Furthermore, it has risen 50% from a low seen on November 1st, 2022.

The chart below shows an empirical study of the percentage that the price of sugar has traded above its 200 week moving average.

Ordinarily, such rising inputs would normally affect the margins of chocolatiers, confectioners and soft drink manufacturers, however it seems these companies have managed to pass on higher costs under the story of wide spread inflation.

Many of their stock prices are performing very well.

The rising price of sugar is also a boon to sugar cane growers (with Brazil and India being the world’s two largest producers) and those around Mackay, Queensland.

Today, the price of sugar is trading in rarified air.

It is also registering overbought tendencies.

And when my analysis incorporates the outsized ‘long’ positions in the Commitments of Traders then I will recognise it as the momentum trade that it is.

In other words, the probability of higher prices diminishes under the current conditions and any unwinding of those non-commercial ‘trading longs’, can see a sharp drop and test of that 200 week moving average.

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

EUR/USD

DKK/USD

AUD/IDR

Overbought (RSI > 70)

Silver (in AUD)

Gold (in AUD)

Russia’s MOEX Index

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Sugar

EUR/AUD

Extremes “below” the Mean (at least 2.5 standard deviations)

China 10 year government bond yields

U.S. 10 year bond yield minus German 10 year bond yield

Iron Ore

Corn

Oats

Soybeans

Oversold (RSI < 30)

U.S. 5 year bond yield minus U.S. 3 month bond yield

Australian Coking Coal

JKM LNG Gas

Lithium Hydroxide

AUD/GBP

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

None

Notes & Ideas:

Equities generally had quiet week, again, with a slight bias towards weaker prices.

For instance, the S&P 500 rose 0.9%, while Midcaps and Smallcaps fell 0.3% and 1% respectively.

The SOX, FTSE and ASX smallcaps fell between 0.3% and 0.9% for the week, while the ASX 200 rose 0.2%.

Trend less equity markets remains the trend, for now.

Government bond yields fell. While my trend analysis favours lower yields, pattern recognition work tells me it’s prudent to identify the sideways and ‘holding’ pattern seen of late and wait for new ‘higher high’ or ‘lower low’ to be recorded.

The Japanese 10 year bond yield recorded the most notable drop from 0.46% to 0.38%.

The most action was seen in Commodities as it had the active week in some time.

Coffee, Cocoa, Cattle, Middle East Urea and Hot Rolled Coil Steel are no longer sporting overbought tendencies.

Sugar’s 6 week rally has now amounted to a 27.5% return.

In fact, the streaks amongst commodity prices have returned. Heating Oil has declined for 5 consecutive 5 weeks, Lithium has sunken for 9 weeks, Australian Coking Coal is in a 5 week downward streak (9 of its past 10 have been negative) while the EUR/USD is in its 9th rising week.

We saw a continuation of last week’s weakness in energy, copper and soybeans with more agricultural (corn and wheat) joining the declines.

