Working From Home is the real risk for institutionalised employees

I wonder if the majority of people losing their jobs at Blackrock, Goldman Sachs or Morgan Stanley were the ones who chose more work/life balance than the rest by insisting to work from home?

Once upon a time, sackings were often based on last in, first out.

Perhaps now it based on one’s proximity to the office and collegiately?

In sport, if you sit far away from the bench (and possibly goofing around) the coach won’t see you readily.

But if you stand close to the coach throughout the game, there is a much better chance of being put in the game…….or even being promoted.

Especially, if you are seen to be interested and even periodically ask to be ‘put in the game’.

There is nothing like a bunch of hubris and a good recession to fix the labour market.

Listed Australian gold equities have had a stellar run, especially in the past month or so.

However, I have been a seller and not initiating any new buys.

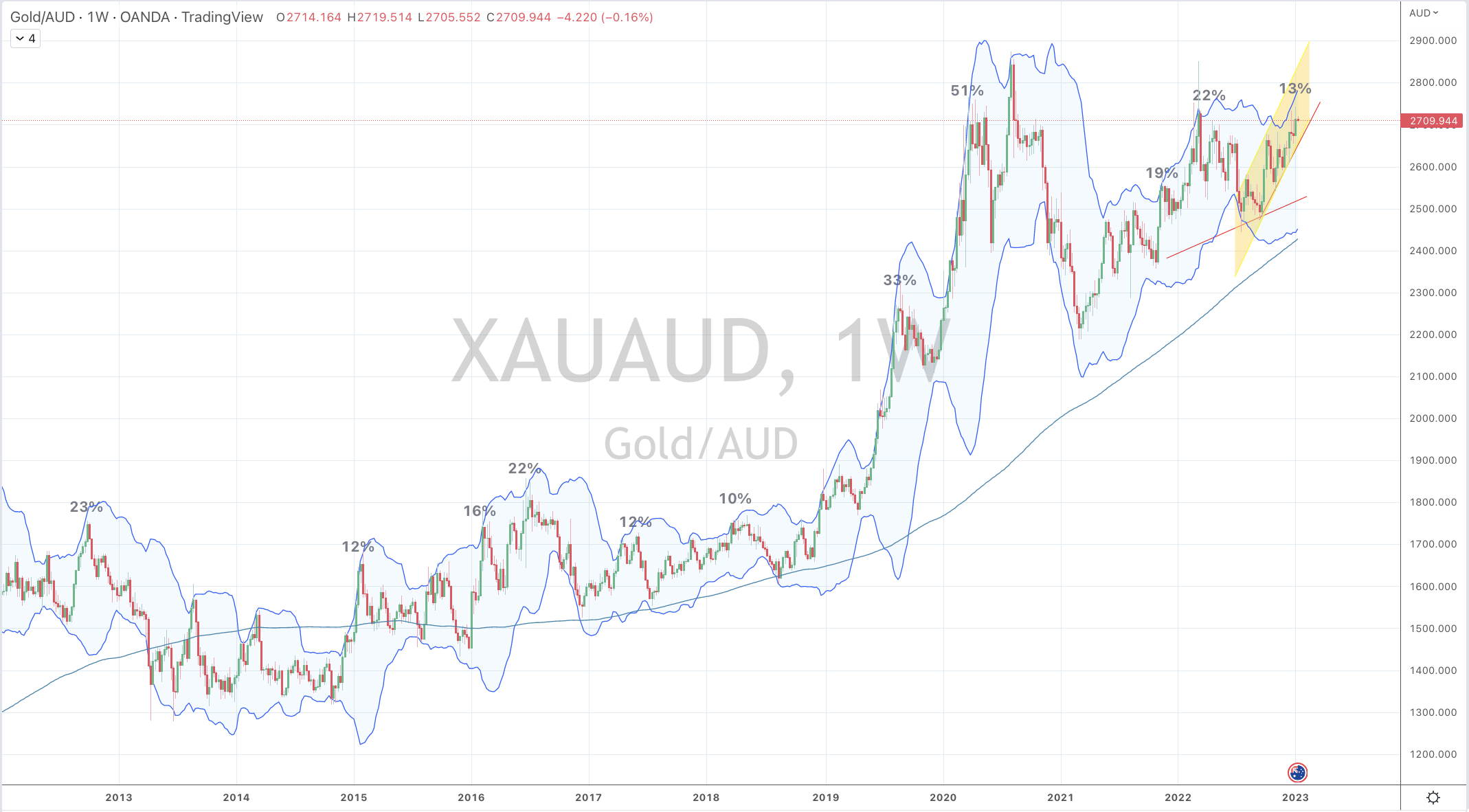

Albeit the Australian Dollar (AUD) Gold price has been acting well as it has been making higher lows and higher highs, some context is required.

