A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

British 10 year government bond yields

Overbought (RSI > 70)

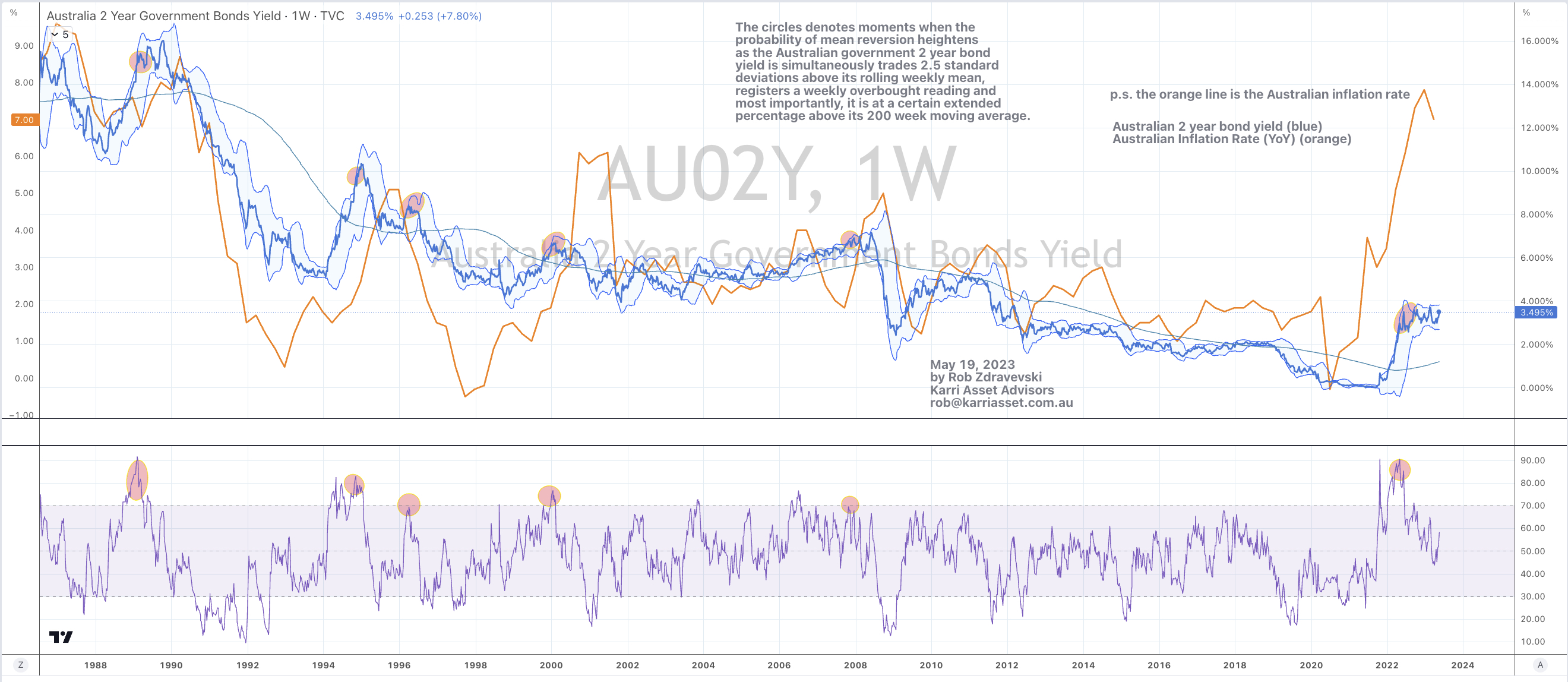

Australian 3 month bank bill yield (90 day swap rate)

U.S. 3 month government bond yield

Cocoa

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Nikkei 225

Extremes “below” the Mean (at least 2.5 standard deviations)

China 10 year government bond yields

Copper

Oversold (RSI < 30)