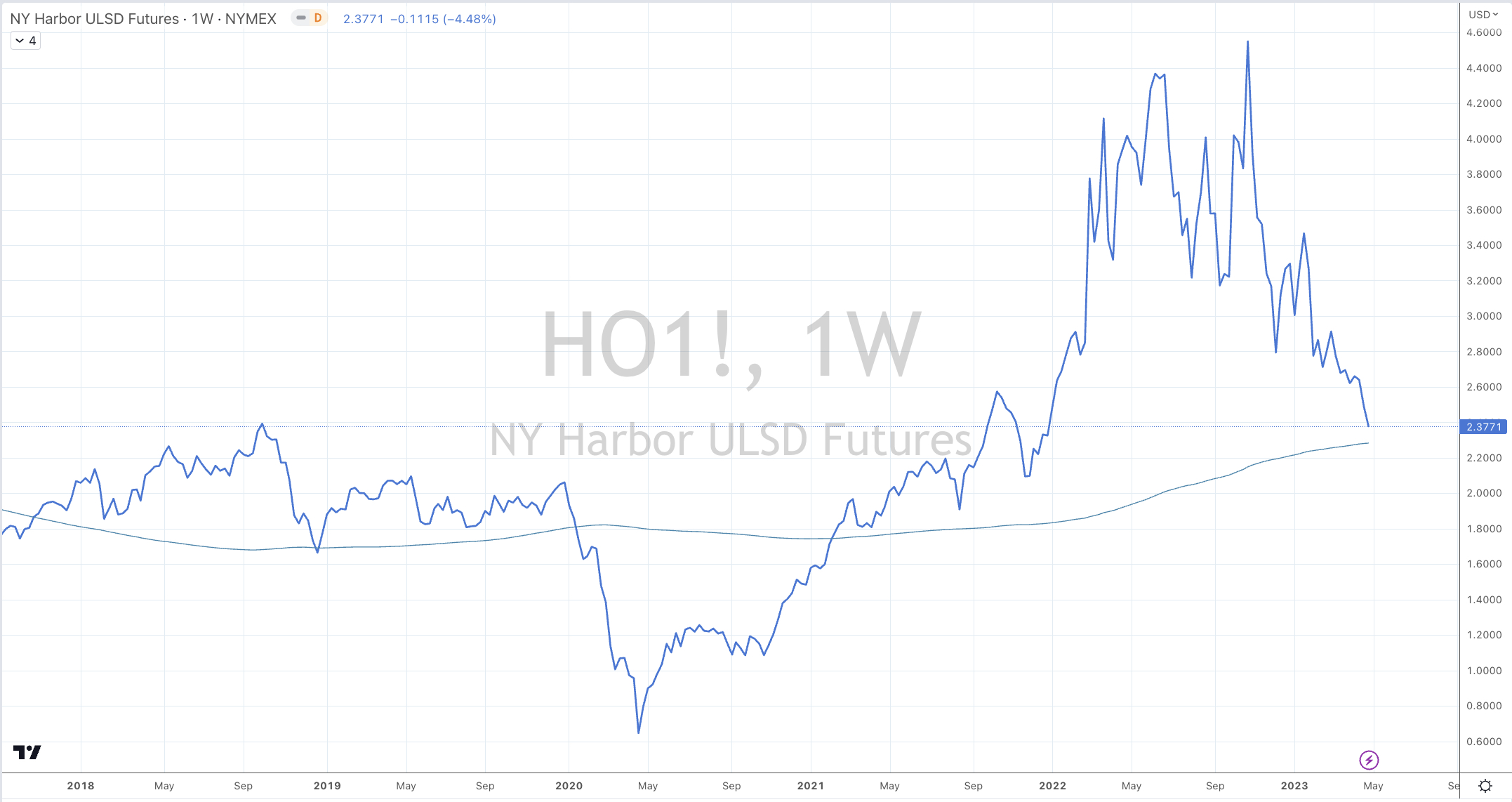

Other observations include, Gasoil (diesel) and Heating Oil are 3% from reaching a long awaited men reversion to its 200 week moving average and Copper broke below a support line.