Since December 1, 2022, the AUD Gold price has only risen 2.4%, (as the shorter time frame chart illustrates below) while some gold related equities have risen 15%-20% over the same time. The excitement doesn’t quite correlate.

For more context, the AUD Gold price has traded within a 9% band for the past 12 months.

Now, if I zoom out and place the recent ‘spike’ in perspective, the AUD Gold price is beginning to trade near 2.5 standard deviations above its weekly mean and trading at 13% above its 200 week moving average. In the second chart below, I’ve denoted other historically ‘stretched’ moments.

Incidentally, Gold priced in Canadian Dollars is exhibiting ‘greater’ Overbought tendencies.

This is a story about knowing where the pendulum is and not necessarily lamenting about missing out on the last 20% or selling too early, as I have indeed done. Regarding the latter, I do tend to enter too early and sell early. Its part of my philosophy of enjoying the ‘fat part of the trade’.

I think anyone acquiring gold assets priced in AUD at current levels (whether bullion, listed equity or exploration tenements) isn’t getting a bargain but instead falling victim to a smaller scale of FOMO.

In the coming weeks, I’ll be watching for any news relating to ‘insiders’ selling shares and whether specific stocks make higher highs

The larger warning is that there are ‘gaps’ below in many trading charts which typically get ‘filled’ at some time.

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities

The following assets (on a weekly timeframe) registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

None

Overbought (RSI > 70)

German 2 year government bond yields

Gold (in Canadian Dollars)

Cattle

Istanbul’s BIST Index

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Japanese 10 year bond yield

Extremes “below” the Mean (at least 2.5 standard deviations)

U.S. 5 year yield minus U.S. 3 month bill yield spread

Oversold (RSI < 30)

Urea (U.S. Gulf)

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Turkish 10 year government bond yields

Notes & Ideas:

This week’s biggest news was the stunning rally in equities, mainly seen in Europe.

So much so, the U.K’s FTSE 100 closed at its highest level since late July 2018.

Encouragingly, the U.S. small and mid caps outperformed the large cap indices.

Bond yields mainly fell, meaning bond prices rose as they caught a bid.

This means we bond prices rising while equities were doing the same.

Amongst the currencies, I’m seeing continued strength in the Korean Won, the Singapore Dollar and the Japanese Yen versus the USD, as they swing towards the other end of the pendulum. I recall their weakness 3 months ago.

The AUD/GBP continued its rise following a recent outside bullish weekly reversal.

In commodities, Lean Hogs mean reverted to their 200 week moving average.

Australian Coking Coal prices have risen 20% in the past 2 weeks.

Energy prices resumed/continued their decline. Natural Gas prices have fallen 30% in the past 2 weeks.

Grains saw weakness as they near Oversold levels

And the Baltic Dry Index slumped 25% as it attempts to re-test the August 2022 lows. (see the chart below)

I’ve got some correlations to study relating to these commodities.

The larger advancers over the past week comprised of;

Australia Coking Coal 8.2%, Copper 2.6%, Platinum 2%, Cotton 2.8%, Uranium 2.6%, Gold 2.3%, Shanghai 2.2%, CSI 300 2.8%, AEX 5.1%, KBW Banking Index 4.4%, CAC 6%, DAX 4.9%, DJ Transports 3.6%, MIB 6.2%, HSCEI 6.5%, HSI 6.%, IBEX 5.7%, KOSPI 2.4%, S&P MidCap 400 2.6%, Nasdaq Biotech 1.8%, Helsinki 3%, Stockholm 4.6%, Russell 2000 1.8%, S&P SmallCap 600 2.4%, SMI 3.9%, SOX 4.1%, TAEIX 1.7%, TSX 2.2%, FTSE 100 3.3% and Australia’s Small Cap Index rallied 3.2%.

