Bargains are starting to appear in equities

October 31, 2023 Leave a comment

How I’m broadly seeing the equities market.

You can subscribe for future editions here

Trying to hear what's not being said

October 31, 2023 Leave a comment

How I’m broadly seeing the equities market.

You can subscribe for future editions here

October 31, 2023 Leave a comment

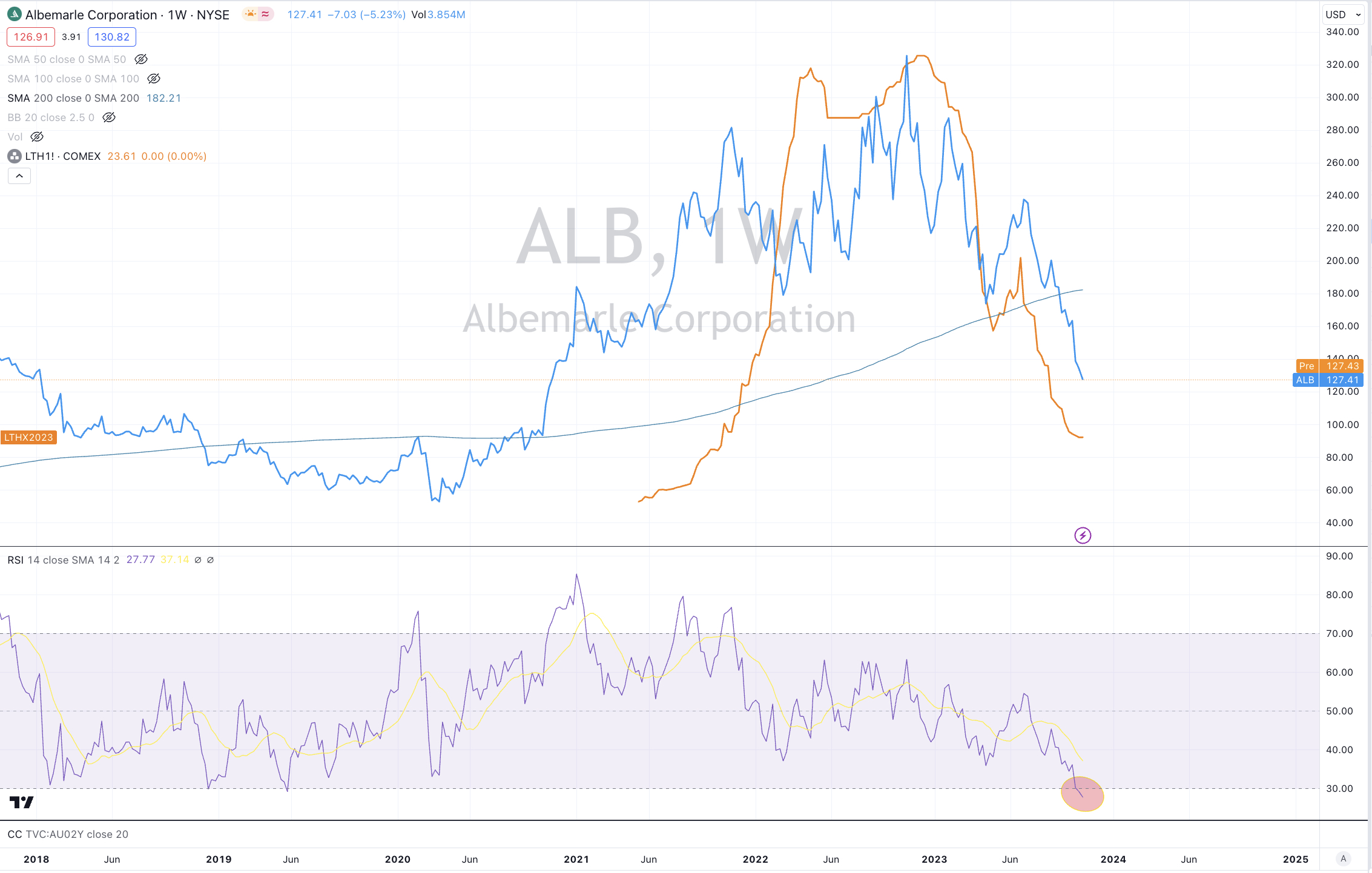

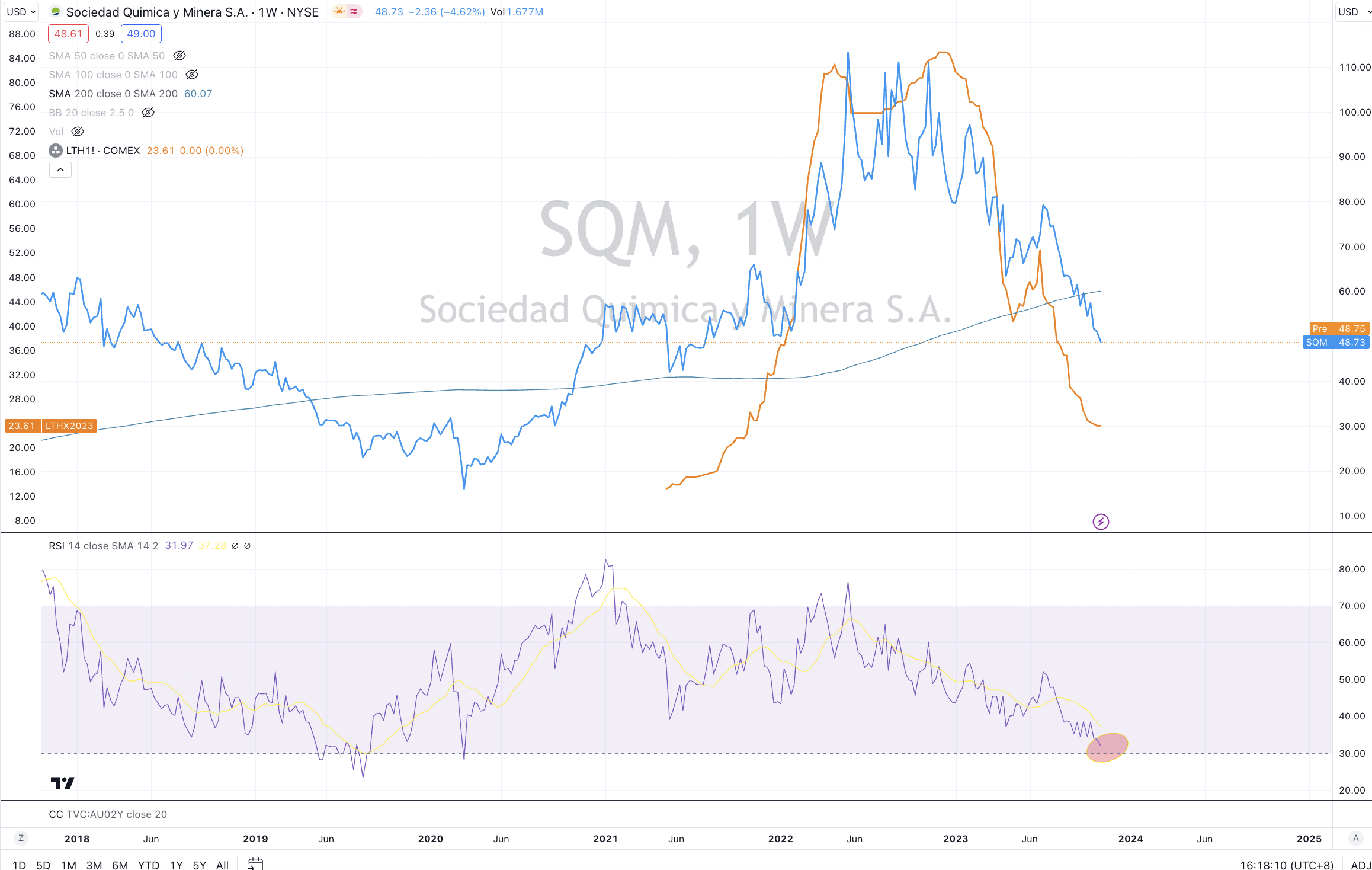

It is not a surprise that Lithium related stocks are falling.

They are mean reverting….back to their 200 week moving average (200 WMA).

Some have already done so, while others have more to go.

Some have registered oversold weekly readings too. Others are yet to do it.

In the weekly charts below, the stock price for each featured company is represented by the blue line.

The lithium hydroxide (Comex) futures price is in orange.

While some of the companies are mining (producing) lithium spodumene or lithium carbonate, you get the picture.

Before all of this carnage, many of them were trading at extreme percentages above that 200 WMA. That was a major warning back then which I wrote about and clients received those views directly.

Their fundamental valuations and capital expenditure plans is another discussion.

Gravity is indeed a bitch.

