Amidst the negative undertones within this The Australian Financial Review article, the is a luxury of being privately held and able to shutter an unprofitable mine. Many others are ‘forced’ to proceed and produce with the unfeasible because the market and shareholders expect them to.

It’s more concerning for those mining companies who are in the pre-capex dreams of becoming producers.

p.s. since when did a credit ratings agency start providing commodity pricing forecasts?

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations

KLSE – the Kuala Lumper Stock Exchange

Nikkei 225

Overbought (RSI > 70)

Cocoa

Uranium

Dow Jones Industrial Average

Nasdaq 100

Philadelphia’s Semiconductor Index

And India’s NIFTY equity index

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

None

Extremes “below” the Mean (at least 2.5 standard deviations)

USD/INR

Hang Seng China Enterprises Index (HSCEI)

Hang Seng (HSI)

Oversold (RSI < 30)

China 10 year government bond yields

Nickel on India’s MCX Exchange

Nickel on LME

Lithium Hydroxide

JKM LNG

CSI 300

The Oversold Quinella – Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

Soybeans

Corn

Shanghai Composite equity index

Notes & Ideas:

Government bond yields rose for the week, in back and forth weekly action over the past month, although yields are painting a picture of either consolidating the decline in yields seen since October 2023 or recovering part of the fade.

They have all bounced from their oversold extremes seen 4-6 weeks ago.

The only bond market to see yields fall was China’s 10 year paper.

Equities saw a 2-speed environment.

Most global equity indices saw weakness while the ‘larger’ U.S. indices continued their rise.

For example, the Nasdaq has risen 5.5% over the past 2 weeks, although it did fall 3.1% in the week prior to the most immediate fortnight.

The smaller U.S indices didn’t see the aforementioned strength. The banking and small cap indices were flat while the Russell 2000 was down 0.4% and the MidCaps were up 0.4%.

However, some indices are now trading at stretched levels above their 200 week moving average.

The SOX (closed at its all-time high) is 46% above it, while the Nasdaq 100, the Nikkei 225 and the Nasdaq Composite are 31%, 29.5% and 21% respectively above that measure.

Incidentally, the S&P 500 is trading at 20% above its 200 week moving average and we may start to see money shifting and broadening to the Small and Mid Caps, the further that percentage spread rises.

Taiwan’s TAEIX rose 1% following an election return of the incumbent political party.

On the other side of the ledger, most European markets fell, lead by the Nordics but also including the 1% declines in the DAX and the CAC.

This week saw the Hang Seng and the HSCEI close at their lowest levels since October 24, 2022, while some mainland China markets were mute.

The CSI 300 fell 0.4% while the China A50 rose 0.6%.

India’s SENSEX fell 1.2% and isn’t overbought this week.

Copenhagen snaps its 10 week winning streak and the Nasdaq Biotechnology Index has broken its run of 9 consecutive weekly gains.

The Dow Jones Index had a bullish outside reversal week while Indonesia (snapping its 5 week winning streak) and India’s NIFTY performed outside bearish reversals.

Chile’s main index has fallen 5.3% over the past 3 weeks, yet still remains 21% above its 200 week moving average suggesting a reasonable probability that mean reversion (convergence) lays ahead.

The ASX Materials Index has sunk 9% in the past fortnight and the Hang Seng China Enterprises Index (HSCEI) has tanked 11.5% over the same time. The latter now appears in this week’s oversold category.

And Brazil’s BOVESPA has declined 5% over the past 3 weeks. 4 weeks ago, it was overbought.

Commodities were mixed.

The notable movers either side of the ledger broadly offset the week ending results for the various commodity indices.

Large advances were seen in Sugar, Cocoa & Cotton which saw advances compound to 11.5%, 9%, 4.5% respectively over the past fortnight.

For trend followers, Heating Oil is giving good bullish signals, while Palladium has sunk 25% over the past 4 weeks.

Natural Gas broke its 4 week winning streak as it collapsed 24% over the past week in wicked price action. It rose 30% in the prior 2 weeks.

Other gas contracts such as Dutch TTF and JKM LNG also saw weakness.

