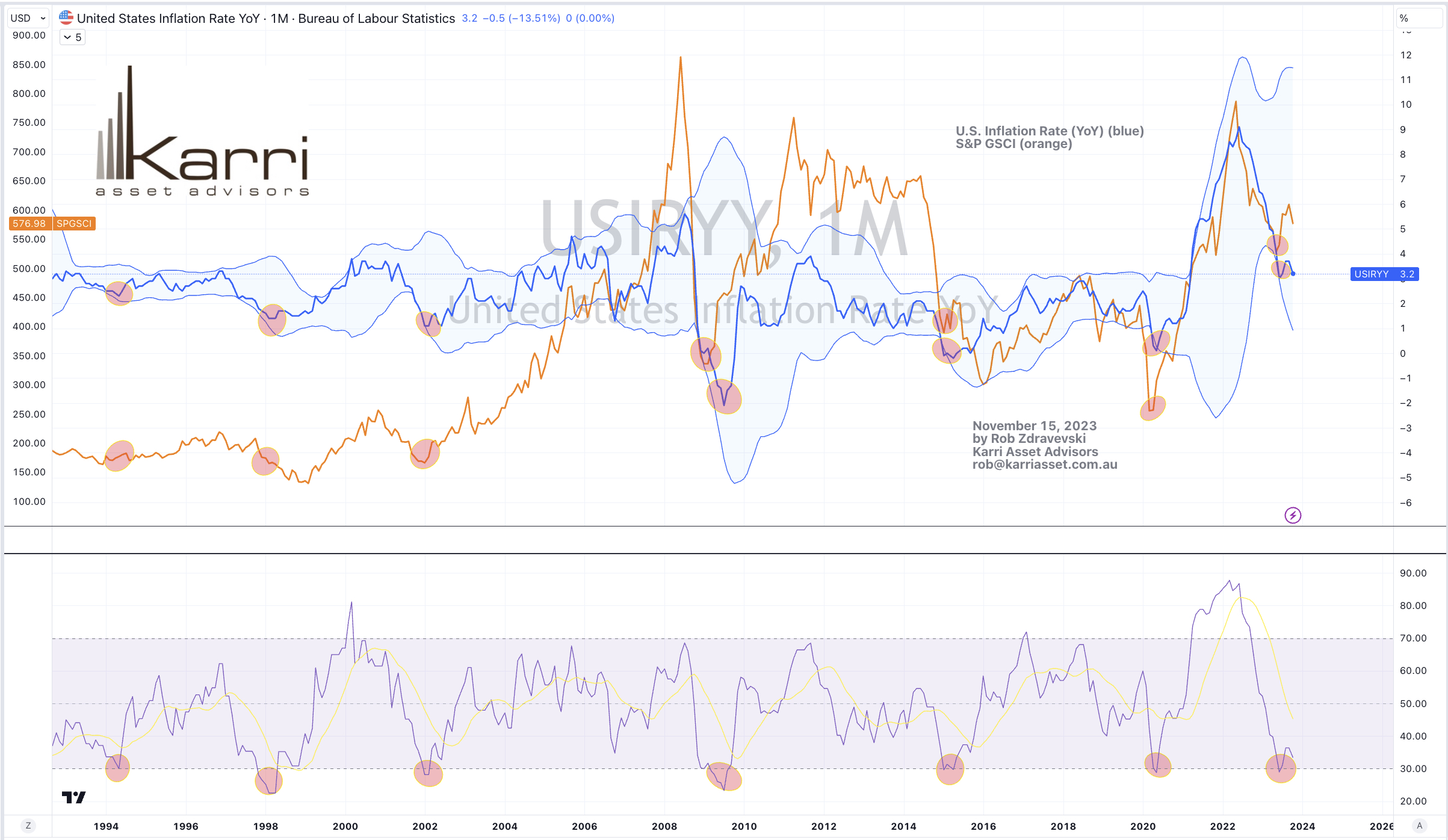

Macro Extremes (week ending November 17, 2023)

November 19, 2023 Leave a comment

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations

SHY – 1-3 year Treasury ETF

Rice

AUD/JPY

GBP/JPY

BOVESPA

Overbought (RSI > 70)

Turkish 10 year government bond yields

Cocoa

Orange Juice

Rubber

Uranium

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

EUR/JPY

Extremes “below” the Mean (at least 2.5 standard deviations)

Chilean and British 2 year government bond yields

And British 3, 5 and 10 year government bond yields.

