Macro Extremes (week ending February 25, 2022)

February 27, 2022 Leave a comment

The following assets (on a weekly timeframe) registered an Overbought reading or traded more than 2.5 standard deviations above its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

Gold

Lean Hogs

Palladium

Platinum

Corn

Overbought (RSI > 70)

Australian 2, 3 and 5 year government bond yields

U.S 2, 5 & 10 year government bond yields

German 5 year government bond yields

Spanish, French, Greek, Italian, Japanese, Portuguese and New Zealand 10 year government bond yields

CRB Index

Australian Coal

Aluminium

Gasoil

Tin

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Australian & Russian 10 year government bond yields

Bloomberg Commodity Index

WTI Crude Oil

Brent Crude Oil

Gasoline

Nikkei 225 Index

Assets (securities) which touched the other side of the extreme, being Oversold (where the RSI is < 30) or were at least 2.5 standard deviations below its mean are;

Extremes “below” the Mean (at least 2.5 standard deviations)

Korean Won / USD

AEX, CAC, DAX, DJIA, MIB, IBEX, S&P Midcap 400, Nasdaq 100, Sensex, Copenhagen, Swiss SMI and the S&P 509

Oversold (RSI < 30)

U.S. 10 year minus 2 year government bond yield spread

Hot Rolled Coil Steel (HRC)

Korea’s KOSPI Index

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Russian Ruble / USD (it weakened 8%)

Notes & Ideas:

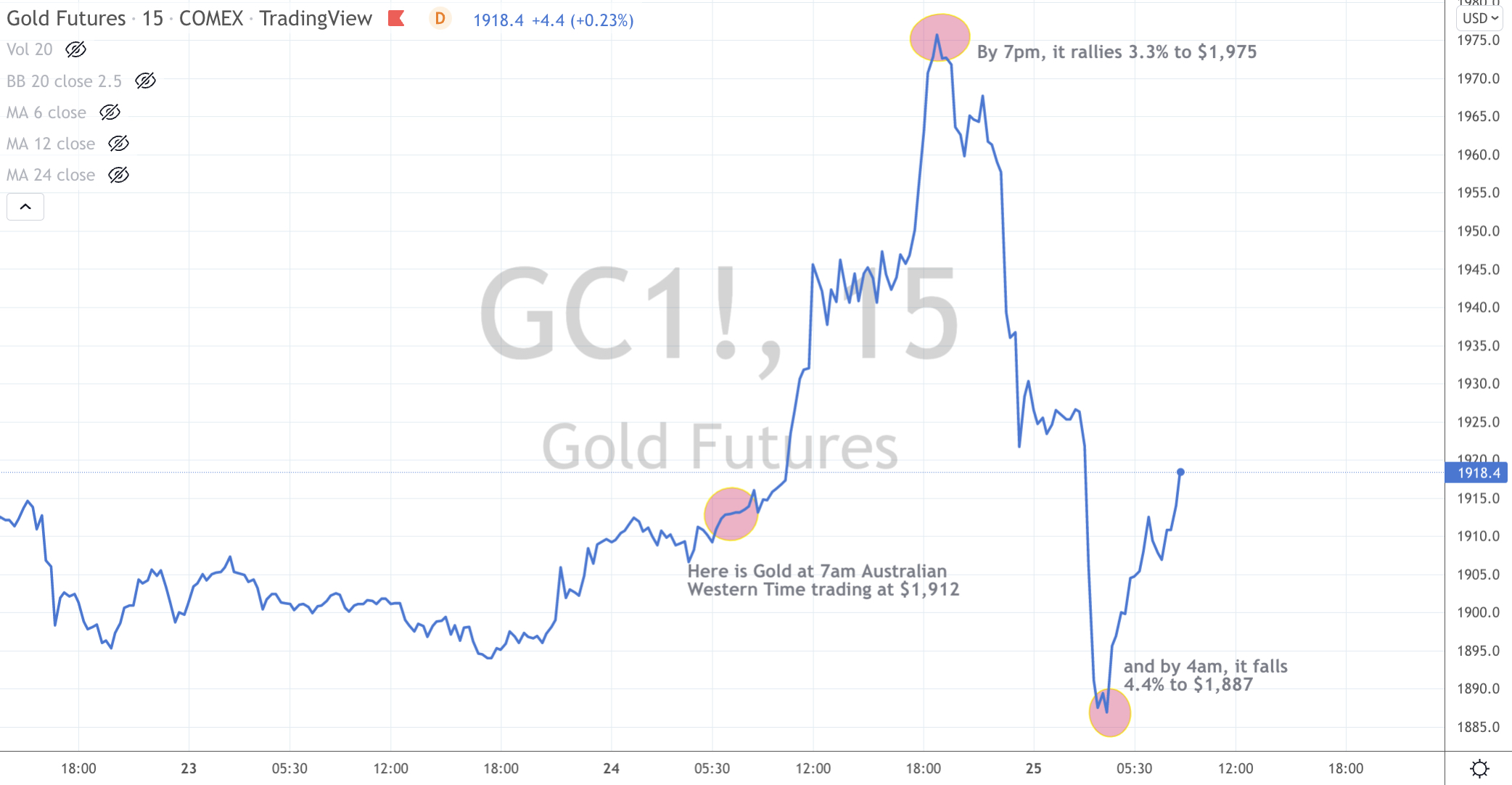

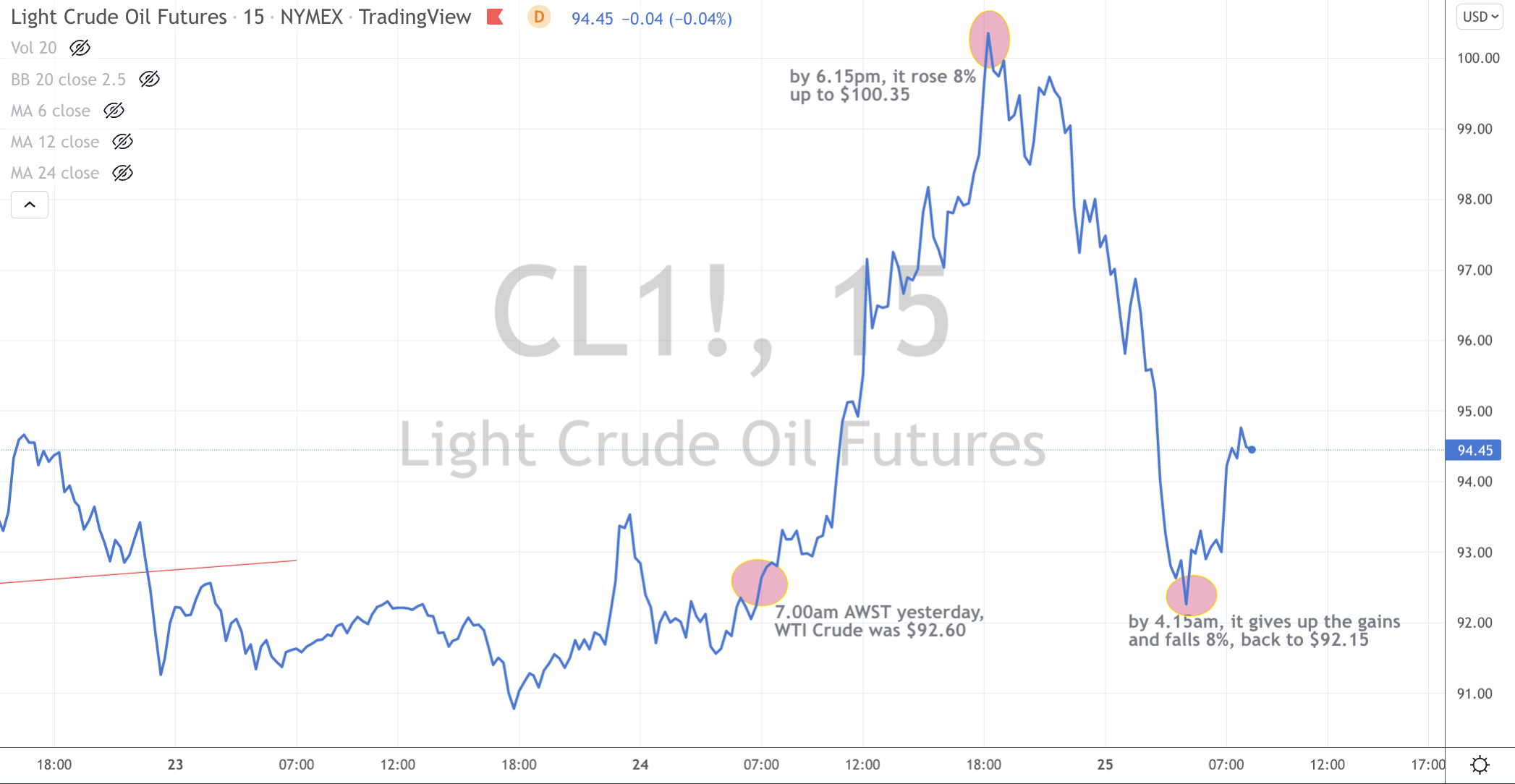

This week’s big news was the savage decline (and reversal) in prices due to the initial reaction of Russia attack on Ukraine.

For example, at their highest points Heating Oil, Natural Gas, Crude Oil, Soybeans and Corn rose between 10%-11%.

Wheat advanced 19% at one stage, Dutch TTF Gas soared 80%, Gasoline climbed 15% and Gold rose 4% to only close ‘flat’ on the week.

On the flip side, the U.S. KBW Banking, DAX and CAC were down 7% at their lowest ebb during the week.

Such volatility is not only a test of one’s metal and resolve but is a costly lesson for those ‘whipsawed’ through their stop losses.

I illustrated some of the intra-day moves in this post.

Russian 10 year bond yields move from 9.8% to 12.2% and Turkish 10’s went from 20.8% to 23%.

However, there are some misnomers in the Oversold equity indices readings as they breached their 2.5 standard deviation moves ‘intra-week’ before reversing higher.

Incidentally, the Baltic Dry Index rose 11% on the week. This measure of the cost of shipping dry, bulk goods is up 68% since my ‘bottom’ call on January 24th.

Since they appeared and were cited in this weekly note a few weeks, Coffee and Orange Juice are down 8% and 13% respectively since they registered Overbought Extremes.