Gold (as priced in Australian Dollars) is in a 5 week winning streak.

Soybeans and Corn are registering oversold extremes.

Soybeans are in a 5 week losing streak and have fallen 9 of the past 10 weeks.

While Corn is also nearing a major mean reversion. Some may recall my warnings of not chasing parabolic moves in grain prices at the commencement of the Ukraine invasion.

Cattle is still trading at extended percentages (35%) above its 200 week moving average.

And Lithium Hydroxide has now spent 29 consecutive weeks in weekly oversold territory.

Amongst currencies, the AUD has seen its 4th consecutive week of declines against many pairs (except against the Yen), which sits proportionally within my published note on December 29, 2023 that the AUD was ‘full’.

The U.S. Dollar has risen for the past 3 weeks against most pairs.

The only currency pair trading at an extreme this week is the overbought Indian Rupee versus the U.S. Dollar. Although this occurrence shouldn’t be taken at face value for there are some nuances about it.

I see a dichotomy in the direction of the rising CHF/AUD and the ‘risk-on’ sentiment or more particularly, the strengthening Nasdaq.

This requires more work and some rationalising because the weaker Yen is emphasising ‘risk-on’ in equities.

The Euro was mixed.

The British Pound was firmer.

And the SEK/USD has fallen for 4 consecutive weeks resulting in a tumble of 5%.

This January 7th, 2024 note mentioned something about that.

Each Sunday I publish a note titled ‘Macro Extremes’ which observes and notes prices of various assets or markets trading at the extended part of their ‘pendulum’ for the week that just ended.

Here is a review of some selected price action of those appearing in the publication over the past couple months.

On December 19, 2023, the British 10 year bond yields were at their lowest since May 2023. They have since moved from 3.50% to 3.92%.

The October 22, 2023 edition saw Mexico’s IPC equity index register a ‘quinella’ of oversold readings when it was at 47,800 points. By December 20th, it rallied (21%) to 58,000 points when it reached an overbought quinella.

That same edition mentioned the extreme oversold of the Nasdaq Biotech Index when it was trading around the 3,650 point mark. 3 weeks ago, its was overbought when it hit 4,430 points, which is a stupendous 21% run within 9 weeks.

A week later, the ASX Industrials Index triggered its own oversold quinella at 6,150 points. it soon lifted (12%) to 6,900 points by New Years Day.

And the October 6, 2023 edition warned to not chase the overbought Orange Juice price which was then trading at $3.90. Its current price is $3.08.

The next edition of Macro Extremes is published tomorrow.

While I prepare for a capital expenditure led cycle which will aide the case for higher commodity prices, positioning your investments for such a ‘theme’ won’t be as simple as owning equity in any or many mining companies.

The hoo-ha that we heard about the price of #gold hitting new highs through the month of December 2023 seems now muted.

Today is an example of the risks involved with mining production when combined with the market’s (or analysts) expectation of valuation.

Australia’s Evolution Mining and Canada’s Barrick Gold Corporation both reported their quarterly mining production and their stock prices fell 20% and 9% respectively.

We also saw some commensurate declines amongst some peers.