October 31, 2023

by Rob Zdravevski

rob@karriasset.com.au

October 30, 2023 Leave a comment

I think interest rates fall and mean revert.

Specifically, I expect the Australian 10 year bond yield to pull back to the 3% mark in the coming 6-12 months.

It’s currently at 4.88%

Once upon a time, I heard many investors say that would take a 5% return “any day of the week”.

Empirically, the Australian 10 year bond yield has no business being extended this far above its 200 week moving average, especially when coupled with the quantum of the move from its recent depths.

You should find this analog in (many) other government bond yields.

Falling bond yields should ignite discussion that diminishing and continuing negative real interest rate returns makes a positive case for being long equities.

There is also a trap for those fixing their borrowing rates today, possibly at the wrong end of the pendulum frenzy,

while falling rates could put some zip back into those ‘unprofitable’ tech stock stories again?

October 30, 2023

by Rob Zdravevski

rob@karriasset.com.au

October 29, 2023 Leave a comment

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations

Australian 3 year government bond yields

Australian 5 year government bond yields

Swiss and U.K. 10 year government bond yields

U.S. 5 year bond minus 3 month bill yield spread

Natural Gas

Gold as priced in AUD and CAD

EUR/JPY

Overbought (RSI > 70)

Chilean, Japanese, Turkish and U.S. 10 year government bond yields

Japanese 5 year government bond yield

U.S. 30 year government bond yields

TBT & TBX

U.S. 10 year bond yield minus German 10 year bond yield spread

U.S. 10 year minus 10 year breakeven inflation rate

Cocoa

Orange Juice

Uranium

And Rubber

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Australian 10 year government bond yield

U.S. 20 year government bond yield

Extremes “below” the Mean (at least 2.5 standard deviations)

Copper/Gold Ratio

Shangai Composite

CSI 300

China A50

Dow Jones Industrials

Dow Jones Transports

Nasdaq Composite

Spain’s IBEX

KOSPI

Nasdaq 100

ASX 200

S&P 500

And the Copenhagen, Helsinki and Swiss equity indices

Oversold (RSI < 30)

TLT

Lithium Hydroxide

Nickel

JPY/USD

MYR/USD

IDR/USD

The Oversold Quinella – Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

Nasdaq Biotech Index

Indonesia & Thailand’s equity indices

And the ASX Industrials Index

Notes & Ideas:

Government bond yields fell except in Australia and Japan.

U.S. 5 – 7 year corporate bond yields aren’t overbought this week.

The U.S.10 year minus U.S. inflation rate just eased out of overbought land

And for the 2nd consecutive week, the U.S. 3 month bill isn’t overbought.

Equities continued its slide with another woeful week.

Chinese equities were the odd ones out, rising 1.5%.

The silver lining is that more equity indices are registering oversold extremes.

The CAC, DAX, FTSE 250, IBEX and the DJ Transports are all in 6 week falling streaks.

The latter has declined 19% in13 weeks helping it complete a mean reversion to its 200 week moving average.

The Russell 2000 has fallen for 7 of its past 8 weeks, sinking 9% in the past 3 weeks.

The S&P Small Cap 600 has also eased lower in 7 of tis last 8 week, as it’s now in a ‘new’ 4 week consecutive slide and has sunk 16.5% over the past 13 weeks.

Indonesia’s main index has fallen for the past 5 weeks.

The Nasdaq Biotech index touched its first oversold quinella since May 2022. The Nasdaq 100 and the S&P 500 are at 2.5 standard deviations below their weekly mean for the first time since May and June 2022 respectively.

Copenhagen has registered 7 weekly losses out of its past 9.

The KOSPI Index is at its lowest close since January 2023.

And Stockholm, Toronto’s TSX, the MidCap 400, Singapore’s Strait Times and the ASX 200…..all reverted down to their respective 200 week moving average.

Commodities were mixed, again during the week.

Most energy contracts were weaker while industrial and precious metals firmed.

Baltic Dry Index isn’t overbought after sliding 24% and breaking its 7 week winning streak.

Inversely, Hot Rolled Coil Steel moved out of its 8 week residence in oversold territory after it rallied 23% in the past week.

Urea prices were amongst the losers for the week while Natural Gas was a notable winner.

Gold (as priced in CAD) has risen 11% over the past 3 weeks.

Uranium remains overbought for an 11th consecutive week.

while Lithium Hydroxide declining streak extends to 16 consecutive weeks.

Amongst currencies, the Australian Dollar was stronger agains all except the ZAR and THB.

The Loonie was weaker.

