A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

n.b. pricing of (commodity) futures contracts is only considering the immediate front month.

* denotes multiple week inclusion

Extremes above the Mean (at least 2.5 standard deviations)

IEF, IEI & SHY ETF’s

Sugar #16

EUR/GBP

EUR/USD

NZD/AUD

PHP/USD

Overbought (RSI > 70)

Australian government 10 year bond yield minus the Aust. 2 year bond yield spread

BofA High Yield Index

Tin

Urea (U.S. Gulf)

Gold in CAD and USD

Pakistan’s KSE Index *

And Chile’s IGPA Indices *

The Overbought Quinella (Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

BofA BB High Yield Option Adjusted Spread

U.S. 10 year minus U.S. 5 year bond yield spread

U.S. 30 year minus U.S. 10 year bond yield spread *

Gold in AUD and ZAR *

Extremes below the Mean (at least 2.5 standard deviations)

Australian 2, 3, 5 & 10 year bond yields

German and Italian 2 year bond yields

New Zealand & Polish 10 year bond yields

U.S. 10 year break-even inflation rate

TBX

U.S. 3, 5, 7 and 10 year bond yields

U.S. 5 year bond yield minus the U.S. 5 year break-even inflation rate

U.S. 5 year bond yield minus the U.S. 3 month bill yield

U.S. 5 year bond yield minus U.S.inflation rate

U.S. 10 year bond yield minus the Australian 10 year bond yield

U.S. 10 year bond yield minus the U.S. 10 year break-even inflation rate

U.S. 10 year bond yield minus the U.S. 10 year inflation rate

Aluminium

Brent and WTI Crude Oil

Cotton

U.S. (DXY) Dollar Index

Iron Ore

Gasoline

S&P GSCI

USD/CHF

USD/DKK

USD/SEK

Amsterdam’s AEX

KBW Bank Index

Dow Jones Industrials

Taiwan’s TAEIX Index *

KRE Regional Banks Index

Nikkei 225

Toronto’s TSX

Vietnam

ASX Materials

And ASX Small Caps

Oversold (RSI < 30)

