Be careful chasing shiny things

March 15, 2022 Leave a comment

Here is a little story of Palladium’s recent price action.

Platinum will be more interesting to buy around the $900 mark.

March 15, 2022

by Rob Zdravevski

rob@karriasset.com.au

Trying to hear what's not being said

March 15, 2022 Leave a comment

Here is a little story of Palladium’s recent price action.

Platinum will be more interesting to buy around the $900 mark.

March 15, 2022

by Rob Zdravevski

rob@karriasset.com.au

March 14, 2022 2 Comments

First, you must pick a currency.

It is the first thing you must do; when conducting business, settling a transaction or making an investment.

Even if you are buying oranges from the greengrocer, unless you are trading them for apples.

It’s time for some tactical tweaks and tilts in the Currency market.

The evident move has been the strengthening of the U.S. Dollar.

I’m a Seller of some USD and preparing to…..

Buy some Euro near the 1.08 level,

Buy some GBP at 1.2850,

Buy JPY (now) around the 117.50 mark,

Buy some HKD (if you have business to conduct there)

The Korean Won is back to the same weakness (against the USD) seen in March 2020, which mimics the same level as February 2016 and July 2010.

That is certainly making South Korea competitive again which is good for their electronics, heavy machinery and automobile industries.

I’ll be interested buying their equities when the KOSPI Index touches 2,460, which is a further 7% below today’s closing price.

And finally, the Danish Krone (DKKUSD 6.80) and Swedish Krona (SEKUSD 9.60) are also exhibiting notable weakness, attractive to Buy, should you specific commercial requirements to do so.

March 14, 2022

by Rob Zdravevski

rob@karriasset.com.au

March 14, 2022 Leave a comment

As of March 14, 2022….

These are the most stinkiest, unloved and oversold equity indices in the world at this moment;

(except for Russia because it’s not open for trading)

CSI 300

DAX

Italy’s MIB

HSCEI

Hang Seng

IBEX

Helsinki

And these ones are nearly there……but not yet

FTSE 100

Stockholm

Amsterdam

CAC 40

Shanghai Composite

Kospi

Nikkei 225

March 14, 2022

by Rob Zdravevski

rob@karriasset.com.au

March 14, 2022 Leave a comment

The bias for the AUDUSD is lower.

The recent 2 cent rally was divergent to the global US Dollar rally and was without strength.

Its on important support at the moment, being 0.7230

but it is something to watch closely and poised to break either way in next 2 days as it remains stuck in a broad range between 0.7550 and 0.6970.

but my work suggests the ’set-up’ is for lower AUD vs USD,

this will translate a reversal in USD strength against the Yen as well

If we see all this play out, it should also result in commodity prices correcting and a truce called between Russia/Ukraine.

March 14, 2022

by Rob Zdravevski

rob@karriasset.com.au

March 14, 2022 Leave a comment

The consensus seems to be;

Stocks are going lower,

Gold is destined higher,

Interest Rates can only rise,

Inflation is omnipresent,

Other commodities will stay elevated

and Oil is to surge further.

I’m spending some time thinking about the opposite occurring.

Furthermore, I have been commenting to clients how dangerous these markets can be.

In some cases, they are resembling a ‘video game’.

This means that the reality of the risks involved doesn’t always register or perhaps the repercussions aren’t recognised or considered to be real.

WTI Crude Oil recently traded at a high of $130.50.

5 days later , it is now $106.

When you ponder that someone bought that Oil at that $130.50 high and should they still hold it, they are comforting a 18%.

This is the same percentage loss that buyers of Wheat are wearing if they also paid the recent highest price.

On March 7th, someone paid $227 for a futures contract in Dutch TTF Natural Gas. Today’s that European gas price is trading at $131.

When riding any type of wave, it’s quite nice to surf the fat part of the ride. You want to avoid the foam and choppy bits.

It is often when things become broken and messy.

March 14, 2022

by Rob Zdravevski

rob@karriasset.com.au

March 14, 2022 Leave a comment

Here is the US10-US02 bond yield spread (the yield curve) overlaid against the S&P 500.

If you closely track when the yield curve goes ‘notably’ Oversold (on a weekly basis), it’s prescient that the S&P 500 finds support for its next advance.

Now it is doing this for the 9th time in 35 years.

The only time when a new S&P 500 bullish trend was stifled or diffused, was when the yield curve moves sharply to an Overbought level (or more specifically to a reading near to 62 or above) within 10 months of seeing its previous Oversold moment.

Coinciding with my earlier posts today, the timing of entry will be the artistic part.

The science of seeing the yield curve touching 0.08% – 0.02% may aid the decision.

March 13, 2022

by Rob Zdravevski

rob@karriasset.com.au

March 13, 2022 Leave a comment

Here is another one for the asset allocators……the S&P 500 is making its 26th visit down to a 2.5 standard deviation move within the past 35 years.