The BRL/USD has risen for the past 3 weeks after having declined steadily for the past 3 months to complete its mean reversion.

The GBP/AUD had a bearish outside week.

The JPY/USD is still floating around the extremes.

And the Indonesian Rupiah is in a 8 week losing streak versus the USD.

The larger advancers over the past week comprised of;

Aluminium 1.9%, Cocoa 4.3%, Cotton 2.4%, Lean Hogs 6.8%, Copper 2.3%, HRC 23.2%, Natural Gas 20.1%, Orange Juice 2.1%, Palladium 1.7%, Sugar 1.8%, Dutch TTF Gas 3.8%, Uranium 2.1%, Gold in CAD 2.5%, Oats 5.2%, CSI 300 1.5%, China A50 1.8%, HSCEI 1.8%, Mexico 1.5%, BIST 100 rose 2.6% and the ASX Materials Index rose 0.9%.

The group of decliners included;

Rotterdam Coal (5.8%), Baltic Dry Index (23.6%), WTI Crude Oil (2.9%), Gasoil (5.8%), Heating Oil (3.3%), Coffee (2.6%), LNG (4.2%), Newcastle Coal (4.9%), Nickel (2.1%), Gasoline (2.5%), Urea U.S. Gulf (5.2%), Brent Crude (3.9%), Urea Middle East (7.1%), Corn (3%), Wheat (1.8%), JKM (2.7%), KBW Banks (2.2%), DJ Industrials (2.1%), DJ Transports (6.2%), S&P SmallCap 600 (2.3%), Nasdaq Composite (2.6%), KOSPI (3%), Nasdaq Biotech’s (4.1%), Nasdaq 100 (2.6%), Nifty (2.5%), Russell 2000 (2.6%), S&P Small Cap 600 Value (2.9%), SOX (2.7%), S&P MidCap 400 (2.8%), S&P 500 (2.5%), TAEIX (1.9%), Nasdaq Transports (3.5%), TSX (2%), FTSE 100 (1.5%), ASX 200 (1.1%), ASX Industrials (2.4%) and the ASX Small Caps fell 1.9%.

October 29, 2023

by Rob Zdravevski

rob@karriasset.com.au

October 27, 2023 Leave a comment

Last night, Microsoft (MSFT:US) shares fell 4%, which means its market cap declined by US$92 billion.

In Australian Dollars that equals A$143 billion or nearly the total market capitalisation of the Commonwealth Bank of Australia.

But it’s OK, for in the previous day, its market cap rose by US$75 billion.

Even more impressively, 92 million shares traded over the past 2 days.

While that’s only 1.3% of their outstanding shares, it equates to US$31 billion worth of stock changing hands (or A$49 billion).

For some reference, the daily average value of the shares traded on the whole of the Australian (ASX) stockmarket is approximately A$5 billion (or US$3.2 billion).

Furthermore, Alphabet (Google) (GOOGL:US) has seen it’s stock price fall 12% over the past 2 days, meaning its market cap declined by US$211 billion or A$332 billion.

(The combined total market cap of Rio Tinto and BHP is ~ A$390 billion).

Over those days, 141.4 million shares traded or US$17.7 billion worth of stock.

And that’s just the Class A shares.

October 27, 2023

by Rob Zdravevski

rob@karriasset.com.au

October 26, 2023 Leave a comment

The market swoon in the ASX 200 should be nearing its conclusion.

The ASX 200 is a whisker from trading 2.5 standard deviations below its weekly mean.

The study below shows the various moments it has done so over the past 10 years.

Probability suggests allocating money at such moments but you’ll be disappointed if you’re seeking quick results.

October 26, 2023

by Rob Zdravevski

rob@karriasset.com.au

October 24, 2023 Leave a comment

I saw this news today:

Sealed Air’s (SEE:US) President and CEO steps down, effective immediately.

Sealed Air Corporation is a packaging company known for its brands such as Cryovac food packaging and Bubble Wrap cushioning packaging.

It’s a stunning announcement and often a change of CEO is a good catalyst for the stock price, but I was prompted to take a quick glance at financials…and I started typing out some notes.

Market Cap is $4.1 billion

Net Debt is $4.8 billion is more than its market cap, nearly as much as its annual revenue and 5.5 times more than its EBIT of $873 million.

The Interest Expense of $230 million (on that $4.8bn debt) equals 26% of its EBIT and 4% of its revenues

If you write-off or omit the $2.2 billion of goodwill held on the balance sheet, Net Assets are negative $2 billion.