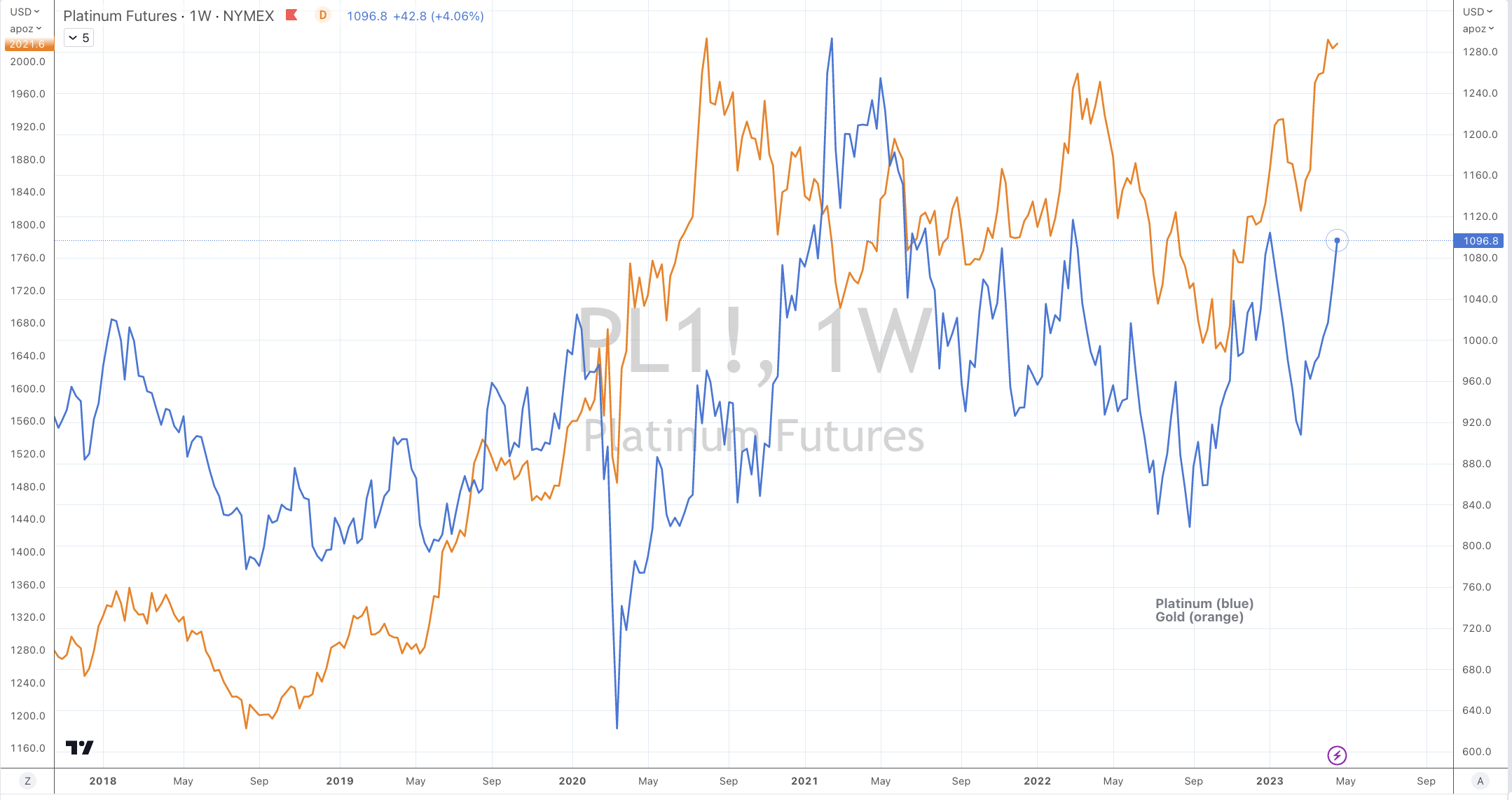

The run in the PGM’s (platinum and palladium) took a breath this past week with the former breaking its 6 week rising streak.

Australian Coking Coal joined the oversold ranks having now seen a 39% decline over the past 5 weeks whilst also mean reverting back to its 200 week moving average.

Corn’s nearest contract fell 12% this past week while the next contract month fell 14%. The pertinent reason for mentioning the subsequent month’s contract this week, is that it registered quinella of oversold readings and it also mean reverted to its 200 week moving average.

And Lumber has closed at its lowest level since mid-May 2020.

Remember all those stories about rising timber prices affecting homebuilding costs?

Euro strength dominated action amongst currencies.

The AUD was weak against most and many currencies which prompts me to say Australian assets are on sale against the GBP and EUR.

While the BRL/USD takes break from trading at an extreme, it continued to strengthen and we also saw the Danish Krone trade into overbought territory against the USD.

The larger advancers over the past week comprised of;

Baltic Dry Index 4.8%, Lean Hogs 3.4%, Natural Gas 7.9%, Sugar 6.1%, Urea (U.S. Gulf) 3.2%, Urea (Middle East) 9%, Gold in AUD 1.5%, Nasdaq 100 1.9%, Sensex 2.4%, Mexico 1.8%, Chile’s Santiago equity index rose 3.6%.

The group of decliners included;

Australian Coking Coal (13.7%), Rotterdam Coal (2.1%), Brent Crude (1.4%), Copper (2.3%), Heating Oil (4.5%), Hot Rolled Coil Steel (9.3%), JKM LNG Gas (2.8%), Coffee (2.9%), Lumber (11.6%), Cattle (4.9%), Lithium (6.6%), Tin (5.7%), Nikkei (5%), Palladium (6.1%), Platinum (4.3%), Gasoline (2.8%), S&P GSCI (1.6%), Dutch TTF Gas (4.1%), Corn (11.8%), Oats (6.5%), Soybeans (2.1%), Wheat (5.8%), KBW Bank Index (2%), DJ Transports (2.7%), MIB (2.4%), IBEX (1.9%), KOSPI (1.7%), Nasdaq Biotech Index (2%) and Thailand’s SET Index fell 1.9%.

The chart below shows a little tuning to this call.

A spurt to 1.1200 (as marked by circles) would see the EUR/USD mean revert upwards to its 200 week moving average, likely register a weekly overbought reading and trade to standard deviations above its rolling weekly mean.

The ASX 200 equity index is the same price as it was 2 years ago.

How are your passive, indexed ETF returns working out?

What if various equity indices are flat for many years to come?

This is also applicable to those index-hugging fund managers too.

(after all, if you stay close to the index, you get to keep your job)

Timing the market (and using probability) is what professional investors apply their skills towards, every day of every year.

At this particular time, I hope investors are not ingesting that old financial services line, “it’s time in the market and not timing the market’.