Incidentally, the Dow Jones Industrials and the S&P 500 rose 1.5%, while the Nasdaq and the ASX 200 both advanced 1%.

The group of decliners included;

Aluminium (5.2%), Rotterdam Coal (9.6%), Bloomberg Commodity Index (4.2%), Baltic Dry Index (25.4%), China Coal (2.2%), WTI Crude (8.1%), Gasoil (4.4%), Lean Hogs (8.5%), Heating Oil (8.8%), HRC (1.9%), JKM LNG (3.6%), Coffee (5.4%), Natural Gas (17.1%), Nickel (3.8%), Gasoline (9.4%), Sugar (5.4%), CRB Index (4.7%), Dutch TTF Gas (8.9%), Urea U.S. Gulf (7.1%), Brent Crude (8.7%), Urea Middel East (4.2%), Corn (3.6%), Oats (6.3%), Rice (3.4%), Soybean (2.1%), Wheat (6.1%), S&P GSCI (6%) while Brazil’s BOVESPA declined 0.7% and India’s SENSEX fell 1.6%.

Henry Hub Natural Gas has now reverted down to its 200 week moving average.

This is quite a mean feat.

Readers of my notes will be aware of the significance I have been placing on the gravitational pull of such long term moving averages especially after seeing wickedly bullish parabolic price moves.

You’ll find my notes calling for lower Gas prices in my notes archive.

Weaker Natural Gas prices will continue to have a negative effect on the share price of related utilities and gas companies, while it’s a positive for industry consumers.

I’m still waiting for Gasoline, Diesel (Gasoil), Heating Oil and Crude Oil to perform the same mean reversion back down toward their respective 200 week moving averages.

The Dutch TTF Gas price is nearly there as is the Japan-Korea LNG Price Marker.

