 7th consecutive week along with having the highest overbought reading since 2011.

Cocoa has declined 9% in the past 2 weeks after spending some time in overbought land.

Orange Juice closed at another new all-time high.

Sugar broke its 5 week winning streak.

U.S. Mid West Hot Rolled Coiled Steel has been oversold for 5 weeks.

Soybeans have declined for 5 consecutive weeks, while Lithium Hydroxide declining streak extends to 12 consecutive weeks.

And Australian Coking Coal and Uranium have their 12 week winning streak intact and registering an overbought quinella.

Amongst currencies, the Australian Dollar and the Canadian Dollar were generally firmer this week, again.

The AUD is in a 5 week consecutive week advance versus the Thai Baht.

The Canadian Loonie is on a 6 week winning streak vs. the EUR and entered overbought territory during the week against it and the British Pound.

The USD was stronger except against the SEK.

The DXY extends its rising streak to 11 weeks and that is the case specifically for USD/DKK.

The GBP/USD is in a 6 week losing streak and has fallen in 9 of its past 11 weeks.

And the EUR was mixed, while the EUR/USD is in a 11 week losing streak.

The larger advancers over the past week comprised of;

Australian Coking Coal 9.7%, Aluminium 5.2%, Rotterdam Coal 4.7%, Baltic Dry Index 6.8%, China Coking Coal 9.7%, Gasoil 1.9%, Lumber 3.9%, Natural Gas 11.1%, Orange Juice 2.4%, Dutch TTF Gas 5.2%, Urea Middle East 6.7%, Uranium 5.8%, Oats 1.8%, MOEX 2.8%, BIST 3.8%, SOX 2.1% and KRE Regional Bank Index rose 1.5%.

The group of decliners included;

Cocoa (4.6%), Coffee (3.3%), JKM LNG (5.6%), Lithium Hydroxide (7.7%), Nickel (2.9%), Platinum (2%), Gasoline (4.5%), Sugar (1.8%), Urea Gulf (3.2%), Silver in AUD and USD (5.7%), Gold in AUD (3.9%), Gold in CAD (3.3%), Gold in USD (4%), Soybeans (1.6%), Wheat (6.6%), China A50 (1.8%), HSCEOI (1.8%), KLSE (1.8%), KOSPI (1.7%), Nikkei 225 (1.7%) and Thailand’s SET fell 3.4%.

October 1, 2023

by Rob Zdravevski

rob@karriasset.com.au