That line is often accepted by many as an excuse for their lack of attention towards prices and valuations in the capital markets.

Conversely, when it comes to buying or selling residential real estate or the purchase of a car or an airplane ticket, we become suddenly ‘market timers’ and we’ll tell anyone who is listening how good we are.

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

Coffee

Copenhagen

BRL/USD

U.K. 3 years government bond yields

Overbought (RSI > 70)

Cocoa

Hot Rolled Coil Steel (HRC)

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Cattle

Sugar

Russia’s MOEX Index

Extremes “below” the Mean (at least 2.5 standard deviations)

None

Oversold (RSI < 30)

U.S. 5 year bond yield minus U.S. 3 month bond yield

Urea (Middle East)

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Lithium Hydroxide

Notes & Ideas:

Equities generally had quiet week. In Europe they traded slightly higher through the past week, while U.S. and Australian equities ranged from being slightly lower to unchanged. Asian and South American bourses bore the larger losses for the week, with Chile dropping the most as the government plans to nationalise the lithium industry.

Continuing previous weekly commentary, equities are consolidating and broadly remain treadless, although Spain’s IBEX and Switzerland’s SMI did make ‘recent’ higher highs.

Government bond yields moved in the direction that I wrote about last week. They rose modestly across the world except for the Canadians.

With the recent hoo-ha in the bond market, it’s timely to paraphrase a Kipling adage, ‘keeping one’s head while others are losing theirs’.

Several weeks ago, the U.S. 2 bond was yielding 5.08%. It then tanked to 3.56% and is now trading at 4.20%, which is close to being at the mid-point of those highs and lows.

Overall Commodities traded quietly with a bias for lower prices with energy and copper and soybeans leading the way while metals (industrial and PGM’s) saw strength.

The PGM’s (platinum and palladium) have had a stellar run while Australian Coking Coal prices have declined 25% over the past 4 weeks.

Last week’s overbought orange juice along with gold and silver (as priced in AUD) are no longer so.

The currencies which were at extremes last week, are not anymore.

The U.S. Dollar was slightly firmer (amongst media noise discussing its demise), enough so to lift it out of oversold territory.

The AUD was weaker against the EUR and GBP, while the BRL continues to weaken against the USD.

The larger advancers over the past week comprised of;

Rotterdam Coal 2.5%, Baltic Dry Index 4.8%, Cocoa 3%, China Coal 13.2%, Lumber 2%, Tin 13.6%, Natural Gas 5.6%, Nickel 6.7%, Palladium 7.4%, Platinum 8%, Sugar 3%, MOEX 3.2% and the Nasdaq Transports rose 2.1%.

The group of decliners included;

Australian Coking Coal (3.7%), Bloomberg Commodity Index (2.1%), WTI Crude (5.6%), Gasoil (6.2%), Lean Hogs (4.3%), Copper (3.1%), Heating Oil (5.7%), JKM LNG (6.3%), Lithium (2.1%), Gasoline (8.3%), S&P GSCI (3.5%), CRB Index (2%), Cotton (3.3%), Dutch TTF Gas (2.4%), Brent Crude (5.8%), Soybeans (3.4%), Rice (1.5%), CSI 300 (1.4%), HSCEI (2.2%), Hang Seng (1.8%), BOVESPA (1.8%), Helsinki (2.1%), TAIEX (2.1%), SET (2.2%) and Chile fell 3.5%.

For reference, Australia’s Small Cap fell 1.1%, the ASX 200 eased 0.4% lower, Toronto’s TSX rose 0.6%, the Dow Jones Industrials and S&P 500 were almost unchanged with slight declines of 0.2% and 0.1% respectively, the Nasdaq Composite and 100 correspondingly lost 0.4% and 0.6%, the Philadelphia SOX Index slumped 1.6% whilst the Dow Jones Transport Index climbed 1.2% for the week.

Keep in mind that when I review my market calls it is not to resemble any bragging. My posts are meant to be a digital record of my views and I fairly review the good and bad decisions here.

I did think this was quite a prescient call, although it’s not so much whether one sold but it more of a ‘flag’ when not to buy.

Today, the FTSE has risen nicely from that mid March low yet it hasn’t traded above that February 23, 2023 price and its trend isn’t exhibiting the correct traits of strength.

I’m aware that sampling a 2 month window is hardly considered a lengthy period for many investors, but I’ll argue that taking risk and being exposed (with meaningful percentages) to the FTSE 100 over that time wasn’t the best risk adjusted strategy.