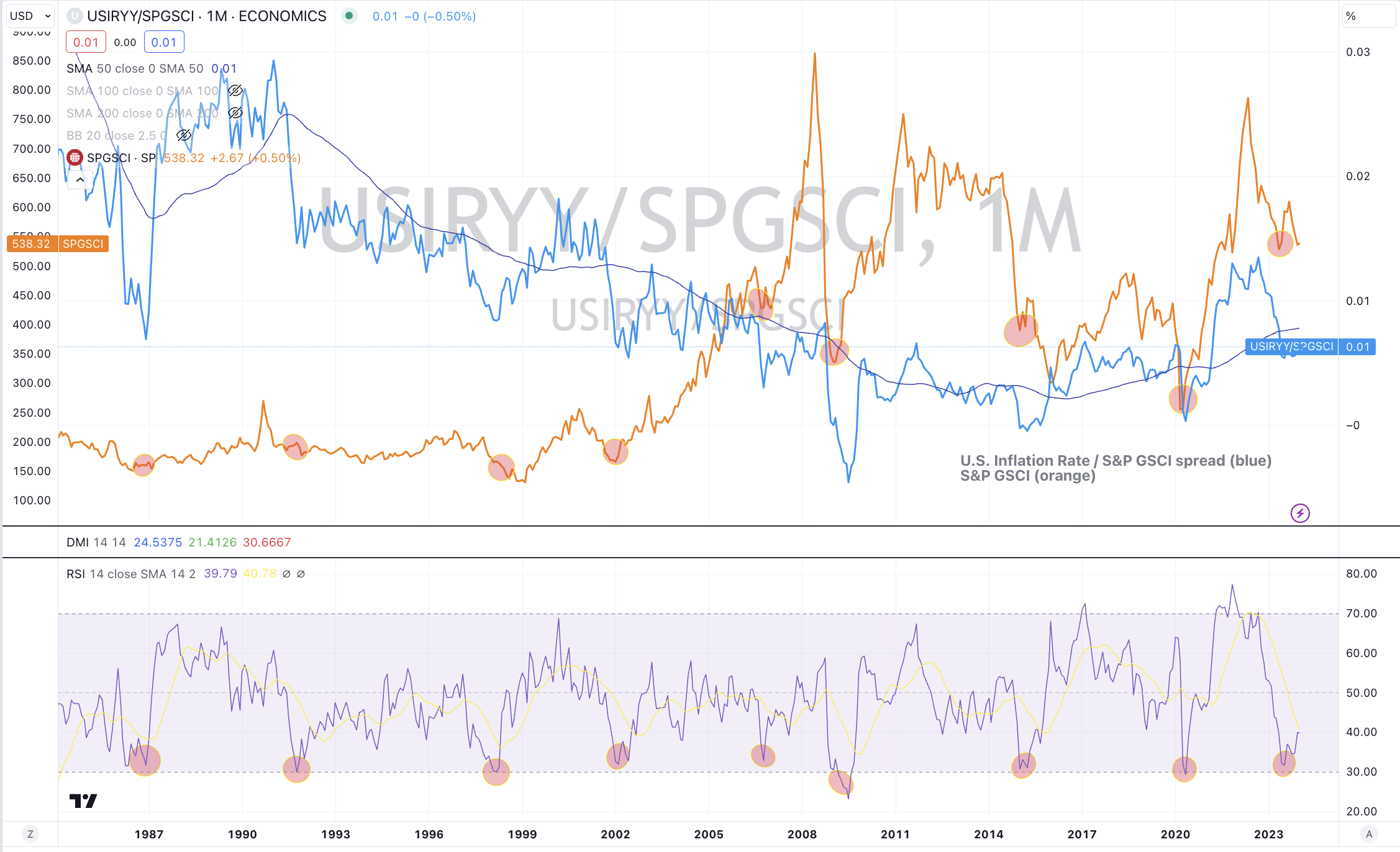

Here are the 9 occurrences over the past 40 years when the U.S. Inflation Rate/S&P GSCI spread was registering a monthly RSI reading of 32 or below.

It coincided with reasonable moments to buy commodities, as illustrated by the orange line which represents the S&P Goldman Sachs Commodity Index (SPGSCI).

I made a similar reference in a note published 2 months ago.

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations

KLSE – the Kuala Lumper Stock Exchange

Nikkei 225

Overbought (RSI > 70)

Cocoa

And India’s NIFTY and SENSEX equity indices

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

SHY – U.S. 1-3 year bond ETF

Uranium

Extremes “below” the Mean (at least 2.5 standard deviations)

Soybeans

Oversold (RSI < 30)

Nickel on India’s MCX Exchange

Nickel on LME

CSI 300

Lithium Hydroxide

JKM LNG

The Oversold Quinella – Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

China 10 year government bond yields

Corn

Notes & Ideas:

Government bond yields fell for the week, giving up some of the previous week’s rise.

Although, it was generally a quiet week, the arrest moves were seen in the tanking of yields amongst the Japanese 2’s and 5’s.

