A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

Rubber

Overbought (RSI > 70)

U.S. 3 month bill yields

Russian 10 year bond yields

Cocoa

MOEX

And Turkiye’s BIST 100

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Uranium

Extremes “below” the Mean (at least 2.5 standard deviations)

None

Oversold (RSI < 30)

U.S. Mid West Hot Rolled Coil Steel

The Oversold Quinella – Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

Lithium

Notes & Ideas:

The government bond yields which appeared in the overbought list last week are no longer there as yields fell everywhere.

Chinese 10 year bond yields were the exception, for they rose and moved out of Oversold territory.

More interestingly, the U.S. 2 year bond yield posted an outside bearish reversal week.

All Equity indices were higher this week with many of them posting gains somewhere between1.4% to 1.6%, while the lost below features the over-achievers.

Copenhagen and Chile were the only two markets to decline for the week with the latter in a 5 week losing streak.

Last week’s losers (Chinese and U.S. banks) are this amongst this week’s winners and the Shanghai Composite & Hang Seng aren’t oversold this week.

While the Nasdaq Composite has climbed 5.5% over the past fortnight.

Commodities were mixed although rising metals and oil prices tipped the scales into the positive for the broader indices.

Amongst the energy sector, we saw Crude Oil, Gas and Coal prices rise while Gasoline, Distillates and Heating Oil fell. The latter giving up all of last weeks gain.

Over the past 2 weeks, Sugar, Aluminium, Platinum have risen 9%, 7% and 6% respectively, while Wheat has fallen 7% over the same time.

LNG and Oats aren’t overbought this week although Rubber entered this region for the first time in 16 months following its 16% rise over the past 3 weeks.

Uranium and Australian Coking Coal are in 8 week winning streaks. Iron Ore’s rising streak completes its 5th week while Heating Oil broke its 9 week consecutive climb.

Inversely, Lithium Hydroxide prices are in a 9 week losing streak while Middle East Urea prices have fallen for 5 consecutive weeks.

Cocoa is overbought again amidst a stellar 60% advance since late September 2022.

And U.S. Midwest Hot Rolled Coil Steel prices fell 10% and are now Oversold.

In currencies, the AUD rose and broke various declining streaks include that against the USD.