Today, with it’s stock price trading at $7.04, Australian copper mining company, Sandfire Resources (SFR.AX) is approaching a moment where probability tells me to sell its shares soon. *

The chart below shows 3 notable (recent) moments when Sandfire Resources stock price was trading at the upper end of various extreme measures. It is also at stretched percentages above its 200 week moving average.

In July 2022 (9 months ago), I posted a note which observed the ‘extreme’ low in its share price. The stock was trading around the A$3.80 mark then.

…..which mentioned the first bid BHP made for Oz Minerals and showed other stocks that created the same buy signal during that month of July 2022.

For as long as the business isn’t broken and the theme remains intact, it takes some fortitude to accumulate equity when all around you seems dire.

Incidentally, the stock price of Sandfire Resources correlates well with the price of Copper……and Copper correlates closely with other currencies, inflation, bond yields and gross domestic product readings.

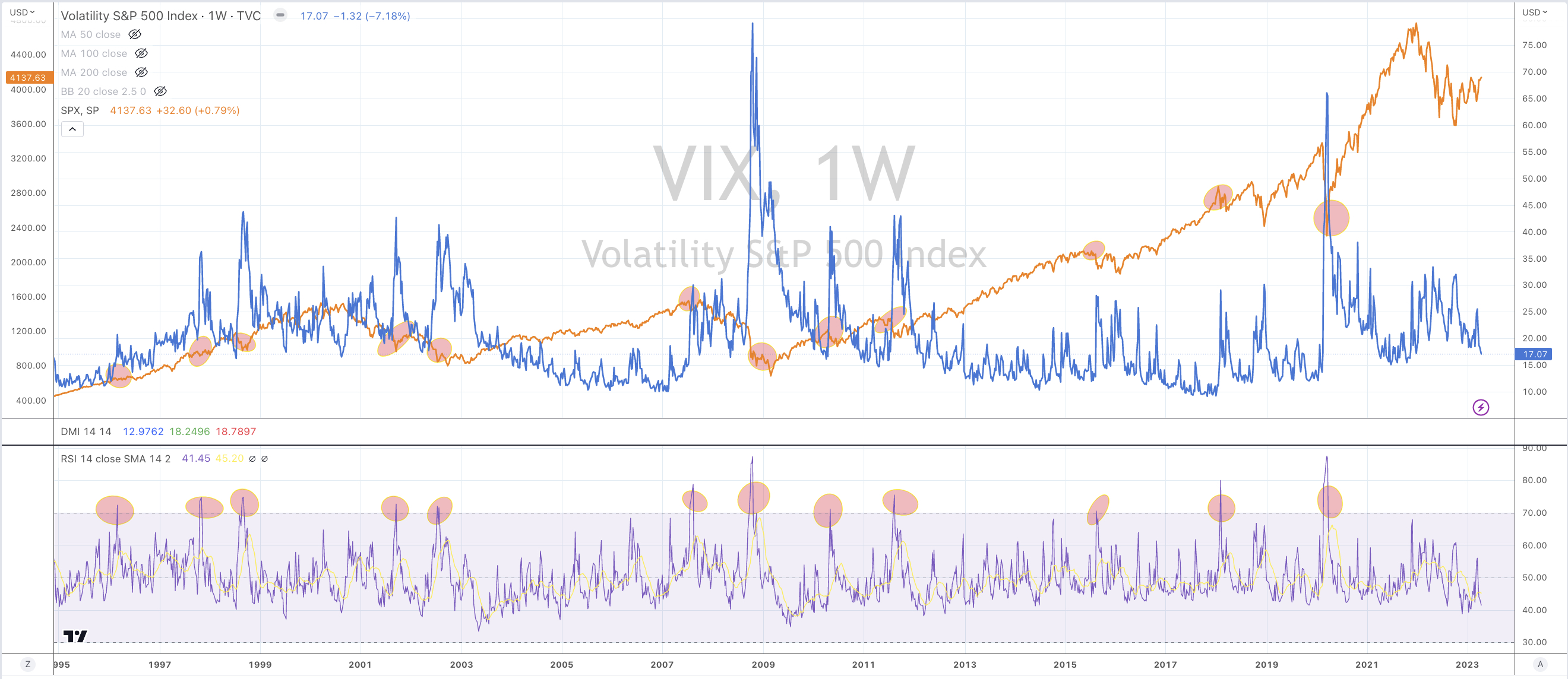

Over the past 30 years, here are 12 moments when the VIX was overbought on a weekly basis and how it corresponded to an adequate signal to accumulate the ‘market’, or the S&P 500 (orange line) in particular.

I don’t use this study in isolation but it’s a handy cross-referencing tool.