Oversold (RSI < 30)

Lithium Hydroxide

Nickel

Palladium

The Oversold Quinella – Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

None

Notes & Ideas:

Government bond yields fell. Some have declined for 4 consecutive weeks.

Japanese 2 year bond yields fell sharply. The 5’s and 10’s also declined notably with the latter seeing a week on week change from 0.84% to 0.73%.

Swiss 10 year government bond yields were overbought last week and soon maybe entering oversold territory.

Equities had a positive week, almost everywhere.

So much so, no index appears in this week’s decliners list.

Chinese indices were subdued while Australian indices lagged the surging pack.

The ASX 200 rose 1%, the ASX Materials climbed 1.4% and the ASX Small Caps advanced 1.3%

The standout was the recently oversold ASX Industrials Index which soared 3.1% for the week.

It is worthy to note that various indices are now closing in on overbought territory, which tells me that this recent rally could be a short term trap.

Mexico’s index is in a 4 week winning streak.

Over the past 3 weeks, the DAX has risen 8%, the Nasdaq Composite has climbed 11%, while the KBW Bank Index has soared 16%.

Commodities generally rose, following a few weeks of weakness.

In fact, there were some substantial advancers as seen in the list below.

Silver, Palladium, Platinum and Orange Juice led the way.

Last week’s oversold entrants, Cotton, Coffee, Cattle, Newcastle Coal, Platinum, Oats….are no longer so.

Cocoa and Rubber are in the midst of 7 week winning streaks.

Energy contracts were still weaker, especially the Gases.

WTI Crude has closed at its lowest point since early July 2023. It is in a 4 week losing streak and had fallen It has fallen 15% over that time.

Incidentally, Brent Crude has also declined for 4 consecutive weeks.

Inversely, Heating Oil ended its 4 week losing streak, although its downtrend remains intact.

Natural Gas has slumped 14% over the past 2 weeks.

Baltic Dry Index rallied 23% in the past fortnight.

Uranium remains overbought for an 14th consecutive week.

while Lithium Hydroxide declining streak extends to 19 consecutive weeks,

And Silver had a bullish outside week.

Amongst currencies, the Australian Dollar was stronger, reversing last weeks weakness.

The Canadian Loonie was weaker along with the USD.

The DXY Index fell 1.9% for the week.

The Euro also exhibited strength.

The Yen remains weak and various pairs are appearing in the reciprocal overbought category.

The larger advancers over the past week comprised of;

Australian Coking Coal 2.1%, Baltic Dry Index 10.8%, Cocoa 2.3%, China Coal 2.5%, Cotton 5.4%, Gasoil 1.7%, Copper 4.2%, Lumber 5%, Tin 2.2%, Orange Juice 11.9%, Palladium 8.2%, Platinum 6.6%, Uranium 5.8%, Silver in AUD 4.1%, Silver in USD 6.6%, Gold in USD 2.2%, Rice 4%, AEX 1.7%, KBW Banks 6.9%, CAC 2.7%, DAX 4.5%, DJ Industrials 1.9%, DJ Transport 3.5%, MIB 3.5%, IBEX 4.2%, BOVESPA 3.5%, Indonesia 1.9%, S&P SmallCap 600 5.2%, Nasdaq Composite 2.4%, KRE Regional Banks 9.3%, KOSPI 2.5%, FTSE 250 4%, S&P MidCap 400 4%, Mexico 2.8%, Nasdaq Biotech 2.1%, Nasdaq 100 2%, Nikkei 3.1%, Copenhagen 4%, Helsinki 2.4%, Stockholm 3.9%, Russell 2000 5.6%, SET 1.9%, S&P Small Cap Value 5.4%, FTSE 100 2%, SMI 1.7%, SOX 4.3%, Chile 2.6%, S&P 500 2%, TAEIX 3.2%, Nasdaq Transports 3.7% and Toronto’s TSX rose 2.7%.

The group of decliners included;

Rotterdam Coal (3.1%), Coffee (2.3%), JKM LNG (3.9%), Lithium (1.9%), Newcastle Coal (3.1%), Natural Gas (2.4%), Gasoline (1.6%) and Dutch TTF Gas fell 3.4%.

November 19, 2023

by Rob Zdravevski

rob@karriasset.com.au

Happy Birthday Vida !