Perhaps lost amongst many was that 2 weeks ago, Brazilian 10’s were at their lowest since August 2021.

And so, even with the recent bounce in yields, the first wave of declines seen since the September/October 2023 highs should be the first past of a larger mean reversion in bond yields.

Equities were mixed with many staying within 1% of last week’s closing prices.

If pressed, there was a slight bias towards weakness. The few that rose appear in this week’s list of movers.

The Nasdaq 100 rose 3.2% recovering the previous week’s 3.1% decline.

Volatile ? Perhaps but certainly we are seeing notable rates of change.

The last few editions listed the list of winning weekly streaks amongst various equity indices. They have all been broken.

The last major intact streak is the 9 consecutive weeks of gains for the Nasdaq Biotechnology Index.

Indonesia’s main bourse has risen for 5 straight weeks.

Inversely, the HSCEI is at its lowest closing price since early November 2022.

The ASX Materials Index has sunk 5% in the past fortnight as has the Hang Seng China Enterprises Index (HSCEI).

Brazil’s BOVESPA and Mexico’s IPC have respectively fallen 2.5% and 3% over the past 2 weeks after being overbought 3 weeks prior.

The SOX rose 3%, recovering half of last week’s 6% slide. It isn’t at a new all-time high which it made a few weeks ago.

And while the S&P 500 continues to ‘act’ constructively, it’s ‘only’ 19% above its 200 week moving average.

Commodities were mostly weaker, albeit slightly.

The big movers were declines seen in shipping rates, metals and grains, again.

The winners included Uranium, Natural Gas, Lean Hogs and Cocoa.

Iron Ore isn’t overbought after falling 4.4% this past week.

The direction of the Copper/Gold Ratio is also back on my radar as this is a good indicator of the economy’s health.

Rotterdam Coal continues its see-saw. The last 3 weeks have seen it fall 8%, then rise 8% to falling 6.5% this past week.

Gold (as priced in Australian Dollars) is in a 4 week wining streak as is Natural Gas.

Natural Gas (Henry Hub) prices have risen 30% in the past 2 weeks, while the Dutch TTG Gas price fell 7% erasing the previous week’s 7% gain.

Soybeans and Corn are registering oversold extremes.

Soybeans is in a 4 week losing real and has fallen 8 of the past 9 weeks.

While Corn is also nearing a major mean reversion. Some may recall my warnings of not chasing parabolic moves in grain prices at the commencement of the Ukraine invasion.

Cattle is still trading at extended percentages (33%) above its 200 week moving average.

Lithium Hydroxide has now spent 28 consecutive weeks in weekly oversold territory.

And Sugar’s rose again, climbing 5% in the past fortnight, following its recent oversold status, which it reached with consecutive weeks of declines.

Amongst currencies, the AUD has seen its 3rd consecutive week of declines against many pairs, which sits proportionally within my published note on December 29, 2023 that the AUD was ‘full’.

The group of largest decliners from the week included;

Aluminium (1.6.%), Rotterdam Coal (6.5%), Baltic Dry Index (30.8%), WTI Crude (1.6%), Iron Ore (4.4%), Copper (1.8%), Coffee (1.6%), Lumber (1.9%), JKM in Yen (11.4%), Tin (4.3%), Newcastle Coal (2.5%), Orange Juice (4.8%), Palladium (5.7%), Platinum (5.2%), Dutch TTF Gas (7.4%), Corn (3%), Soybeans (2.6%), Wheat (3.3%), Shanghai Composite (1.6%), KBW Bank Index (3.1%), HSCEI (2.2%), KRE Regional Bank Index (2.6%), KOSPI (2.1%), Oslo (1.4%), Chile (1.4%) and the ASX Materials. Index fell 1.8%.

