I don’t think the market is about to break but many money managers may.

Peers are speculating whether there are big funds unwinded losing and problem positions.

Perhaps so but that often coincides with the ‘straw which broke the camel’s back’.

Many thought buying government bonds yielding 0.60% for 10 years to be a good bet.

In fact, many thought buying German bonds for a NEGATIVE 0.60% (as shown in orange in the chart below) was somewhat appropriate.

And their reward is………..a 20% loss of capital (with no interest coupon paid), as shown by the blue line of a German Bond (SDEU) ETF.

When you consider that “balanced” funds including those in the pension or insurance business may typically follow a model of allocating 60% of monies to equities and 40% to bonds, they may be double hurting as Germany’s DAX equities Index has fallen 24% from its peak.

That’s the reporting of what happened bit.

Now, many think this is ‘forever’. Many think trends and streaks don’t end, wane or reverse.

Consider the contrarian view to the extremes we are seeing?

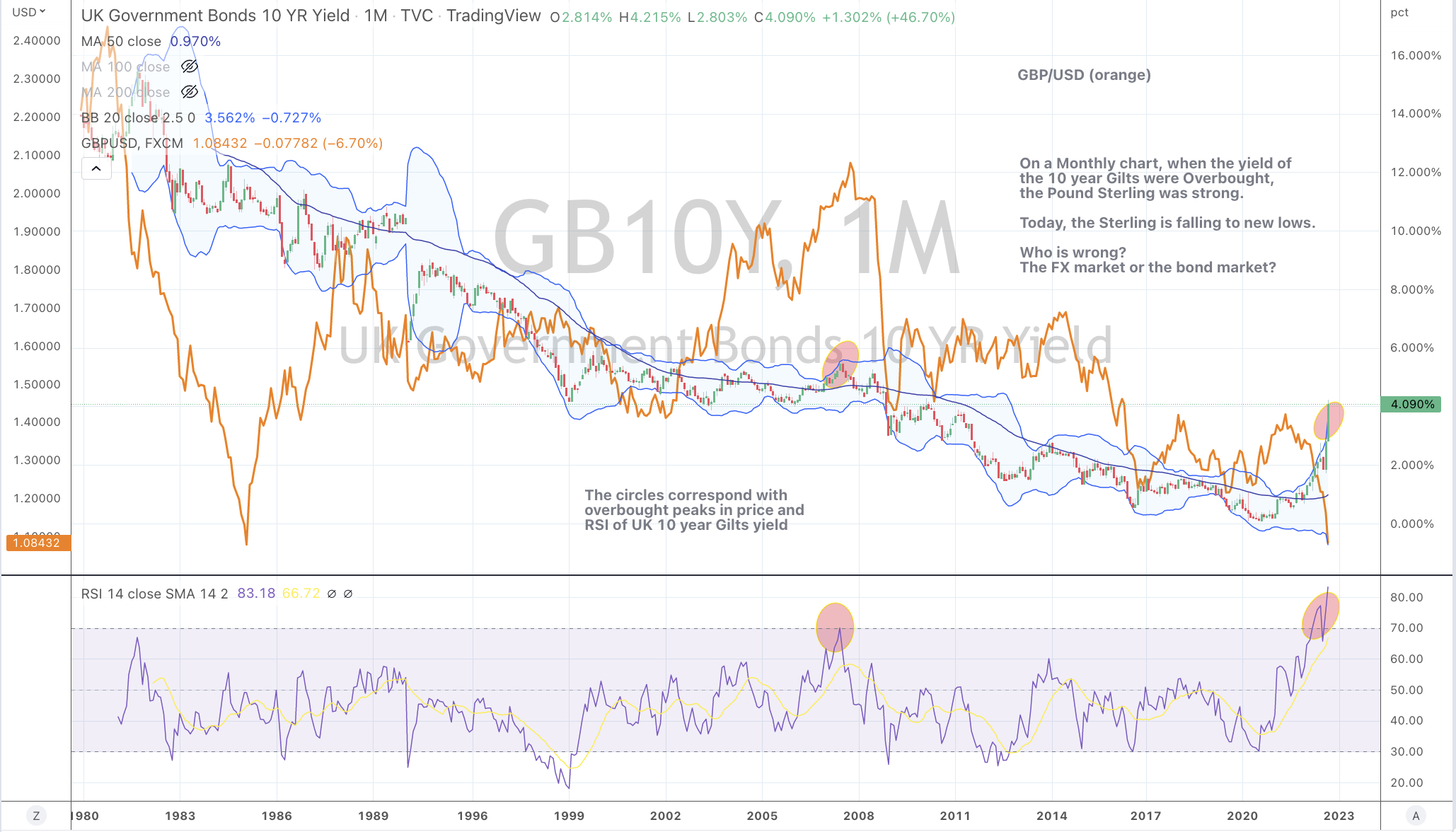

On this Monthly chart, when Gilts yield were Overbought, the Pound Sterling was strong.

Today, Gilts are Overbought BUT Sterling is falling to new lows.

Who is wrong?

The FX market or the bond market?

Whilst FX is the most liquid market, the bond market is more believable.

