A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

U.S. 20 year government bond yields

U.S. 5 year minus U.S. 5 year inflation break-even rate

Chilean equity index

Overbought (RSI > 70)

Russia’s MOEX index

Nasdaq 100

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

British 2, 3, 5 & 10 year government bond yields

Australian 3 month bank bill yield (90 day swap rate)

U.S. 3 month government bond yield

Nikkei 225

Philadelphia Semiconductor Index

Extremes “below” the Mean (at least 2.5 standard deviations)

TLT (U.S. Treasury 20+ year bond ETF)

CSI 300 equity index

Copper

Soybeans

Oversold (RSI < 30)

LNG Japan Korea Marker (JKM)

Lithium Hydroxide

Dutch TTF Gas

Rotterdame delivered Coal

KRE Regional Bank Inde

ZAR/USD

The Oversold Quinella – Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

None

Notes & Ideas:

Equity Indices mainly experiencedlower prices but they were eclipsed by the noisy gains in tech stocks and rebounding U.S. banks.

Beside the list of notable gainers and decliners below, the Dow Jones Industrials fell 1%, the MidCap 400 eased 0.5%, the SmallCap 600 and Russell 2000 eeked a 0.1% gain with the S&P 500 rising 0.3% for the week.

This past week, some equity markets did make a new ‘higher high’. Markets still have a propensity to ‘rip’ higher.

The Nasdaq 100 and the SOX both registered an overbought extremes for the first time since November 2021 while the Nikkei 225 last visited this area in March 2021.

The SOX Index has now risen 18% in the past 2 weeks, the U.S. Regional Bank Index has climbed 11% and the Nasdaq 100 firmed 7% over the same time whilst the S&P 500 is still hovering around the same price as January 2023.

For the week, the ASX 200 fell 1.7% and the ASX Small Caps fell 2.9%.

Government bond yields generally rose (except for Brazil and Türkiye) again and are trending higher. So, I ponder if they make a double or triple top. I’ll watch for ‘higher highs’.

