A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

Lean Hogs

AUD/JPY

USD/CNH

Overbought (RSI > 70)

British 5 year government bond yields

U.S. 3 month bill yields

Cocoa

Oats

Nasdaq 100

Nikkei 225

And Russia’s MOEX & Taiwan’s TAIEX equity index

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

British 2 & 3 year government bond yields

Extremes “below” the Mean (at least 2.5 standard deviations)

Coffee

Oversold (RSI < 30)

Brazil 10 year government bond yields

Lithium Hydroxide

Newcastle Coal

Urea (Middle East)

CNH/USD

MYR/USD

The Oversold Quinella – Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

Australian 10 year minus 2 year bond yield spread

Notes & Ideas:

Equities were lower across the globe.

Most of the index losses over the past erased the previous 2 weeks of gains.

The Nasdaq Composite isn’t overbought this week while the more concentrated Nasdaq 100 remains so. The former snapped its 8 week winning streak.

Japan’s Nikkei 225 also saw an end to its gravity defying 10 consecutive week of gains.

The S&P 500 and the SOX has eased away from overbought territory.

The KRE Regional Bank Index fell 8% this past week to see it close at the same price seen a month ago. Since its May 12th close, it has risen 8% in total.

We saw many indices registers declines of 2% or more over the week, although the Nasdaq 100 and S&P 500 ‘only’ declined 1.4%.

Worthy to watch is the bearish outside reversal week that Australia’s (XSO) Small Cap index registered.

Most Government bond yields fell.

Swedish, British and shorter duration American yields were the exception.

The U.S. 2’s saw their highest closing yield in 4 months but are not making a ‘higher high’.

While the U.K. 2’s and 3’s did make ‘recent’ higher highs and have achieved their highest yields since July 21, 2008.

Australian 10 year yield minus U.S. 10 year yield and Australian 2 year government bond yields are no longer overbought

The U.S. 3 month bill yield made a return to overbought territory.

The U.S. 10 year minus U.S. 5 year yield spread registered its 7th consecutive ‘losing’ week.

The more ‘watched’ US10Y-US02Y is nearing oversold levels.

My obscure yield spread such as the U.S. 10 year bond yield minus Australian 10 year bond yield and the U.S. 10 year bond yield divided by Australian 10 year bond yield aren’t at any standard deviation lows.

The Australian 2 and 3 yer bond yields broke their streaks of 7th consecutive rising weeks with the latter recently seeing its highest yield since August 1st, 2011.

The Japanese 10 year bond yields closed at their lowest in 3 months.

Commodities were mostly weak.

Wheat, Rice, Lumber, Urea and Gas bucked that trend. The latter continue their advance from their recent oversold depths.

Energy contracts broadly erased the past 2 weeks of gains.

Agricultural’s either rose or held up well.

Copper erased last week’s gains.

Precious Metals continue to perform poorly.

Over the past 2 weeks, WTI Crude Oil has now lost 6%, Orange Juice has eased 11% and Palladium has sunk 17%, while Lumber has risen 10%, Wheat climbed 18% and Natural Gas has soared 21% over the same time.

Palladium and Aluminium are nearing oversold levels and Platinum has fallen 19% over the past 2 months.

Uranium, Cattle and Sugar aren’t overbought anymore. The latter produced a bearish outside reversal week.

And Silver has mean reverted to its 200 week moving average.

In Currencies, we saw a reverse of last week’s ‘risk on’ form.

The AUD/JPY trading at an extended 2.5 standard deviations portends a peak in ‘risk taking’. Keep watching this currency cross if it make makes a quinella with an overbought RSI reading to possibly gives a more notable peak in ‘risk’.

The AUD gave up all of last week’s 2% gain and more, depending on the currency cross you are looking at.

The Aussie lost 3% agains the CAD and USD.

The Kiwi/Aussie (NZD/AUD) registered a bullish outside reversal week.