However, have British economic woes decoupled where this traditional symbiotic relationship of a weak currency and higher bond yields is now resembling what we see in emerging market economies?

Albeit this is a dramatically painted scenario, I don’t think this is the case.

The long term strategy is to Buy British Pounds (GBP).

If you are in the business of needing to own debt, then buying U.K. 10 year Gilts at this juncture (the highest yield seen in the past 12 years) is worth considering.

Inversely, I don’t know why you would initiate a new short at 4.10%?

I haven’t seen any of the ’talking heads’ on business TV suggest shorting Gilts at 0.15% but now they are concurring that it goes higher.

Keep in mind that many are simply ‘reporting’ what is happening today but few seldom make a call identifying the extreme end of the pendulum.

Time will tell but I can’t help think many are doing the wrong thing, at the wrong time.

U.S. year bond yields have never seen 8 consecutive weeks of rising yields. Stocks and Commodities tend to see streaks lose steam in the 7th or 8th consecutive week.

We are closer to the streak ending.

The U.S. 10 year bond yield has never been Overbought on a Monthly basis, until now.

The U.S. 10 year bond yield has never been extended this many percentage points above its 50 month moving average.

The U.S. 10 year bond yield is near to trading up to 2.5 standard deviations above its rolling monthly mean for only the 5th instance in 40 years.