And the ‘surprise’ was the U.S. indices finished in the black for the week.

You can read a note written this week which recalled when U.S. equities rose during the 1991 Iraq aerial attack and how equities rose throughout those 32 days.

The larger advancers over the past week comprised of;

Aluminium 3.1%, Australian Coal 2.4%, Rotterdam Coal 17.9% (was up 32%), Baltic Dry Index 11.4%, WTI Crude 1.5%, Gasoil 3.1%, Heating Oil 2.4%, JKM 15.5%, Lumber 2.2%, LNG 13%, Tin 2.7%, Natural Gas 0.9%, Nikkei 2.1%, Gasoline 7.7%, Silver 0.1%, TTF 26.3%, Brent Crude 5.1%, Urea 19%, Uranium 8.2%, Corn 0.8%, Wheat 6.9%, S&P 500 Midcap 1.2% (was down 5.6%), Nasdaq 1.3%, SOX 2% and S&P 500 0.8%.

The group of decliners included ;

China Coal (7.8%), Iron Ore (3.2%), Gold (0.6%), Hogs (5.2%), Copper (1%), HRC (9.6%), Coffee (3%), Platinum (2.5%), Cotton (2%), Gold in AUD (1%), Oats (10.5%), Soybean (1.2%), AEX (2.3%), CAC (2.6%), DAX (3.2%), DJIA (0.6%), MIB (2.8%), HSCEI (6.4%), Hang Seng (6.4%), MOEX (27.2%) was down 50%, KOSPI (2.5%), Nikkei (2.4%), Sensex (3.4%), Helsinki (3.2%), Stockholm (2.6%), Strait Times (3.9%), TAEIX (3.2%), Istanbul (5.3%) and the ASX 200 (3.1%).

February 27, 2022

by Rob Zdravevski

rob@karriasset.com.au