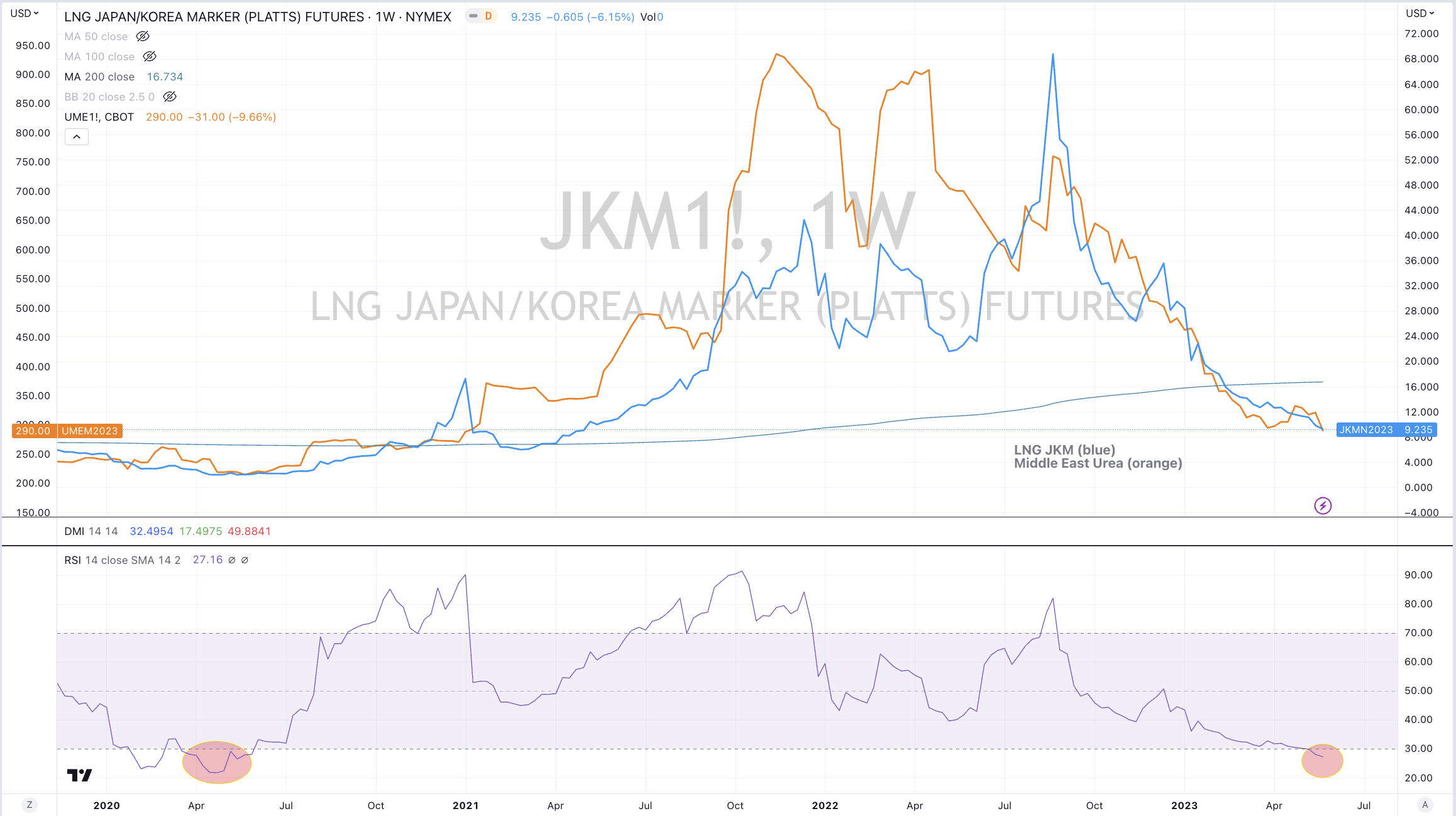

JKM LNG Gas

Lithium Hydroxide

KRE Regional Bank Index

ZAR/USD

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Corn

Soybeans

Notes & Ideas:

Equities showed life following weeks of sideways travel. The moves can’t be described nor confirmed as a new trend or the ‘rip’ higher, the latter being something I have written to clients about recently.

While it’s worthy to note many equities markets are yet make any type of ‘higher high’.

The KBW Bank index rose 6% for the week, more than reversing last weeks 3.5% decline and it’s no longer oversold.

While last weeks bearish outside reversal seen in South Korea and Taiwan didn’t materialise into weakness.

For the week, the ASX 200 rose 0.3% and the ASX Small Caps fell 0.9%.

Government bond yields generally rose, except for Türkiye’s.

In this weeks list, the British 10’s entered an overbought territory while the other 2, 3 and 5 year durations are nearly doing the same.

And the U.S. 5 year bond yield minus U.S. 3 month bond yield isn’t oversold this week.

Commodities were broadly higher with energy generally faring well while the ‘softs’ (agriculturals) suffered the largest declines along with Tin and Nickel.

Sugar is no longer overbought nor is Gold as it is priced in AUD.