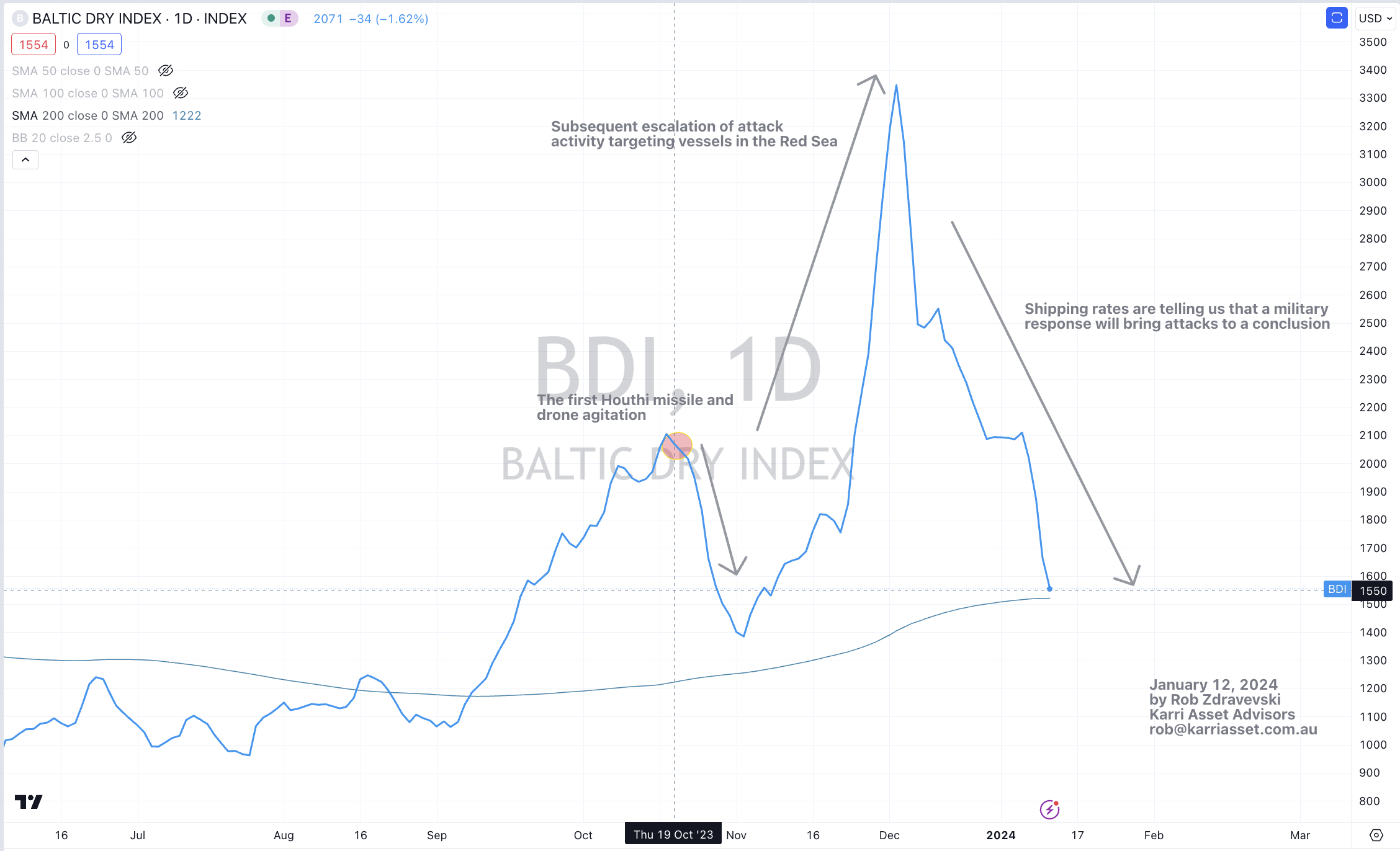

Since this post on December 20, 2023, warned readers to not trade (chase) the headlines, Shipping Rates and Oil prices have declined.

Within it, I wrote, “The global powers with economic interests will put a stop to it and the companies with a commercial interests will simply cease putting cargoes at risk.”

Now, 22 days later, we are seeing their “corrective measures”.

The notations in the attached charts point out how prices reacted from October 19, 2023 when the first missiles and drones (bound for Israel) were shot down and when activity escalated around mid-December 2023.