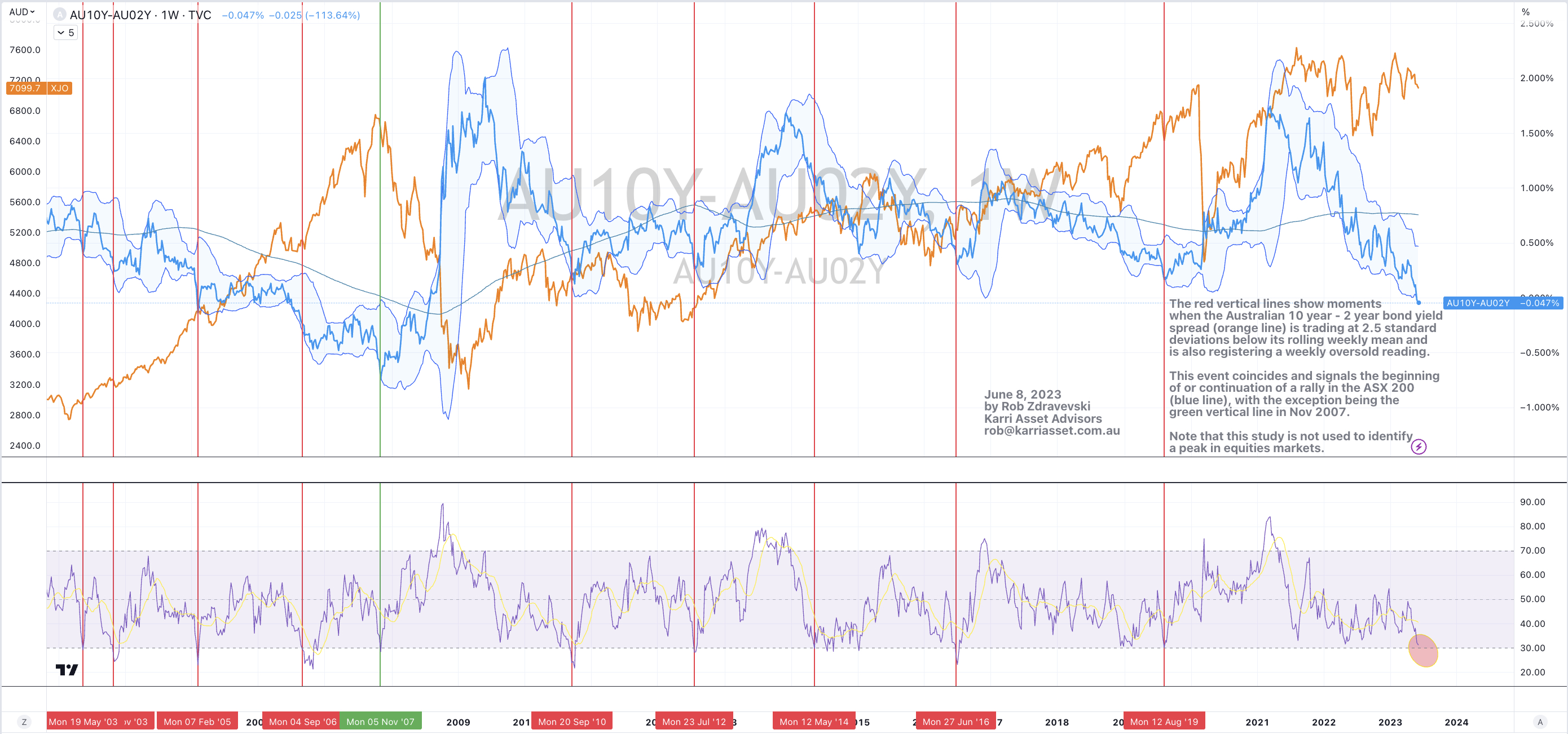

The Australian 10 year minus 2 year bond yield spread is nearing an oversold reading. This week was its lowest close since October 2010. Preceding that, the same percentage was seen in September 2008.

All the durations of British Gilts are overbought.

The U.S. 3 month yield has seen its highest close “in this cycle” at 5.32%.

The last time one could’ve earned near this interest rate was when it traded at 5.14% in February 2007.

Before that, it traded at 5.38% on January 1, 2001. Merely, 23 years ago.

Brazilian 10 year bond yields are nearing oversold territory but more relevant is that the yield has eased from 13.6% to 11.6% over the past 3 months.

Relevant because Brazil was amongst the first central banks to start their hawkish inflation strategy.

Commodities were broadly weaker while oil and softs bucked the trend firming through the week.

Coal, Urea, Gas and Shipping rates were amongst the notable decliners.

JKM LNG continues to close at its lowest point in 3 years and Australian Coking Coal finally mean reverted.

Dutch TTF Gas entered weekly oversold territory for the first time in 3 years.

Cocoa and Sugar are no longer overbought.

Nickel has now fallen 13% over the past 3 weeks and Silver has declined 10% over the same time. Whilst over the past 2 weeks, the Baltic Dry Index has tanked 26%, Dutch TTF Gas slumped 25% and JKM LNG has sunk 17%. Inversely, Orange Juice has climbed 20%.

Currencies

The AUD lost 2% of its value against the USD and it was weak against everyone else including the Rupiah and Rupee.

Inversely, the USD saw strength. Recall those media reports (once again) about the death of the U.S. Dollar.

The Malaysian Ringgit is nearing an Oversold moment agains the USD.

The South African Rand closed at lowest historical price versus the USD and the AUD.

The Chinese Yuan is weaker as it nears an oversold reading.

The larger advancers over the past week comprised of;

WTI Crude 1.4%, Orange Juice 13.1%, Brent Crude 1.7%, Corn 8.9%, Oats 6.6%, Soybeans 2.3%, Wheat 2%, MOEX 2.1%, Nasdaq Composite 2.5%, SOX 10.7%, TAIEX 2%, KRE 2.8% and the Nasdaq 100 rose 3.6%.

.

The group of decliners included;

Australian Coking Coal (2.1%), Aluminium (2.5%), Rotterdam Coal (16.6%), Baltic Dry Index (15.3%), Cocoa (2.5%), China Coal (4.3%), Iron Ore (2%), Lean Hogs (8.4%), JKM LNG (6.2%), Coffee (5.4%), Natural Gas (6.5%), Nickel (2.5%), Palladium (6.6%), Platinum (4.4%), Silver (2.9%), Cotton (3.9%), Dutch TTF Gas (17%), Urea U.S. Gulf (14.9%), Urea Middle East (9.7%), Lumber (2.9%), Shanghai (2.2%), CSI 300 (2.4%), CAC (2.3%), DAX (1.8%), MIB (2.9%), HSCEI (4%), Hang Seng (3.6%), Nasdaq Biotech’s (2.6%), TSX (2.1%), KLSE (1.8%) and the FTSE 100 fell (1.7%).

May 28, 2023

by Rob Zdravevski

rob@karriasset.com.au