Its inventories (which have doubled over the past 4 years) now equate to 18% of its revenue.

And that is only a quick glance….

To boot, the stock has fallen from $65 to $28 over the past 18 months and today Wall Street analysts are downgrading the stock. Hmmmm…..too late.

Today, I hear the term ‘value traps’ describing such stock price declines. That’s also too late.

The thing is….when the stock was trading at $60 (its market cap would have been nearly $8 billion) it wouldn’t a value trap….it would’ve simply been expensive.

p.s. it’s trading at the same price as seen in 1998.

The assessment about the company’s stock price to be done much earlier, under various ‘what-if” scenarios.

What if the cost of interest doubles?

What if we don’t sell and move our inventory?

What if we don’t receive 100 cents in the dollar for our $730 million in receivables?

While today, Sealed Air’s debt equals 100% of its market cap (I may discuss EV/EBITDA another day), there are other companies today whose debt equals 50% of their market cap.

What if………?

At some stage, this stock could be a really compelling to own but in a world full of other opportunities coupled with 5% risk free rates, do I need to be there especially when conviction is more paramount and in recent memory…..

but then, perhaps owning the debt is better than the equity.

October 24, 2023

by Rob Zdravevski

rob@karriasset.com.au

October 24, 2023 Leave a comment

For those who shorted the U.S. 30 year bond yesterday (link) while the yield was trading around 5.12% – 5.17%…….was it a case of the inability to think for oneself ?

Now I see it is trading at 4.95%, only 20 hours later.

This quip isn’t really about picking highs or lows, but I’m fairly sure (days earlier) that many of ‘those’ short sellers believed in the ‘higher rates for longer’ thesis………until they traded the new headlines.

That’s a strange way to think about a 30 year maturity bond?

October 24, 2023

by Rob Zdravevski

rob@karriasset.com.au

October 22, 2023 Leave a comment

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations

Australian 3 year government bond yields

Australian and U.S. 5 year government bond yields

Australian, Swiss and French 10 year government bond yields

U.S. 5 year breakeven inflation rate

U.S. 10 year breakeven inflation rate

U.S. 5 year bond minus 3 month bill yield spread

Rotterdam Coal

U.S. 10 year bond minus 5 year yield spread

Gold Volatility Index

Gold as priced in AUD and CAD

EUR/GBP

Overbought (RSI > 70)

Chilean, Japanese, New Zealand and Turkish 10 year government bond yields

Japanese 5 year government bond yield

U.S. 7, 10, 20 and 30 year government bond yields

TBT & TBX

U.S. 10 year bond minus 2 year yield spread

U.S. 10 year minus U.S. inflation rate

U.S. 10 year minus 10 year breakeven inflation rate

Australian Coking Coal

Baltic Dry Index

Orange Juice

Uranium

Rubber

And Russia’s MOEX

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

U.S. 5 – 7 year corporate bond yields

South Korean 10 year government bond yield

U.S. 10 year minus German 10 year government bond yield spread

Extremes “below” the Mean (at least 2.5 standard deviations)

Copper/Gold Ratio

IEI & SHY

MXN/USD

Shangai Composite

CSI 300

CAC 40

China A50

IDX, KOSPI, BOVESPA & IBEX

FTSE 250

Nasdaq Biotech Index

And the Copenhagen, Helsinki and Swiss equity indices

Oversold (RSI < 30)

U.S. Mid West Hot Rolled Coil Steel

Lithium Hydroxide

JPY/USD

MYR/USD

CLP/USD

IDR/USD

And Mexico’s equity index

The Oversold Quinella – Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

Thailand’s SET equity index

Notes & Ideas:

Government bond yields rose, reversing last week’s decline.

Many overbought yields which appeared in Macro Extremes over the past 2 weeks have now left the list.

Furthermore, the U.S. 3 month bill isn’t overbought.

While the U.S. 5-7 year corporate bond yields have returned to overbought territory, this time into the quinella category.

The mood was evident amongst Equities that another losing week resumes the recent slide.

Such is the ‘slide’ that many indices having fallen 5 of their last 7 weeks or 6 of their recent 8 weeks.

So much so, that a bunch of stock indices have re-entered oversold land.

The Russell 2000 has fallen 6% over the past 2 weeks and 16% in the last 12 weeks, while also closing at its lowest price since early October 2022.

The U.S. Regional Banking Index is at its lowest close since May 2023.

The KOSPI gave up last week’s gain to decline and become oversold whilst recording its lowest closing price since March 2023.