U.S. 3 month government bill yield *

U.S. 10 year bond yield minus the German 10 year bond yield spread

Australian Coking Coal *

Richards Bay Coal *

North European Hot Rolled Coil Steel *

Lithium Carbonate *

Lithium Hydroxide *

Newcastle Coal *

Orange Juice *

Uranium *

AUD/INR

AUD/USD

CAD/CHF

Indonesia’s IDX

Nasdaq Transports

And Thailand’s SET Index *

The Oversold Quinella (Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

Indian 10 year government bond yield *

U.S. 2 year bond yield

AUD/CAD

AUD/EUR

AUD/CHF

AUD/SGD

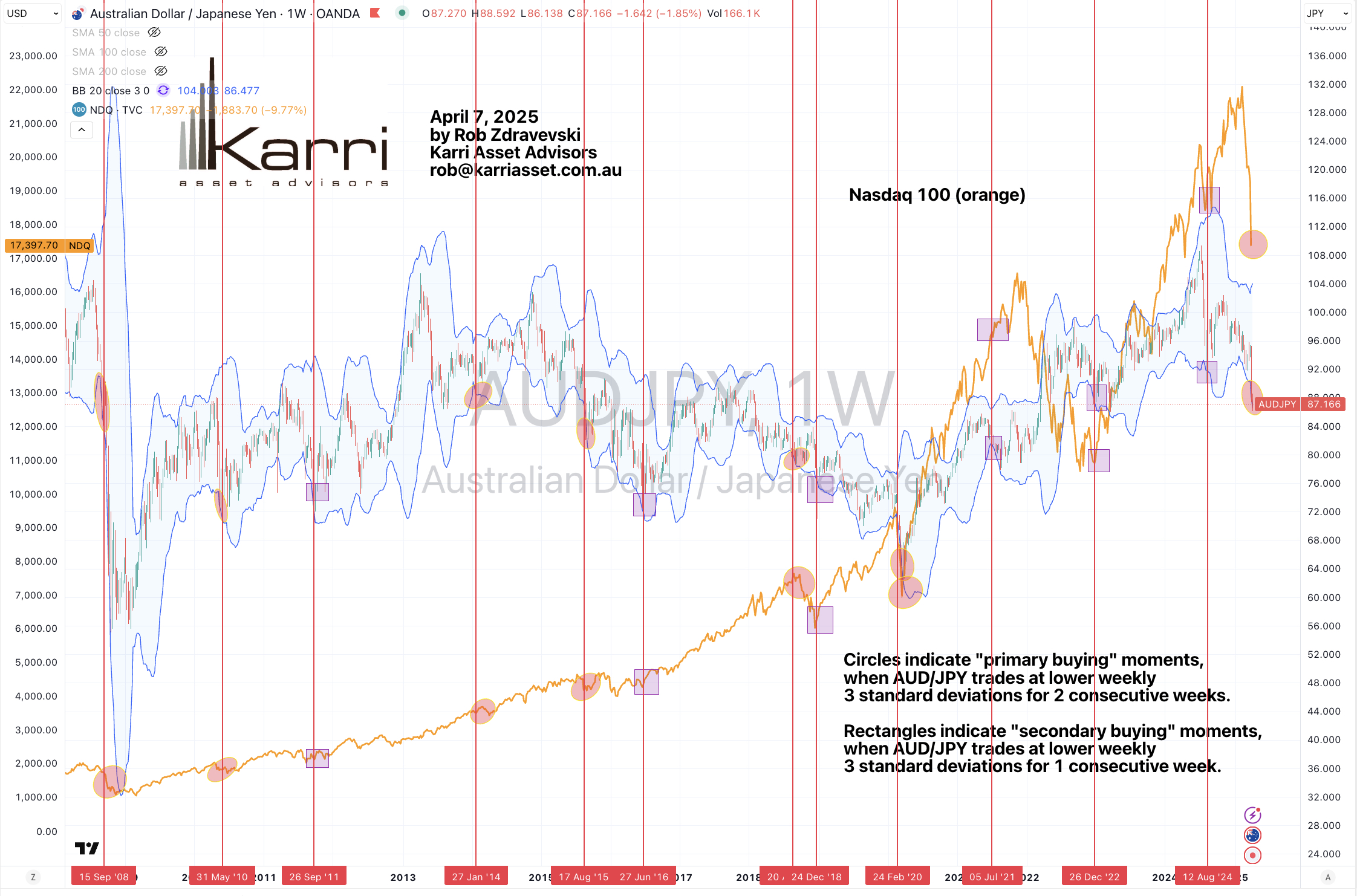

AUD/JPY

AUD/GBP

Dow Jones Transports

S&P Small Cap 600

Russell 2000

FTSE 250

S&P MidCap 400

Nasdaq Biotech Index

Copenhagen

Stockholm

Nasdaq Composite

Philadelphia Semiconductor (SOX) Index

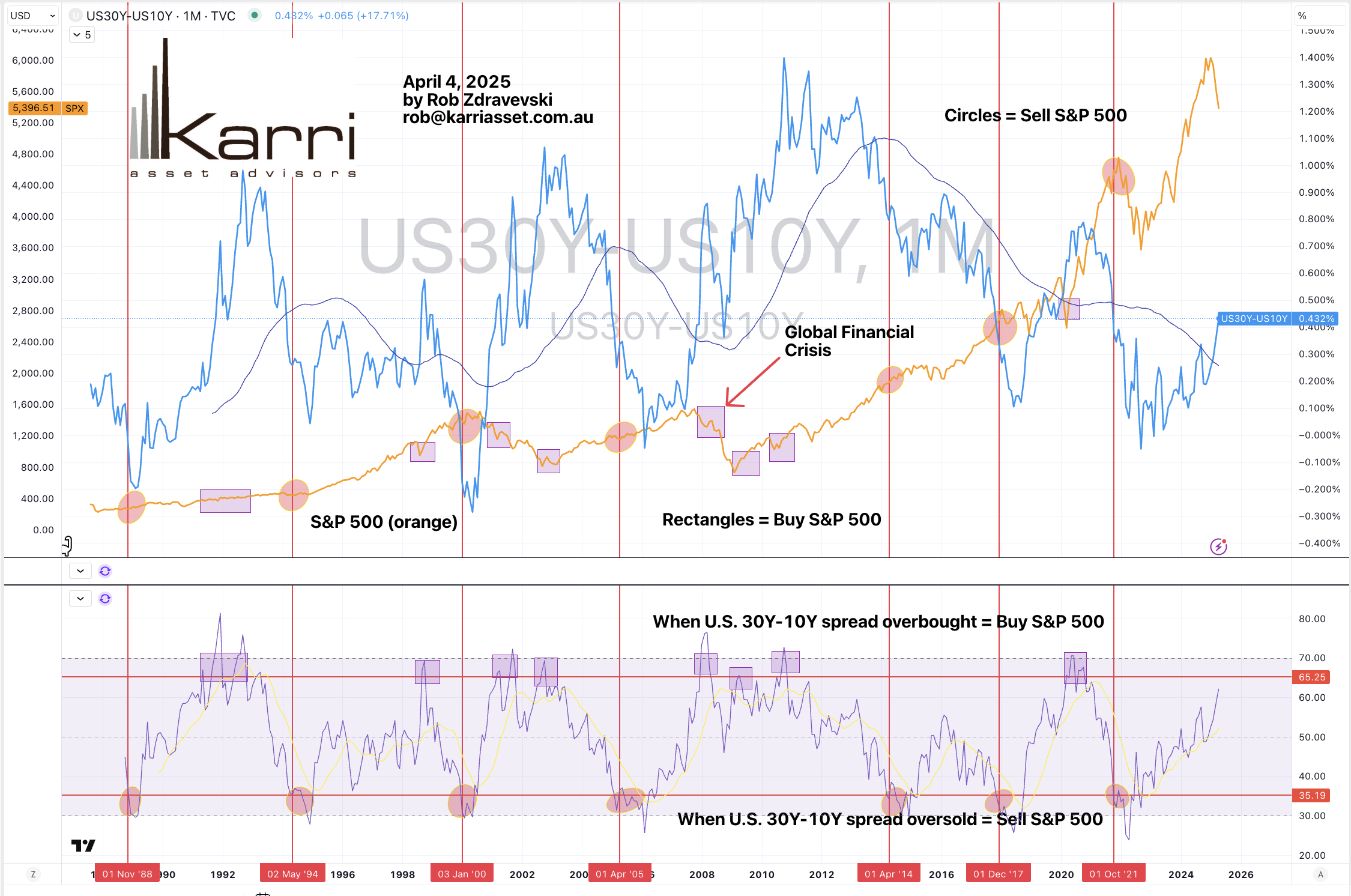

S&P 500

Nasdaq Transports

And the IBB and XBI Biotech ETF’s

Notes & Ideas:

Government bond yields fell.

Any yields which were overbought last week are no longer so.