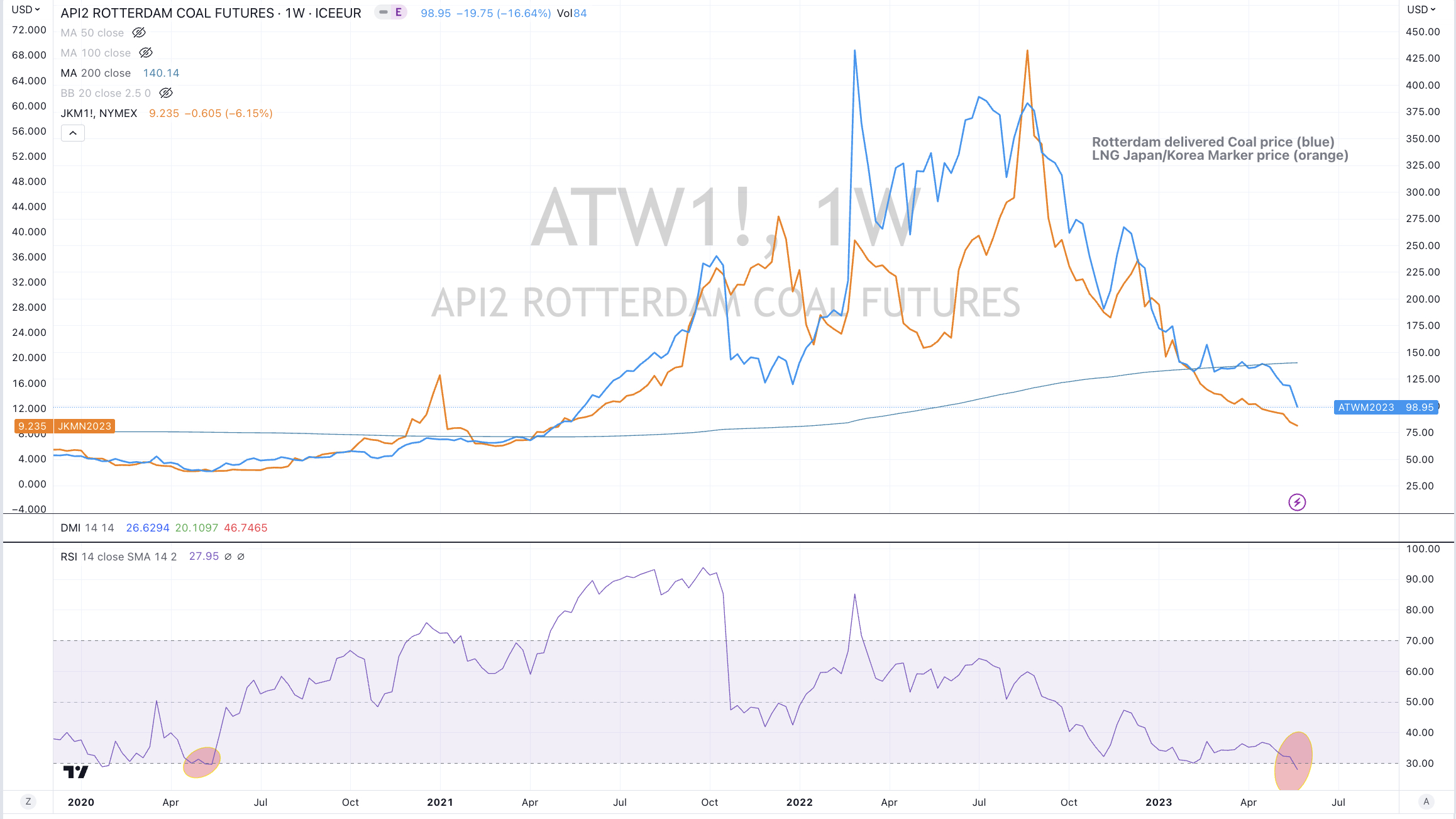

Australian Coking Coal is closing in on its 200 week moving average.

JKM LNG continues to close at its lowest point in 3 years and Heating Oil broke its 7 week losing streak.

Currencies

We saw the AUD mixed, the EUR slightly weaker while the USD broadly firmed.

The USD/JPY is edging towards an overbought extreme.

The larger advancers over the past week comprised of;

Cocoa 2.8%, Aluminium 2.8%, WTI Crude 2.4%, Iron Ore 3.3%, Gasoil 3%, Heating Oil 2.5%, Coffee 5%, Lithium 3.7%, Natural Gas 14.1%, Orange Juice 6.4%, Gasoline 6%, CRB Index 1.6%, Cotton 7.7%, Brent Crude 2.2%, AEX 1.9%, KBW Bank Index 5.8%, DAX 2.3%, BOVESPA 2.1%, Nasdaq Composite 3%, KOSPI 2.5%, Nasdaq 100 3.5%, Nikkei 4.8%, Stockholm 2.3%, Russell 2000 2%, S&P Small Cap 600 2.4%, SOX 7.8%, S&P 1.7%, TAIEX 4.3% and the KRE Regional Bank Index soared 7.8%.