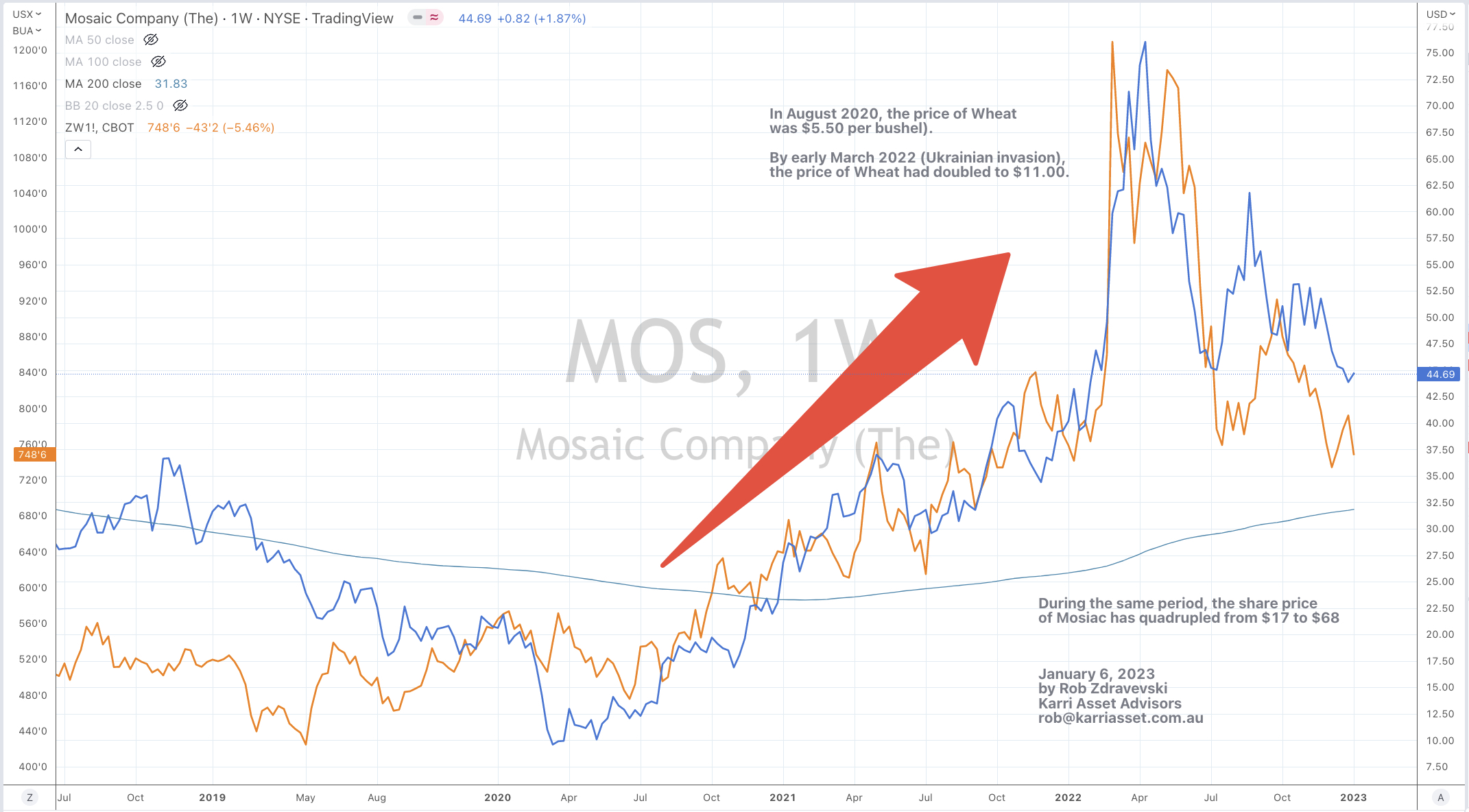

In August 2020, the price of Wheat was $5.50 per bushel).

By early March 2022 (Ukrainian invasion), the price of Wheat had doubled to $11.00.

During the same period, the share price of Mosiac has quadrupled from $17 to $68.

This is a story of correlation and the operational leverage that equities can provide.

It’s also a story about identifying extremes especially at the peaks and respecting mean reversion, particularly following frenzied parabolic price moves.

Now, the price of Wheat and Mosiac Company (one of the world’s largest fertiliser companies) are both trading below pre-Ukraine invasion levels.

Today, I am queuing for Oversold extremes in soft commodities and related sector equities.

My call of WTI Crude Oil visiting $65 still stands.

So, WTI Crude has fallen $9 in the past 2 days.

Now, it’s trading at $73.70

But that’s just reporting the news.

Depending on the strength of the downtrend, the next stop below is ~$62 and failing that, then we may see $54.

(technical trending analysis hint: watch the ADX on the DMI)

Back when Oil was surging to $120, my writings were warning readers to not chase prices higher especially following parabolic price moves and the gravitational pull of long, long term moving averages.

To boot, the price of Oil tracks GDP, it is a large component of inflation readings….and I think that the WTI Oil price leads interest rates.

Keep in mind, that the U.S. 10 yer bond yield was recently 4.33% and now its 3.71%.

To wit, the 10 year bond yield could see 3.30%, if not 2.5% in several months, to latently mimic the Oil price.

So, I say, many had no business buying Oil at $115 nor betting that GDP will expand and the near halving of its price from those highs should be recognised as assisting the moderation of near-term inflation.

While I think $65 is possible, it’s not a time to ‘short’ Oil as such a bet is marginal. Oil may fall $10 or rise $10. Ho hum !!

The fat part of the short trade has been seen.

The preparation is for a low in Oil and then how that relates to other assets and securities.

Apple’s stock price was $143 when I wrote the latest note re-iterating my views on watching the last of the FAANGM (Facebook, Amazon, Apple, Netflix, Google and Microsoft) to fall and mean revert to their 200 week moving average.

Throughout my writings, my FAANGM acronym grew to include Nvidia and Tesla. I’ll call them TFAANNGM ?

Zoltan Pozsar’s research note, titled “War and Commodity Encumbrance” (dated December 27, 2022), will be something I will reference for years to come. Not to judge or critique but rather to remind and guide.

I have previously written about and agree with a paraphrased section where central banks clean up and react to the fiscal policy and geopolitics created by governments, including protectionism and nationalism outcomes.

It comes from the understanding of ‘knowing how the world works’.

While fighting the Fed isn’t advisable, don’t just read and believe the ‘talking heads’ at the central banks, who seem to build a posture that they can or are controlling things. They are just mopping up prior occurrences.