It’s been a handy long term buying moment.

p.s. Long-Term doesn’t equal 3 weeks.

Long-Term is the type of timeframe involved when you consider buying shares for a new born child and not telling them about it until they are allowed to legally buy alcohol.

Timing the entry points and wading in will be artistic part.

March 13, 2022

by Rob Zdravevski

rob@karriasset.com.au

March 13, 2022 Leave a comment

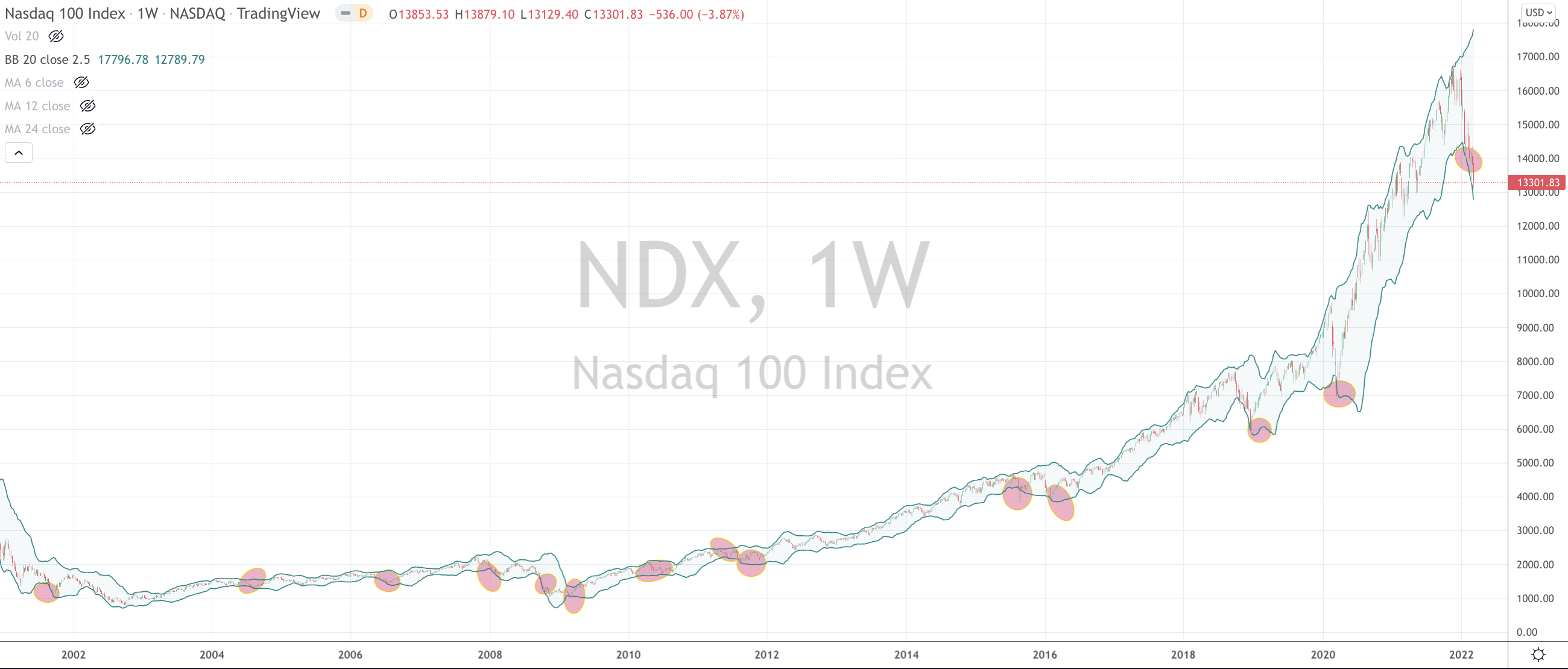

Also, the Nasdaq 100 is in a patch where it’s trading 2.5 standard deviations below its weekly mean.

This is the 14th ‘patch’ in 20 years.

Note the circles in the chart below.

Of course, there is accompanied analysis required, although it bodes well for the beginning of a purple ‘circled’ patch.

March 13, 2022

by Rob Zdravevski

rob@karriasset.com.au

March 13, 2022 Leave a comment

The weekly Relative Strength Index (RSI) for the Nasdaq 100 Index has just registered a reading of 33 or less, for only the 9th time in 34 years.

I’m watching for an extension of the March swoon before initiating some new equity investments and adding to some existing ones.

But under the heading of conditioning for lower and perhaps ‘normal’ returns, don’t expect a moonshot rebound, while I’ll also keep in mind that nobody ‘deserves the bottom’.