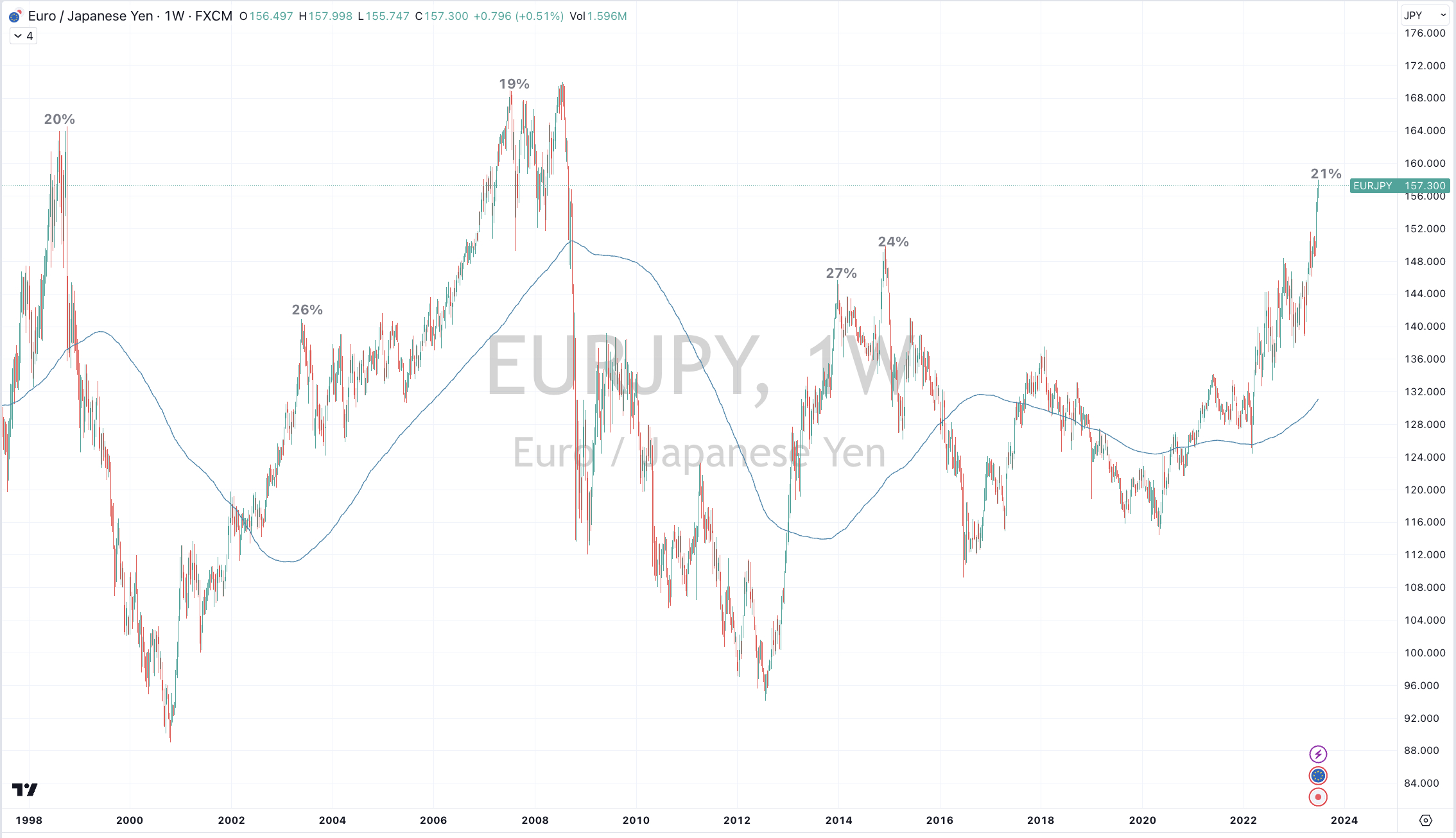

The USD saw its highest close agains the JPY since October 31, 2022. The USD has now risen 10% against the Yen over the past 3 months.

And the USD rose 3% versus the South African Rand (ZAR).

The larger advancers over the past week comprised of;

Baltic Dry Index 15.2%, JKM LNG 5.7%, Lumber 6.6%, Lithium 2.5%, Natural Gas 3.7%, Urea U.S. Gulf 3.3%, Rice 1.6% and Wheat rose 6.4%.

The group of decliners included;

Aluminium (3.7%), Bloomberg Commodity Index (2.7%), Brent Crude (2.5%), China Coking Coal (2.1%), WTI Crude Oil (3.9%), Gasoil (4.7%), Copper (2.2%), Heating Oil (5.7%), Coffee (8.8%), Nickel (5.6%), Orange Juice (2.9%), Palladium (9.7%), Gasoline (6.1%), Sugar (8.5%), Silver (7.3%), S&P GSCI (2.8%), CRB Index (2.9%), Cotton (2%), Dutch TTF Gas (7.1%), Silver in AUD (4.5%), Gold in CAD (2%), Gold in USD (1.9%), Corn (1.5%), Soybeans (2.4%), Shanghai (2.3%), CSI 300 (2.5%), AEX (2.1%), KBW Bank Index (5%), CAC (3.1%), DAX (3.2%), DJ Industrials (1.7%), MIB (2.3%), HSCEI (6.4%), Hang Seng (5.7%), IBEX (2.4%), Nasdaq Composite (1.4%), KOSPI (2.1%), S&P MidCap 400 (2.5%), Nasdaq Biotech (2.1%), Nikkei (2.7%), S&P SmallCap 600 (3.1%), Oslo (4.2%), Copenhagen (3%), Helsinki (6.2%), Stockholm (3.8%), Russell 2000 (3%), SOX (4.5%), STI (2.1%), TSX (2.8%), FTSE 100 (2.4%), ASX 200 (2.1%), ASX SmallCaps (3.5%), Mexico (2.7%), KRE Bank Index (8.1%) and Thailand SET Index (3.5%).

June 25, 2023

by Rob Zdravevski

rob@karriasset.com.au