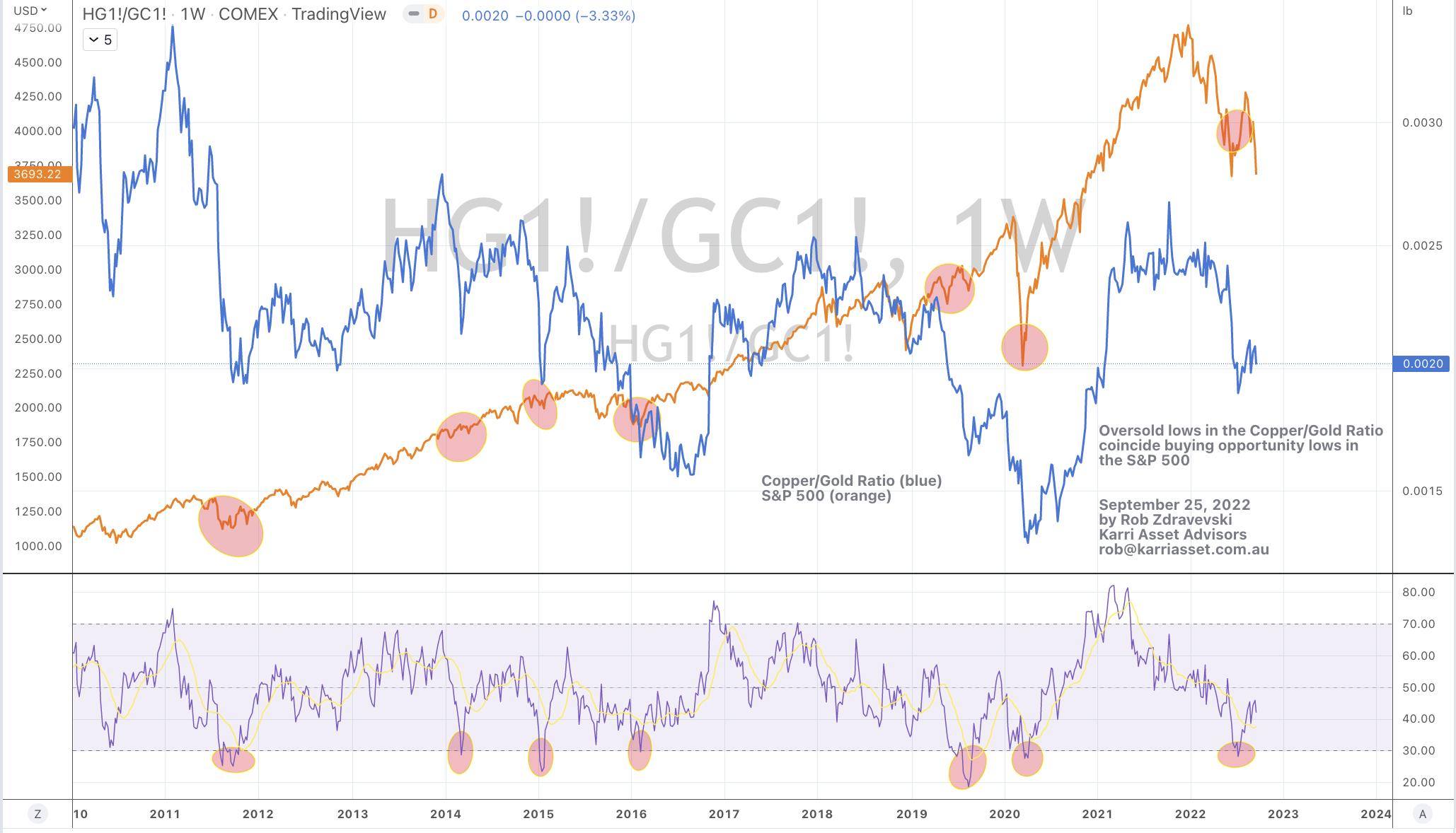

In early July 2022, the Copper/Gold Ratio registered its 7th weekly oversold reading within 12 years.

This occasion coincides with a notable low, or at least safer, longer term buying opportunity in stocks…..or as the chart below implies, in the S&P 500 Index.

In other posts I have mentioned how the monitoring of this ratio is also helpful in tracking the direction of interest rates.

In the meantime, I’ll watch if the Copper/Gold ratio re-visits the oversold region in the coming 3-8 weeks.

The following assets (on a weekly timeframe) registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

Australian 3 year government bond yield

U.S. 10 year minus Australian 10 year bond yield spread

Overbought (RSI > 70)

Greek, Spanish, Portuguese, Italian and U.K.10 year government bond yield

U.S. Dollar Index (DXY)

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

U.S. Dollar Index (DXY)

Australian 2 year government bond yield

U.S. 2. 5, 10, 20 and 30 year government bond yields

German 2, 5 & 10 year government bond yields

French, U.K., Korean and Swedish 10 year government bond yields

TBT & TBX

AUD/GBP

EUR/GBP

Extremes “below” the Mean (at least 2.5 standard deviations)

U.S. 10 yes minus U.S. 5 year bond yield

AUD/USD

CAD/USD

Copenhagen and Helsinki equity bourses

Oversold (RSI < 30)

Tin

Hot Rolled Coil Steel (HRC)

EUR/USD

DKK/USD

JPY/USD

Taiwan’s TAIEX and H.K.’s Hang Seng equity indices

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

GBP/USD

KRW/USD

NZD/USD

SEK/USD

SGD/AUD

IEF, IEI & TLT

Switzerland’s SMI equity index

Notes & Ideas:

The big news for the week is broad.