The group of decliners included;

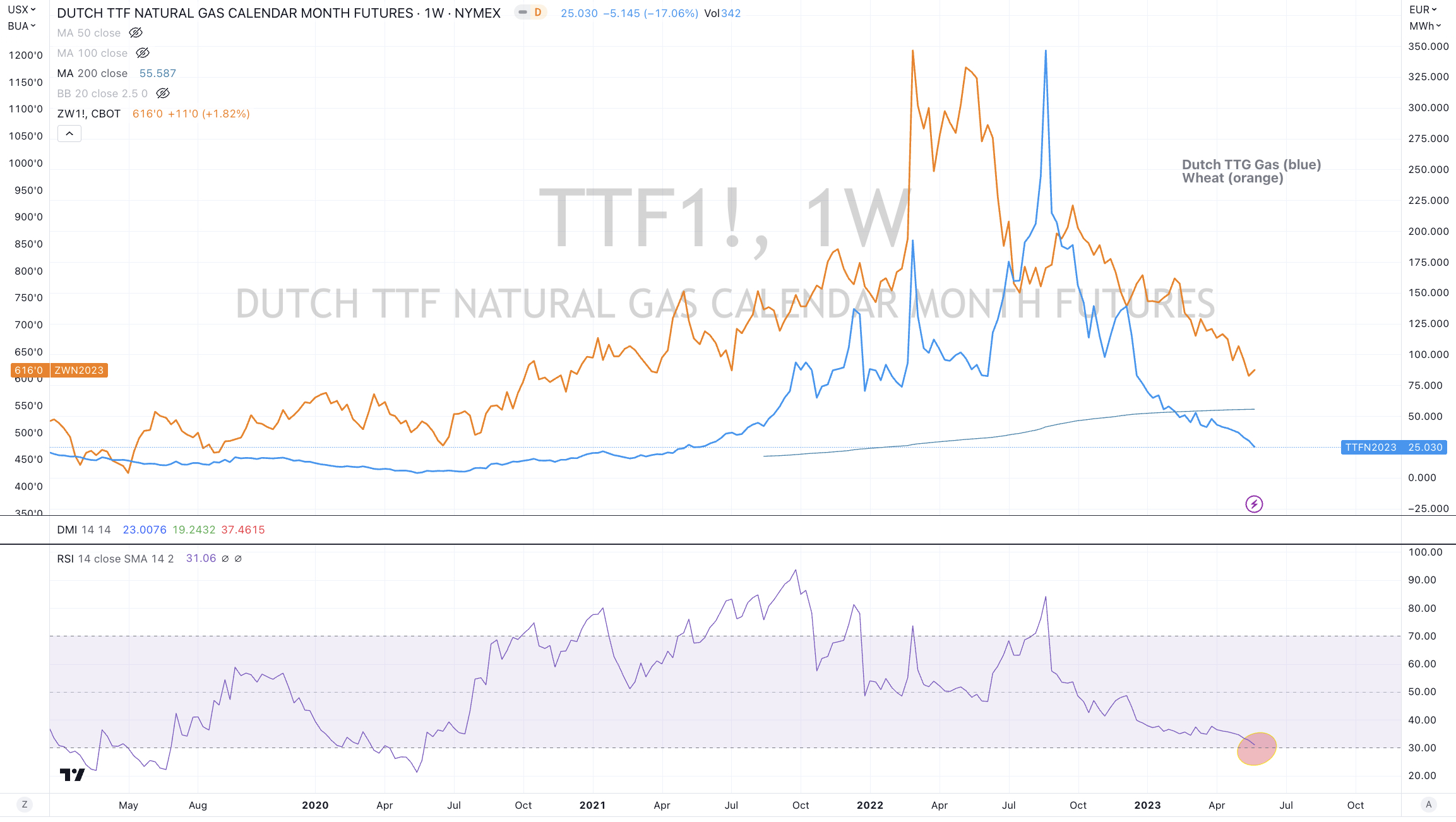

Baltic Dry Index (11.2%), JKM LNG (11.5%), Tin (5.2%), Nickel (4.3%), Sugar (1.7%), Dutch TTF (7.9%), Gold in AUD (1.8%), Gold in CAD (2%), Corn (5.4%), Oats (3.9%), Rice (7.7%), Soybeans (6%), Wheat (4.7%), Lumber (1.8%) and Thailand’s SET Index fell 3%.

May 21, 2023

by Rob Zdravevski

rob@karriasset.com.au