The FTSE 250 is in a 5 week losing streak having fallen 9% over the past 5 weeks.

The CAC and DAX are also in a 5 week losing streak.

The HSCEI is at its lowest close since late November 2022, the S&P MidCap 400 is 0.3% from reverting to its 200 week moving average, the ASX 200 is 0.6% away from doing the same and the Nasdaq Biotech Index and Copenhagen’s OMX 25 have closed at their lowest prices since late September 2022.

Commodities were mixed during the week.

We saw strength in precious metals and the agricultural’s and weakness amongst coal and gas prices.

Crude Oil took a break with WTI Crude only rising 0.4%.

Natural Gas isn’t overbought following its 9% decline during this past week.

The Baltic Dry Index has risen for 7 consecutive weeks, while Orange Juice broke its 6 week consecutive advance (falling from its recent all-time high) and Australian Coking Coal snapped its 14 week winning streak.

Gold (as priced in CAD) has risen 8% over the past fortnight while AUD Gold has climbed 9%. Both appear in this week’s overbought list.

Coffee has soared 14% in the past 2 weeks.

Natural Gas fell 9%, adding to last week’s 3% fall. This halves the 25% rally which started at the beginning of the month.

Uranium remains overbought for an 10th consecutive week.

U.S. Mid West Hot Rolled Coiled Steel has been oversold for 8 weeks,

while Lithium Hydroxide declining streak extends to 15 consecutive weeks.

Amongst currencies, the Australian Dollar was mostly higher against most pairs.

The Loonie was weaker and the Euro was firmer, not quite making to oversold territory.

The CHF/AUD is heading back towards overbought territory.

The Euro is close to being oversold.

The MYR/USD is in a 8 week losing streak.

The larger advancers over the past week comprised of;

Baltic Dry Index 5.2%, Cocoa 5.6%, Coffee 6.7%, LNG JKM 5.9%, Tin 3.3%, Platinum 2.4%, Gasoline 3.9%, Brent 1.6%, Uranium 4.8%, Silver in AUD 2.6%, Silver in USD 2.9%, Gold in AUD 2.2%, Gold in CAD 2.9%, Gold in USD 2.5%, Soybeans 3.1%, MOEX 2.4% and the ASX Industrial rose 0.7% having completed its reversion back to its 200 week moving average.

The group of decliners included;

Australian Coking Coal (2.9%), China Coking Coal (3.3%), Cotton (4.3%), Lean Hogs (5%), Lumber (3.6%), Newcastle Coal (3.6%), Natural Gas (9%), Palladium (3%), Dutch TTF Gas (5.3%), Shanghai (3.4%), CSI 300 (4.2%), AEX (2.4%), KBW Bank Index (3.8%), CAC (2.7%), China A50 (4.2%), DAX (2.6%), DJ Industrials (1.6%), MIB (3.1%), HSCEI (4%), Hang Seng (3.6%), IBEX (2.2%), BOVESPA (2.3%), Indonesia (3%), S&P SmallCal 600 (1.7%), Nasdaq Composite (3.2%), KRE Regional Banks (3.3%), KOSPI (3.3%), FTSE 250 (2.4%), S&P MidCap 400 (2%), Nasdaq Biotech’s (3.7%), Nasdaq 100 (2.9%), Nikkei 225 (3.3%), Oslo (3%), Copenhagen (5.1%), Helsinki (5.5%), Stockholm (5.1%), Russell 2000 (2%), SET (3.5%), SMI (5.1%), SOX (4%), Chile (2.8%), S&P 500 (2.4%), STI (3.4%), TAIEX (2%), Nasdaq Transports (3.1%), TSX (1.8%), FTSE 100 (2.6%), ASX 200 (2.1%), ASX Small Caps (2.2%), BIST 100 (7.4%) and the ASX Materials Index fell 1.6%.

October 22, 2023

by Rob Zdravevski

rob@karriasset.com.au

October 21, 2023 Leave a comment

The chart below shows a chart plotting Rockwell Automation’s (ROK:US) stock price on a weekly basis.

It’s making a new lower low, while not making any new ‘higher highs’.

For this particular stock, I’m looking to re-purchase its shares once it reaches some of those oversold milestones that I written often about.

While somewhere around the $248 mark would likely coincide with such an oversold ‘extreme’ moment, there is a “gap” at $201 which needs to be respected, especially if the current downtrend gathers strength.

October 21, 2023

by Rob Zdravevski

rob@karriasset.com.au