In this week’s overbought category you’ll find term spreads and high yield bond indices appearing.

The oversold category is full of shorter duration yields, cross country yield spreads and real interest rate spreads.

Austrian and Spanish 10’s are in a 4 week losing streak,

As are Aussie 2, 3 and 5 year yields along with German 2’d and 5’s.

U.S. 2 year bond yield mean reverted.

The U.S. 30 year minus U.S. 10 year yield spread has risen for 8 consecutive weeks.

This includes the whole Japanese curve which tanked this week. Leveraged shorter’s most likely became bankrupt. The widow maker is back.

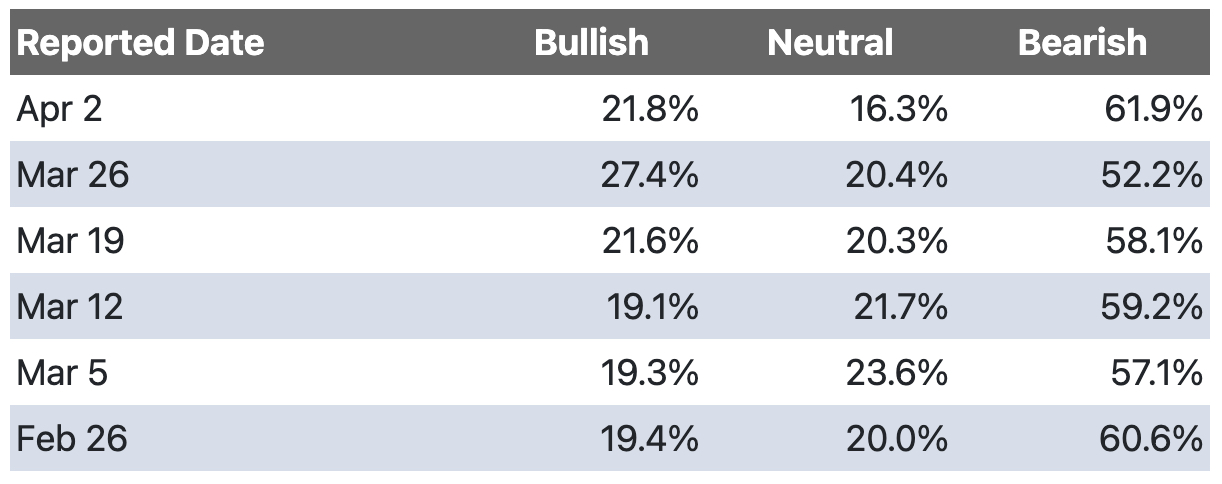

Equities were decisively weaker, again.

This week features a very longest of equity indices trading at oversold extremes.

There were also many indices which mean reverted.

For the 2nd week in a row, Chinese stocks weathered the storm.

The DAX, Hang Seng, Stockholm and Helsinki have fallen for 4 weeks straight.

Copenhagen is in a 5 week losing streak.