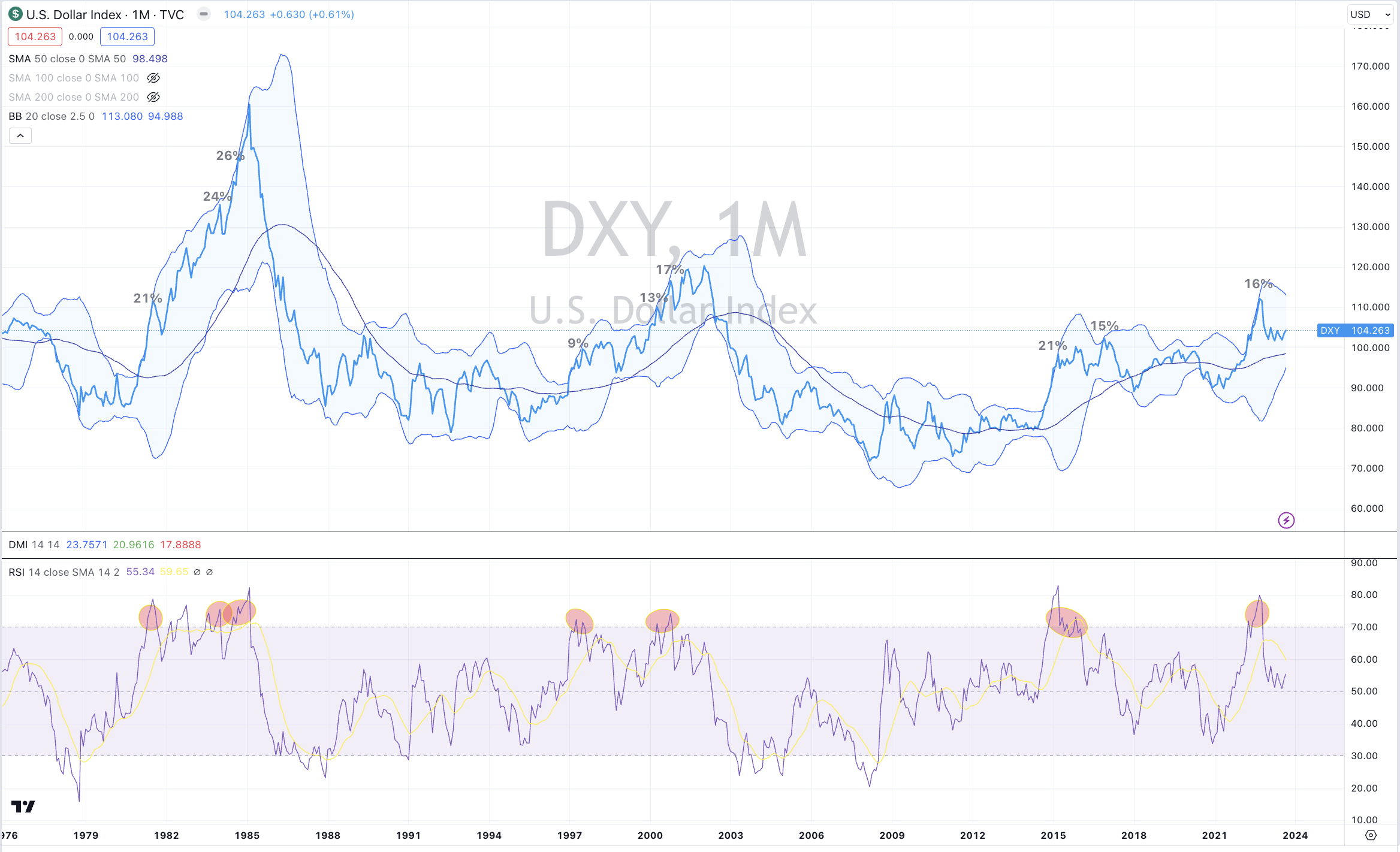

In turn, the USD was generally higher, seeing the DXY Index extend a 7 week winning streak.

The same streak exists in the USD/DKK with the exception of the USD/CAD which broke its 5 week winning run.

CHF/AUD which featured in recent posts isn’t overbought this week.

Overall, the EUR weakened. Specifically, the EUR/USD pair is in a 7 week losing streak now trading at 1.07. Before this move, it was 1.12.

The GBP was flat while the JPY/GBP moved out of Oversold territory.

The larger advancers over the past week comprised of;

Australian Coking Coal 6%, Aluminium 4.7%, Cocoa 4%, China Coking Coal 5.8%, WTI Crude 7.5%, Cotton 3%, Iron Ore 1.8%, Lean Hogs 4.3%, Copper 2.3%, Newcastle Coal 14.7%, Natural Gas 8.9%, Platinum 2.2%, Sugar 4%, S&P GSCI 2.4%, Rubber 3.5%, CRB Index 2.2%, Dutch TTF Gas 2.4%, Brent Crude 5.7%, Uranium 3.9%, Corn 2.3%, Rice 3.3%, Shanghai 2.3%, CSI 300 2.2%, AEX 1.7%, KBW Bank Index 2.9%, DJ Industrials 1.6%, HSCEI 2.5%, Hang Seng 2.4%, Bovespa 1.8%, MOEX 2.3%, Nasdaq Composite 3.3%, Kospi 1.8%, S&P 500 2.5%, TSX 3.6%, ASX 200 2.3%, KRE Regional Banks 4.6%, S&P SmallCap 600 3.5%, BIST 4.4%, FTSE 250 2.2%, ASX Materials 3.2%, ASX Industrials 2%, S&P MidCap 400 3.6%, Nasdaq 100 3.7%, Nikkei 225 3.4%, Oslo 2.8%, Helsinki 3.7%, Stockholm 1.8%, Russell 3.6% and the Philadelphia Semiconductor (SOX) Index soared 5.4%.

The group of decliners included;

Rotterdam Coal (4.7%), Gasohol (2.8%), Heating Oil (5.8%), Hot Rolled Coil Steel (10.6%), Lumber 2.4%, LNG in Yen (6%), Lithium (146%), Tin (3.1%), Gasoline (2%), Urea U.S. Gulf (6.2%), Urea Middle East (9.9%), Oats (2.9%) and Wheat fell 4.2%.

September 3, 2023

by Rob Zdravevski

rob@karriasset.com.au