March 13, 2022

by Rob Zdravevski

rob@karriasset.com.au

March 13, 2022 Leave a comment

The following assets (on a weekly timeframe) registered an Overbought reading or traded more than 2.5 standard deviations above its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

China Coal

Gasoil

Heating Oil

Japanese Korean (JKM) LNG Marker

Tin

Nymex LNG

Platinum

Palladium

Dutch TTF Gas

Uranium

Rice

AUD/GBP

Overbought (RSI > 70)

Australian 2, 5 & 10 year government bond yields

U.S. 2 & 5 year government bond yields

Greek, Spanish, Turkish & New Zealand 10 year government bond yields

Soybeans

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Australian 3 year government bond yields

U.S. Dollar (DXY) Index

Bloomberg Commodity Index

CRB Index

WTI Crude Oil

Brent Crude Oil

Gasoline

Rotterdam Coal

Australian Coal

Nickel

Corn

Wheat

Gold Volatility Index

Gold (in AUD & USD)

Assets (securities) which touched the other side of the extreme, being Oversold (where the RSI is < 30) or were at least 2.5 standard deviations below its mean are;

Extremes “below” the Mean (at least 2.5 standard deviations)

U.S. 10 year minus Australian 10 year government yield spread

Copper/Gold Ratio

Oil/Gold Ratio

EUR/AUD

EUR/GBP

EUR/USD

DKK/USD

JPY/USD

Dow Jones Industrial Average

S&P 500

U.S. (KBW) Banking Index

Sensex, IBEX, Nikkei 225, DAX, FTSE-100 and Italy’s MIB equity indices

Oversold (RSI < 30)

U.S. 10 year minus 2 year government bond yield spread

(Now at the same level as March 9th, 2020)

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

KRW/USD

SEK/USD

HKD/USD

AEX, CSI 300, HSCEI, Hang Seng, Helsinki, Stockholm & Switzerland’s SMI equity indices

Notes & Ideas:

Broadly, we have seen an opposite of the previous week. It was a resumption of weakness for American indices and a rebound in Europe. For some context, a 4% bounce in an Oversold DAX merely recovers part of the previous week’s 10% decline and Helsinki’s 7% rise recouped part of last week’s 1% slump.

But we did see reasonable declines amongst Asian bourses.

Last week, I wrote that it “was a week for the record books”.

Alas, that has all been trumped by even higher intra-week highs, some resembling ‘blow-off tops”and then followed by wicked retracements and reversals.

For example, Gasoil (diesel) was up 40% at one stage to end up closing the week 14.6% lower. JKM was up 34%, Palladium surged 39% and then registered a 6% decline on the week, Nickel soared 152% and saw a 13 standard deviation weekly move while Copper traded 4 standard deviations above its mean.

If you didn’t look at the numbers, you’d think Oil was up on the week while mild mannered Cocoa was steady and unchanged.

Incidentally, it’s OK that Wheat fell 8% for the week because it rose 40% last week.

In other reversal news, bond yields rose, meaning prices fell suggesting geopolitical risk was waning.

While it remains a sellers market in commodities, it is a buyers market in selected equities.

As I’ve written in recent newsletters, I am finding the most amount of investible opportunities than I’ve seen in the past 15 months.

The larger advancers over the past week comprised of;

Baltic Dry Index 26.5% (which is + 76% in 6 weeks), Aust. Coal 9.8%, Gold 1%, Hogs 2.3%, Nickel 25.4%, Silver 1.4%, Cotton 4%, Urea 4.2%, Uranium 16.5%, Gold (in AUD) 2.1%, Corn 1.1%, CAC 3.3%, DAX 4.1%, MIB 2.6%, IBEX 5.5%, Sensex 2.4%, Helsinki 6.6%, Stockholm 4.3%, SMI 1.7%, FSTE 2.4% and Istanbul rose 4%.

The group of decliners included;

Aluminium (11%), Rotterdam Coal (15.9%), China Coal (11%), WTI Crude (5.5%), Gasoil (14.6%), Copper (6.3%), Heating Oil (9.5%), HRC (4.3%), JKM (3.9%), Lumber (11.6%), Nymex LNG (33.3%), Tin (5%), Natural Gas (5.8%), Orange Juice (6.2%), Palladium (6.2%), Gasoline (6.5%), Brent Crude (4.8%), Rice (3.6%), Wheat (8.5%), Shanghai (4%), KBW (2.3%), CSI 300 (4.2%), DJIA (2%), HSCEI (8.2%), HSI (6.2%), IBOV (2.4%), Kospi (2%), S&P Midcap 400 (1.7%), Nasdaq (3.9%), Nikkei (3.2%), SMI (3.5%), S&P 500 (2.9%), TAIEX (2.7%), DJ Transports (3.8%) and Australia’s ASX 200 only declined 0.7%, erasing part of last weeks 1.6% advance.

March 13, 2022

by Rob Zdravevski

rob@karriasset.com.au