Government bond yields reached extreme peaks with all of the major U.S. durations doing so.

The CRB (commodities) Index fell 4%.

Equity bourse declined between 4% – 7%.

The fall in equities honoured the preceding weeks observation about Bearish Outside Reversals.

The S&P MidCap 400 and SmallCap 600 have fallen 11% in the past 2 weeks. I had warned that the markets were about to play a cruel trick on those who believed in the previous rally.

A couple bourses went into Oversold territory and TAEIX has done it for the 2nd time within 3 months.

While many bourses complete their mean reversion to their 200 week moving average, such as Copenhagen, CAC, S&P Midcap 400, the SOX……the ASX 200 and Nasdaq Composite have double dipped to their 200 WMA.

The S&P 500 is 108 points (or 3%) away from visiting its 200 WMA. The Nasdaq 100 is 153 points or 1.4% above its 200 WMA. That’s something to watch for this coming week.

Chinese and H.K. indices continued to make lower lows with the Hang Seng (HSI) ‘going’ oversold.

Currencies continue to be in the news, in particular the strength of the U.S. Dollar and the corresponding weakness in others.

The Aussie divergence continues as cited in this post.

So, I’ll watch for how the AUD/USD and WTI Crude symbiotically test their next respective levels of 0.6464 and $77.50, as neither ‘daily’ downtrends are confirming continuing strength.

Hint: probability is rising that we are at the tail-end (+/- 3%-6%) of the downdraft in both assets.

“He {Labor federal Treasurer Jim Chalmers} has warned that the budget cannot rely on temporary revenue windfalls from high export prices for iron ore, coal and gas.”

…..but Australia is heavily reliant on those commodities, their exports and the tax revenues.

This plays into the pragmatic comments Greg Sheridan made in his article titled “Our Climate Fantasy” dated July 30, 2022 (The Australian newspaper).

To paraphrase some of the article,

‘Australia has many projects set to go and it is important that Prime Minister Albanese rejects bans for the commencement of new gas and coal projects’.

“Resources and minerals are irreplaceable in our economy”

“moving to net zero will be expensive and reduce our living standards”

Australia needs to continue to develop its resources to help pay for the running a country this large (in area).

Whilst there is no capital gains garnered from the largest (subsidised) asset class in the country, being owner-occupied residential real estate, revenues from a dwindling individual tax paying base let alone the manufacturing or financial are not enough to cover the gap.

One needs to keep in mind that Australia can’t export solar, wind or hydro energy.

How reliant is Australia on ’these’ commodities?

Of the total credits of goods exported (FY 21-22) being $534 billion, metals ore and minerals ($172bn), coal $113bn), other metals ($14bn) and fuels ($87bn) accounted for $386 billion or 72% of all exports. (source: Australian Bureau of Statistics)

And as reluctance to finance new project grows in lock step with shareholder ESG related pressures, the opportunities lie with the incumbents in those industries.

Climate activists are seemingly unaware of the financial and commercial reality behind notions such as government receipts, or being the lowest cost producer, the cost of building alternative power sources and the need for base load power for the modern world many enjoy.

I don’t think exporting fitness supplements, television programming, insurance or financial services adds up to much.

p.s. don’t bother replying to me using your laptop, mobile phone or internet connection let alone physical mail for it all requires some form of hydrocarbon, silver, silica, copper, chemical….in order for the message t0 be constructed and sent. If you are reading this, you are likely to be utilising many or all of those components.

Ahhhh…is carrier pigeon considered animal cruelty?