The Nasdaq Biotech have fallen for 6 weeks.

DJ Transports, the FTSE 250 and the SOX have also declined for 7 consecutive weeks.

The Nasdaq Composite has retreated for 6 of the past 7 weeks.

The S&P 500 has sunken for 6 of the past 7 weeks.

The S&P Small Cap 600, S&P MidCap 400 and the Russell 2000 have fallen 9 of the past 10 weeks.

The KRE Regionals Banks Index is back to the same price seen in July 2024.

Commodities were weaker.

The indices were mainly affected by the slump in oil prices.

Thus we see Crude and Gasoline at oversold extremes.

Some winners included Urea, Tin, Cocoa and Steel prices.

A couple of them made into overbought territory.

Coking Coal prices are working their way from being oversold for some time.

Orange Juice mean reverted.

Tin has risen 19% over the past 5 weeks.

Copper prices tanked.

Australian Coking Coal broke its 4 week losing streak.

Gold as priced in AUD have risen for 5 consecutive weeks.

while Lithium Hydroxide has been oversold territory for 96 consecutive weeks.

Currencies were woken from slumber and very active.

The simplest observation was risk was ‘off’.

That means the Aussie and Loonie were dumped and the Yen and Swiss were bought.

The world does this when its worried and risk averse.

The Australian Dollar fell 4% (or more) against every currency pair.

Perversely, the Loonie has risen for 5 straight weeks against the USD.

Both ‘risk’ currencies (AUD & CAD) rose against the Yen.

And the GBP/JPY broke its 5 week rising streak.

The larger advancers over the past week comprised of;

Australian Coking Coal 2%, Cocoa 5.8%, U.S. Hot Rolled Coiled Steel 4.7%, Tin 7.5%, Sugar #16 7.4%, Urea U.S. Gulf 6.1%, Urea Middle East 4.1%, Gold in AUD 2.5% and Gold in ZAR rose 2.1%.

The group of largest decliners from the week included;

Richards Bay Coal (3.4%), Aluminium (10.2.%), Bloomberg Commodity Index (5.8%), Baltic Dry Index (7.1%), Brent Crude (9.2%), WTI Crude Oil (10.6%), Cotton (5.3%), Copper (14.2%), Heating Oil (6.6%), Arabica Coffee (3.8%), Lumber (13%), Cattle (3.3%), JKM LNG in Yen (6.7%), Lithium Carbonate (6.7%), Lithium Hydroxide (5.7%), Newcastle Coal (8%), Natural Gas (5.6%), Nickel (10.2%), Orange Juice (4.4%), Palladium (7.8%), Platinum (8.2%), Gasoline (8.4%), Robusta Coffee (4.2%), S&P GSCI (6.8%), CRB Index (6%), Dutch TTF Gas (10.8%), Gasoil (8%), Silver in AUD (9.8%), Silver in USD (13.3%), Gold in CAD (2.2%), Gold in CHF (3.8%), Gold in EUR (2.7%), Gold in USD (1.5%), Oats (2.1%), Rice (3.3%), Soybeans (4.5%), All World Developed ex-USA (6.6%), AEX (7.3%), ATX (9.9%), KBW Bank Index (13.8%), BUX (9.2%), CAC (8.1%), ChinaA50 (5.1%), DAX (8.1%), DJ Industrials (7.8%), DJ Transports (9.8%), MIB (10.6%), HSCEI (2.2%), Hang Seng (2.5%), IBEX (6.7%), Bovespa (3.5%), IDX (7.3%), S&P SmallCap 600 (9%), Russell 2000 (9.6%), Nasdaq Composite (10%), KRE Regional Banks (12.7%), KOSPI (3.6%), FTSE 250 (7.6%), S&P MidCap 400 (9.1%), Mexico (3.2%), Nasdaq Biotech (9.8%), Nasdaq 100 (9.8%), Nikkei 225 (9%), NIFTY (2.6%), Oslo (7.8%), Copenhagen (10.9%), Helsinki (7.4%), Stockholm (10.1%), PX (7.9%), SA40 (8.9%), SENSEX (2.7%), SET (4.3%), SMI (9.3%), SOX (16%), IGPA (2.4%), S&P 500 (9.1%), IPSA (2.5%), STI (3.7%), Nasdaq Transports (9.8%), TSX (6.3%), FTSE 100 (7%), Vietnam (8.1%), WIG (9%), ASX Financials (2.8%), ASX 200 (3.9%), ASX Materials (7.1%), ASX Industrials (3.4%), ASX Smal Caps (6.4%), BIST (2.9%) and the XBI Biotech ETF fell 12.7%.

April 6, 2025

By Rob Zdravevski

rob@karriasset.com.au